Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGM:EVER

Market Sentiment Around Loss-Making EverQuote, Inc. (NASDAQ:EVER)

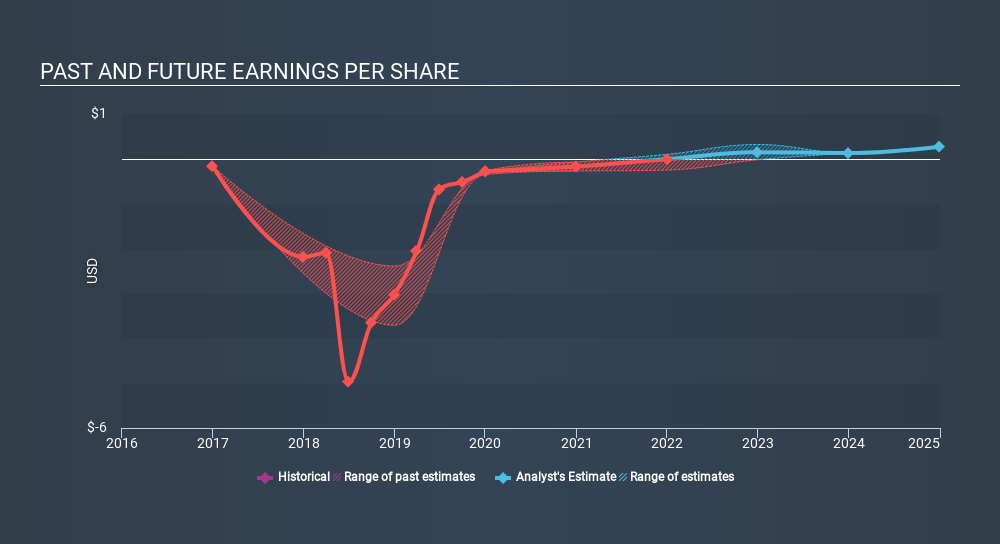

EverQuote, Inc.'s (NASDAQ:EVER): EverQuote, Inc. operates an online marketplace for insurance shopping in the United States. The US$1.0b market-cap company announced a latest loss of -US$7.1m on 31 December 2019 for its most recent financial year result. As path to profitability is the topic on EVER’s investors mind, I’ve decided to gauge market sentiment. I’ve put together a brief outline of industry analyst expectations for EVER, its year of breakeven and its implied growth rate.

Check out our latest analysis for EverQuote

According to the 8 industry analysts covering EVER, the consensus is breakeven is near. They expect the company to post a final loss in 2021, before turning a profit of US$4.2m in 2022. So, EVER is predicted to breakeven approximately 2 years from now. How fast will EVER have to grow each year in order to reach the breakeven point by 2022? Working backwards from analyst estimates, it turns out that they expect the company to grow 68% year-on-year, on average, which is rather optimistic! If this rate turns out to be too aggressive, EVER may become profitable much later than analysts predict.

I’m not going to go through company-specific developments for EVER given that this is a high-level summary, though, keep in mind that by and large a high forecast growth rate is not unusual for a company that is currently undergoing an investment period.

One thing I’d like to point out is that EVER has no debt on its balance sheet, which is rare for a loss-making loss-making, growth company, which typically has high debt relative to its equity. EVER currently operates purely off its shareholder funding and has no debt obligation, reducing concerns around repayments and making it a less risky investment.

Next Steps:

There are too many aspects of EVER to cover in one brief article, but the key fundamentals for the company can all be found in one place – EVER’s company page on Simply Wall St. I’ve also compiled a list of pertinent factors you should further research:

- Valuation: What is EVER worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether EVER is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on EverQuote’s board and the CEO’s back ground.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGM:EVER

EverQuote

Operates an online marketplace for insurance shopping in the United States.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

119 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.0% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

AN

AnimalDoctorKwon on Akebia Therapeutics ·

Vafseo and the Future of Renal Anemia Treatment – Akebia’s Vision for a $5B Kidney Disease Portfolio

Fair Value:US$77.2998.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Butler National ·

Butler National (Buks) outperforms.

Fair Value:US$3.449.3% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EV

evd101 on eToro Group ·

eToro: A High-Risk, Top-Tier Opportunity in the Future of Social Investing

Fair Value:US$148.8579.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.6% undervalued

1308 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.0% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative