Advertisement

- United Kingdom

- /

- Hospitality

- /

- AIM:FUL

Is The Fulham Shore PLC's (LON:FUL) CEO Paid Enough Relative To Peers?

Nabil Ayad Mankarious is the CEO of The Fulham Shore PLC (LON:FUL). First, this article will compare CEO compensation with compensation at similar sized companies. Next, we'll consider growth that the business demonstrates. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

Check out our latest analysis for Fulham Shore

How Does Nabil Ayad Mankarious's Compensation Compare With Similar Sized Companies?

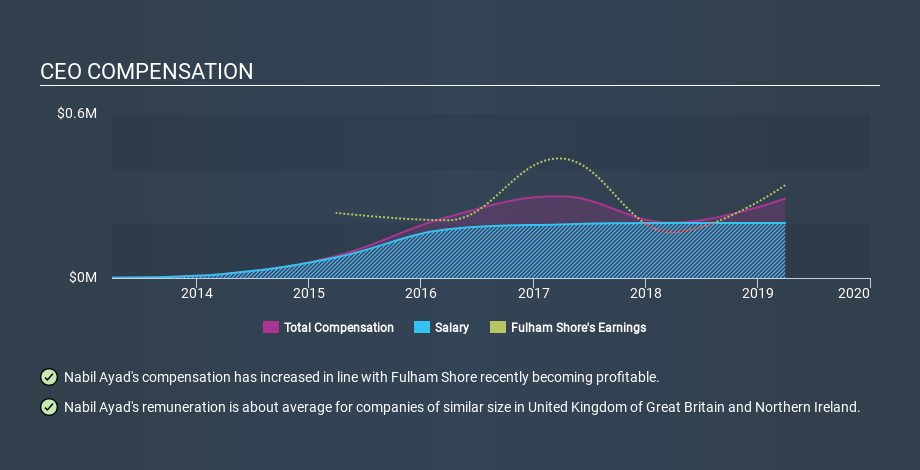

At the time of writing, our data says that The Fulham Shore PLC has a market cap of UK£32m, and reported total annual CEO compensation of UK£291k for the year to March 2019. We think total compensation is more important but we note that the CEO salary is lower, at UK£201k. We took a group of companies with market capitalizations below UK£170m, and calculated the median CEO total compensation to be UK£276k.

Now let's take a look at the pay mix on an industry and company level to gain a better understanding of where Fulham Shore stands. On a sector level, around 64% of total compensation represents salary and 36% is other remuneration. Our data reveals that Fulham Shore allocates salary in line with the wider market.

So Nabil Ayad Mankarious is paid around the average of the companies we looked at. This doesn't tell us a whole lot on its own, but looking at the performance of the actual business will give us useful context. You can see a visual representation of the CEO compensation at Fulham Shore, below.

Is The Fulham Shore PLC Growing?

Over the last three years The Fulham Shore PLC has shrunk its earnings per share by an average of 50% per year (measured with a line of best fit). In the last year, its revenue is up 11%.

Sadly for shareholders, earnings per share are actually down, over three years. While the revenue growth is good to see, it is outweighed by the fact that earnings per share are down, over three years. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has The Fulham Shore PLC Been A Good Investment?

With a three year total loss of 69%, The Fulham Shore PLC would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Nabil Ayad Mankarious is paid around the same as most CEOs of similar size companies.

After looking at EPS and total shareholder returns, it's certainly hard to argue the company has performed well, since both metrics are down. Most would consider it prudent for the company to hold off any CEO pay rise until performance improves. Looking into other areas, we've picked out 3 warning signs for Fulham Shore that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About AIM:FUL

Fulham Shore

The Fulham Shore PLC owns, operates, and manages restaurants in the United Kingdom.

Reasonable growth potential with proven track record.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.558.3% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.1% undervalued

56 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.2% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

JU

julio on Bath & Body Works ·

BBWI VALUATION

Fair Value:US$36.1839.7% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

TR

Treasury_Raccoon_w0gg on Walmart ·

Walmart's 'Other' Segment Will Power New Growth Beyond Retail

Fair Value:US$154.5823.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on REA Group ·

Is REA Group a Good Value Opportunity?

Fair Value:AU$1489.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17060.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative