Advertisement

Mark Ryan became the CEO of Tassal Group Limited (ASX:TGR) in 2003. First, this article will compare CEO compensation with compensation at similar sized companies. Next, we'll consider growth that the business demonstrates. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. This method should give us information to assess how appropriately the company pays the CEO.

View our latest analysis for Tassal Group

How Does Mark Ryan's Compensation Compare With Similar Sized Companies?

Our data indicates that Tassal Group Limited is worth AU$811m, and total annual CEO compensation was reported as AU$1.2m for the year to June 2019. While we always look at total compensation first, we note that the salary component is less, at AU$719k. As part of our analysis we looked at companies in the same jurisdiction, with market capitalizations of AU$292m to AU$1.2b. The median total CEO compensation was AU$1.1m.

Pay mix tells us a lot about how a company functions versus the wider industry, and it's no different in the case of Tassal Group. On a sector level, around 56% of total compensation represents salary and 44% is other remuneration. So it seems like there isn't a significant difference between Tassal Group and the broader market, in terms of salary allocation in the overall compensation package.

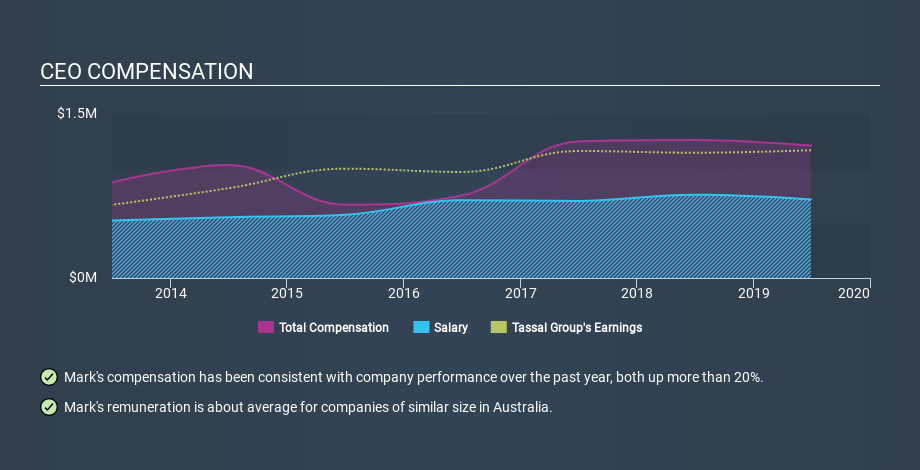

That means Mark Ryan receives fairly typical remuneration for the CEO of a company that size. This doesn't tell us a whole lot on its own, but looking at the performance of the actual business will give us useful context. You can see, below, how CEO compensation at Tassal Group has changed over time.

Is Tassal Group Limited Growing?

On average over the last three years, Tassal Group Limited has shrunk earnings per share by 1.6% each year (measured with a line of best fit). Its revenue is down 7.4% over last year.

In the last three years the company has failed to grow earnings per share. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. You might want to check this free visual report on analyst forecasts for future earnings.

Has Tassal Group Limited Been A Good Investment?

Tassal Group Limited has served shareholders reasonably well, with a total return of 15% over three years. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

In Summary...

Remuneration for Mark Ryan is close enough to the median pay for a CEO of a similar sized company .

We're not seeing great strides in earnings per share, and total returns were decent but not amazing in the last three years. We're not saying the CEO pay is too generous, but one might argue that the company should improve returns to shareholders before increasing it. On another note, Tassal Group has 4 warning signs (and 1 which is a bit concerning) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About ASX:TGR

Tassal Group

Tassal Group Limited, together with its subsidiaries, engages in the hatching, farming, processing, marketing, and sale of Atlantic salmon and tiger prawns in Australia.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.558.3% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.1% undervalued

53 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.2% undervalued

62 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.3% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on REA Group ·

Is REA Group a Good Value Opportunity?

Fair Value:AU$1489.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on ServiceNow ·

The Company Nobody Brags About

Fair Value:US$165.6943.4% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on ASX ·

ASX Limited

Fair Value:AU$4320.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17060.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative