Advertisement

There are a few key trends to look for if we want to identify the next multi-bagger. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. However, after briefly looking over the numbers, we don't think Jensen-Group (EBR:JEN) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Jensen-Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

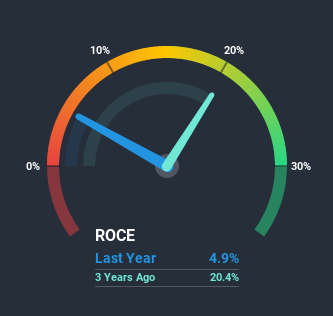

0.049 = €9.1m ÷ (€277m - €91m) (Based on the trailing twelve months to June 2020).

Thus, Jensen-Group has an ROCE of 4.9%. In absolute terms, that's a low return and it also under-performs the Machinery industry average of 8.6%.

Check out our latest analysis for Jensen-Group

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Jensen-Group's past further, check out this free graph of past earnings, revenue and cash flow.

The Trend Of ROCE

In terms of Jensen-Group's historical ROCE movements, the trend isn't fantastic. To be more specific, ROCE has fallen from 21% over the last five years. Given the business is employing more capital while revenue has slipped, this is a bit concerning. This could mean that the business is losing its competitive advantage or market share, because while more money is being put into ventures, it's actually producing a lower return - "less bang for their buck" per se.

On a side note, Jensen-Group has done well to pay down its current liabilities to 33% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.In Conclusion...

We're a bit apprehensive about Jensen-Group because despite more capital being deployed in the business, returns on that capital and sales have both fallen. Investors must expect better things on the horizon though because the stock has risen 12% in the last five years. Regardless, we don't like the trends as they are and if they persist, we think you might find better investments elsewhere.

Jensen-Group does come with some risks though, we found 3 warning signs in our investment analysis, and 1 of those shouldn't be ignored...

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade Jensen-Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ENXTBR:JEN

Jensen-Group

Designs, produces, and supplies single machines, systems, turnkey solutions, and laundry process automation for the heavy-duty laundry industry.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

100 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9820.4% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

23 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1558.0% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3648.3% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on DIGITAL HEARTS HOLDINGS ·

Strategic pivot in maximizing corporate value

Fair Value:JP¥928.162.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FI

Finder109 on BARK ·

Buy-out proposal for BARK Inc., at $1.10 has be confirmed by the acquisition group

Fair Value:US$1.443.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DH

Dhruva on Paladin Energy ·

Paladin Energy: Betting on the Nuclear Renaissance

Fair Value:AU$1.87563.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.9% undervalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.9% undervalued

1306 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.0% undervalued

1103 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative