Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies United Therapeutics Corporation (NASDAQ:UTHR) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for United Therapeutics

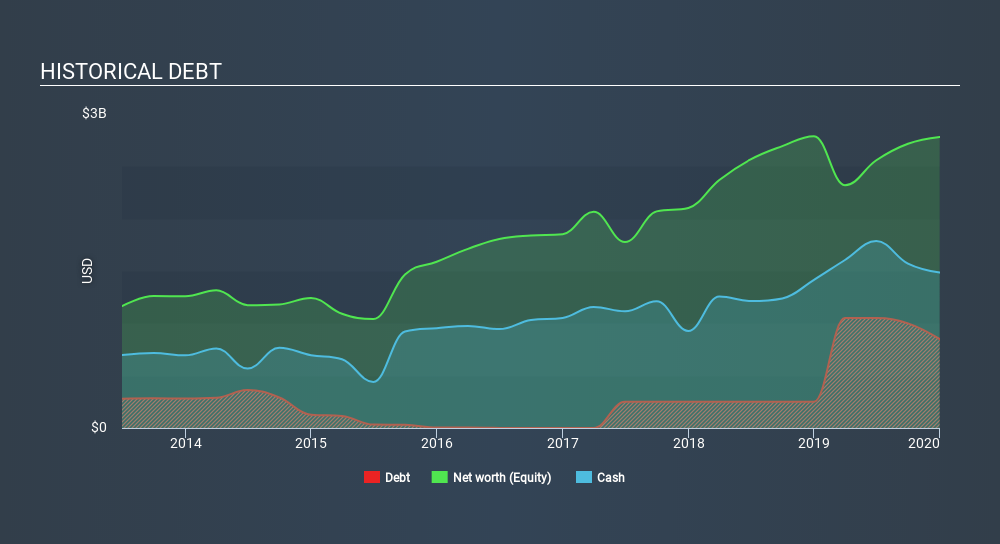

What Is United Therapeutics's Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2019 United Therapeutics had US$850.0m of debt, an increase on US$250.0m, over one year. But it also has US$1.49b in cash to offset that, meaning it has US$635.9m net cash.

How Strong Is United Therapeutics's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that United Therapeutics had liabilities of US$463.0m due within 12 months and liabilities of US$670.0m due beyond that. On the other hand, it had cash of US$1.49b and US$151.4m worth of receivables due within a year. So it can boast US$504.3m more liquid assets than total liabilities.

This surplus suggests that United Therapeutics has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, United Therapeutics boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine United Therapeutics's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year United Therapeutics had negative earnings before interest and tax, and actually shrunk its revenue by 11%, to US$1.4b. We would much prefer see growth.

So How Risky Is United Therapeutics?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that United Therapeutics had negative earnings before interest and tax (EBIT), over the last year. Indeed, in that time it burnt through US$290m of cash and made a loss of US$105m. Given it only has net cash of US$635.9m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - United Therapeutics has 1 warning sign we think you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:UTHR

United Therapeutics

A biotechnology company, engages in the development and commercialization of products to address the unmet medical needs of patients with chronic and life-threatening diseases in the United States and internationally.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor