Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Petrus Resources Ltd. (TSE:PRQ) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Petrus Resources

What Is Petrus Resources's Net Debt?

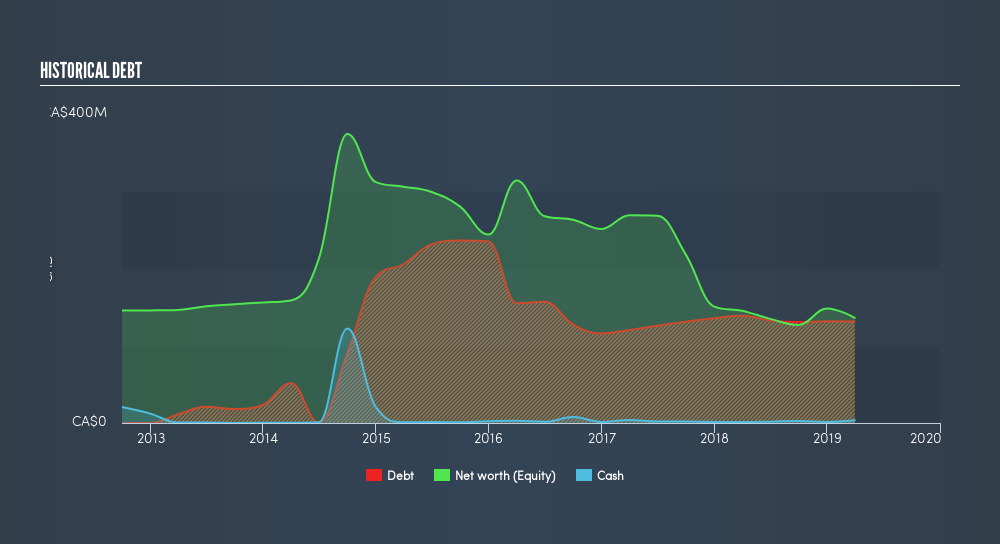

The image below, which you can click on for greater detail, shows that Petrus Resources had debt of CA$131.5m at the end of March 2019, a reduction from CA$138.7m over a year. However, because it has a cash reserve of CA$3.61m, its net debt is less, at about CA$127.9m.

How Healthy Is Petrus Resources's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Petrus Resources had liabilities of CA$24.7m due within 12 months and liabilities of CA$176.1m due beyond that. Offsetting this, it had CA$3.61m in cash and CA$11.9m in receivables that were due within 12 months. So its liabilities total CA$185.3m more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the CA$14.8m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Petrus Resources would likely require a major re-capitalisation if it had to pay its creditors today. Because it carries more debt than cash, we think it's worth watching Petrus Resources's balance sheet over time. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Petrus Resources's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Petrus Resources saw its revenue drop to CA$67m, which is a fall of 15%. That's not what we would hope to see.

Caveat Emptor

While Petrus Resources's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Indeed, it lost CA$818k at the EBIT level. When you combine this with the very significant balance sheet liabilities mentioned above, we are so wary of it that we are basically at a loss for the right words. Like every long-shot we're sure it has a glossy presentation outlining its blue-sky potential. But the reality is that it is low on liquid assets relative to liabilities, and it lost CA$9.7m in the last year. So we think buying this stock is risky, like walking through a minefield with a mask on. For riskier companies like Petrus Resources I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:PRQ

Petrus Resources

Engages in the acquisition, development, exploration, and exploitation of energy business-related assets in Canada.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor