Advertisement

As the AU$20m market cap 8common Limited (ASX:8CO) released another year of negative earnings, investors may be on edge waiting for breakeven. Savvy investors should always reassess the situation of loss-making companies frequently, and keep informed about whether or not these businesses are in a strong cash position. This is because new equity from additional capital raising can thin out the value of current shareholders’ stake in the company. Given that 8common is spending more money than it earns, it will need to fund its expenses via external sources of capital. Today I’ve examined 8common’s financial data from its most recent earnings update, to roughly assess when the company may need to raise new capital.

View our latest analysis for 8common

What is cash burn?

Currently, 8common has AU$1.0m in cash holdings and producing negative free cash flow of -AU$130.5k. The biggest threat facing 8common investors is the company going out of business when it runs out of money and cannot raise any more capital. Not surprisingly, it is more common to find unprofitable companies in the high-growth tech industry. These companies face the trade-off between running the risk of depleting its cash reserves too fast, or falling behind competition on innovation and gaining market share by investing too slowly.

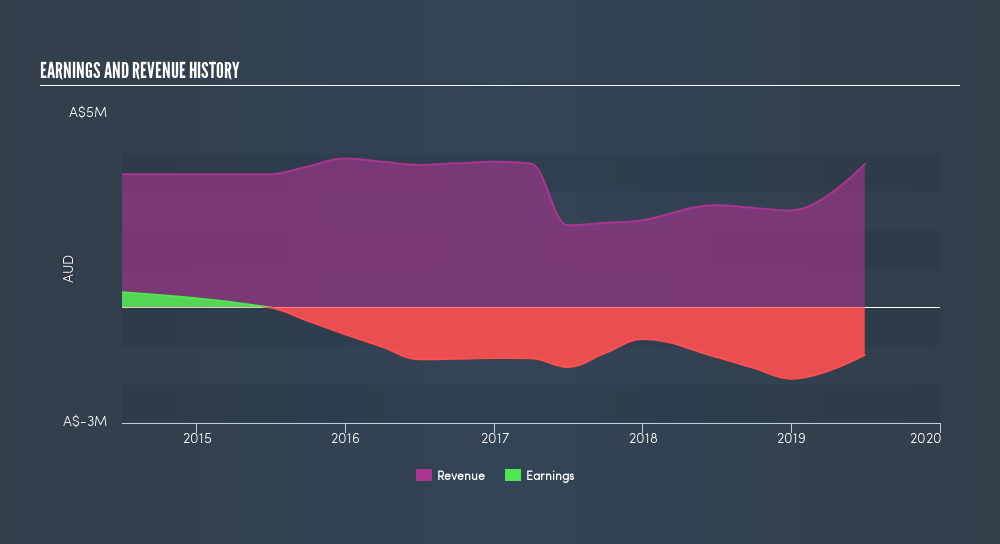

When will 8common need to raise more cash?

We can measure 8common's ongoing cash expenditure requirements by looking at free cash flow, which I define as cash flow from operations minus fixed capital investment, is a measure of how much cash a company generates/loses each year.

In the past year, free cash outflows (excluding one-offs) rose by 29%, which is substantial. However, given the current levels of cash holdings, it seems that 8common will not need further capital soon. The company may be able to continue investing at the same rate without having to issue equity or borrow within the next three years. Although this is a relatively simplistic calculation, and 8common could reduce its costs or open a new line of credit instead of issuing new shares, this analysis still helps us understand how sustainable the 8common operation is, and when things may have to change.

Next Steps:

Although 8common’s cash burn is growing at a double-digit rate, investors can breathe easy knowing it probably won’t be raising money any time soon. Shareholders may be pleased to know this as it signals that the company still has a strong cash reserve, as well as less likelihood of share dilution from new capital raising. However, this analysis still doesn’t tell us when 8common will become breakeven. I suggest you take a look at their expected revenue growth to determine the timing of future profitability as well. I admit this is a fairly basic analysis for 8CO's financial health. Other important fundamentals need to be considered as well. I suggest you continue to research 8common to get a more holistic view of the company by looking at:- Historical Performance: What has 8CO's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on 8common’s board and the CEO’s back ground.

- Other High-Performing Stocks: If you believe you should cushion your portfolio with something less risky, scroll through our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 30 June 2019. This may not be consistent with full year annual report figures. Operating expenses include only SG&A and one-year R&D.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:8CO

8common

Engages in the expense management software business in Australia, Asia, North America, and internationally.

Medium-low and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor