Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:MOH

Moho Resources (ASX:MOH) Is Arguably In A Tricky Situation

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given this risk, we thought we'd take a look at whether Moho Resources (ASX:MOH) shareholders should be worried about its cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. Let's start with an examination of the business's cash, relative to its cash burn.

See our latest analysis for Moho Resources

When Might Moho Resources Run Out Of Money?

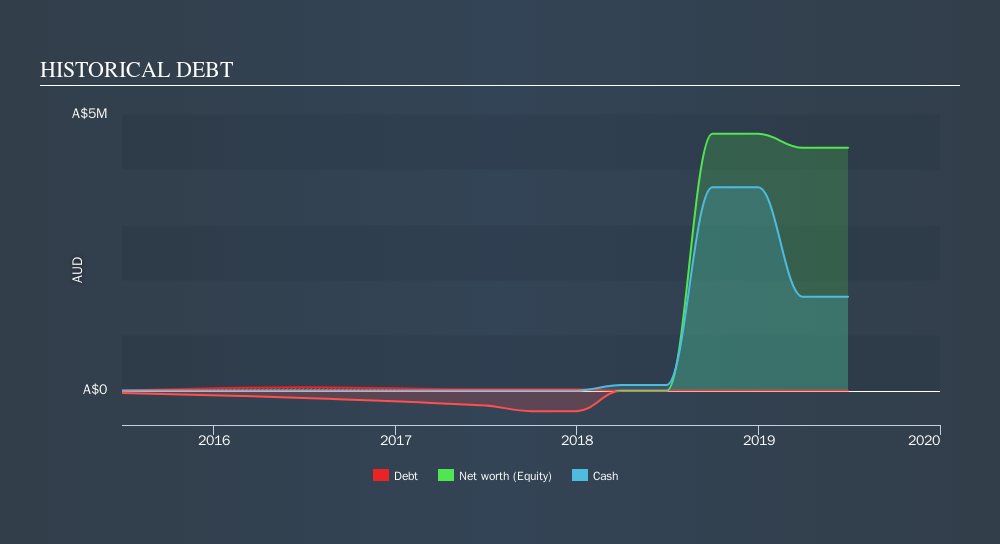

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at June 2019, Moho Resources had cash of AU$1.7m and no debt. Looking at the last year, the company burnt through AU$3.6m. So it had a cash runway of approximately 6 months from June 2019. With a cash runway that short, we strongly believe that the company must raise cash or else douse its cash burn promptly. Importantly, if we extrapolate recent cash burn trends, the cash runway would be a lot longer. The image below shows how its cash balance has been changing over the last few years.

How Is Moho Resources's Cash Burn Changing Over Time?

Although Moho Resources reported revenue of AU$213k last year, it didn't actually have any revenue from operations. That means we consider it a pre-revenue business, and we will focus our growth analysis on cash burn, for now. Its cash burn positively exploded in the last year, up 723%. Given that sharp increase in spending, the company's cash runway will shrink rapidly as it depletes its cash reserves. Admittedly, we're a bit cautious of Moho Resources due to its lack of significant operating revenues. So we'd generally prefer stocks from this list of stocks that have analysts forecasting growth.

How Easily Can Moho Resources Raise Cash?

Given its cash burn trajectory, Moho Resources shareholders should already be thinking about how easy it might be for it to raise further cash in the future. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Moho Resources has a market capitalisation of AU$3.2m and burnt through AU$3.6m last year, which is 112% of the company's market value. That suggests the company may have some funding difficulties, and we'd be very wary of the stock.

So, Should We Worry About Moho Resources's Cash Burn?

As you can probably tell by now, we're rather concerned about Moho Resources's cash burn. Take, for example, its cash burn relative to its market cap, which suggests the company may have difficulty funding itself, in the future. While not as bad as its cash burn relative to its market cap, its cash runway is also a concern, and considering everything mentioned above, we're struggling to find much to be optimistic about. Its cash burn burn situation feels about as relaxing as riding your bicycle home in the rain without so much as a jumper. The need for more cash seems just around the corner, and any dilution is likely to be rather severe. While it's important to consider hard data like the metrics discussed above, many investors would also be interested to note that Moho Resources insiders have been trading shares in the company. Click here to find out if they have been buying or selling.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:MOH

Moho Resources

Engages in the exploration and development of mineral resources in Australia.

Medium-low risk with excellent balance sheet.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5361.6% undervalued

143 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18054.9% undervalued

27 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.319.9% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2449.4% undervalued

33 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Partners Group Holding ·

Partners Group Holding will achieve an 8.14% revenue rise over the next 5 years

Fair Value:CHF 68030.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Cosmo ·

Cosmo Pharmaceuticals Announces Strong Full Year 2024 Revenue and Cash and Provides Business and Pipeline Updates

Fair Value:CHF 10023.8% undervalued

84 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on STIF Société anonyme ·

Niche global leader in BESS explosion protection

Fair Value:€6014.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.6% undervalued

111 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.0% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.1% undervalued

1183 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative