Advertisement

- United States

- /

- Communications

- /

- NYSE:JNPR

Juniper Networks, Inc. Annual Results Just Came Out: Here's What Analysts Are Forecasting For Next Year

Juniper Networks, Inc. (NYSE:JNPR) shares fell 6.8% to US$22.76 in the week since its latest annual results. The result was positive overall - although revenues of US$4.4b were in line with what analysts predicted, Juniper Networks surprised by delivering a statutory profit of US$0.99 per share, modestly greater than expected. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Juniper Networks

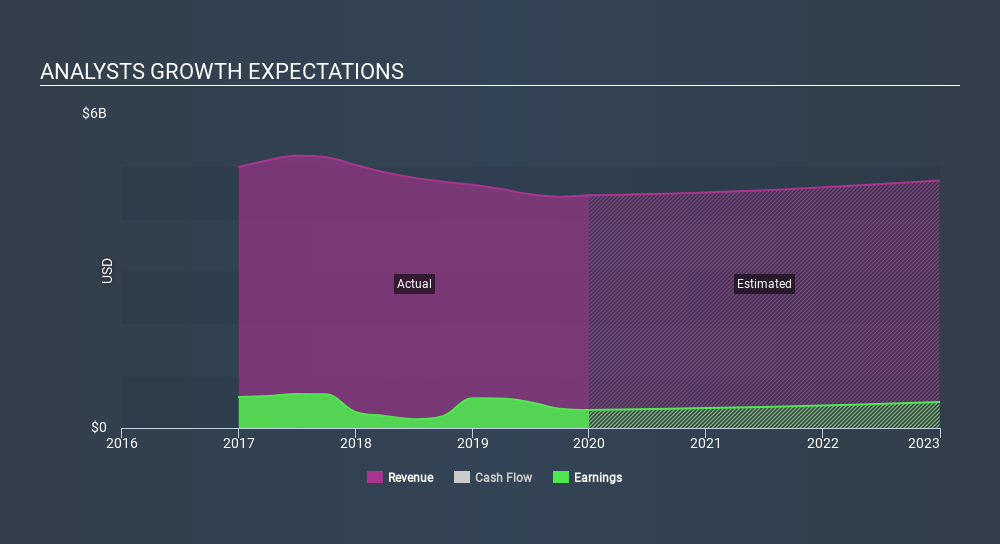

Taking into account the latest results, Juniper Networks's 20 analysts currently expect revenues in 2020 to be US$4.50b, approximately in line with the last 12 months. Statutory earnings per share are expected to climb 17% to US$1.17. In the lead-up to this report, analysts had been modelling revenues of US$4.50b and earnings per share (EPS) of US$1.24 in 2020. Analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share forecasts for next year.

It might be a surprise to learn that the consensus price target was broadly unchanged at US$25.28, with analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Juniper Networks, with the most bullish analyst valuing it at US$30.00 and the most bearish at US$19.00 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Juniper Networks shareholders.

Zooming out to look at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up both against past performance, and against industry growth estimates. It's also worth noting that the years of declining sales look to have come to an end, with the forecast for flat revenues next year. Historically, Juniper Networks's sales have shrunk approximately 0.7% annually over the past five years. Compare this against analyst estimates for the wider market, which suggest that (in aggregate) market revenues are expected to grow 3.4% next year. So it's pretty clear that, although revenues are improving, Juniper Networks is still expected to grow slower than the market.

The Bottom Line

The biggest concern with the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Juniper Networks. Fortunately, analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that Juniper Networks's revenues are expected to perform worse than the wider market. The consensus price target held steady at US$25.28, with the latest estimates not enough to have an impact on analysts' estimated valuations.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have forecasts for Juniper Networks going out to 2022, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:JNPR

Juniper Networks

Designs, develops, and sells network products and services worldwide.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor