Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:VIVO

Is Meridian Bioscience (NASDAQ:VIVO) A Risky Investment?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Meridian Bioscience, Inc. (NASDAQ:VIVO) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Meridian Bioscience

What Is Meridian Bioscience's Debt?

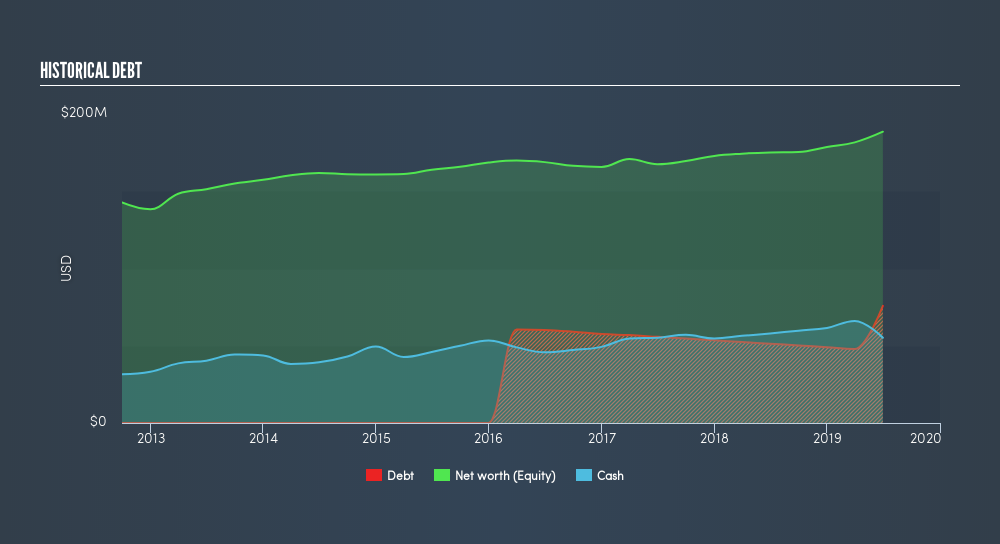

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Meridian Bioscience had US$75.8m of debt, an increase on US$51.3m, over one year. However, because it has a cash reserve of US$55.2m, its net debt is less, at about US$20.6m.

A Look At Meridian Bioscience's Liabilities

We can see from the most recent balance sheet that Meridian Bioscience had liabilities of US$19.8m falling due within a year, and liabilities of US$114.1m due beyond that. On the other hand, it had cash of US$55.2m and US$32.0m worth of receivables due within a year. So its liabilities total US$46.7m more than the combination of its cash and short-term receivables.

Given Meridian Bioscience has a market capitalization of US$431.8m, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Meridian Bioscience has a low net debt to EBITDA ratio of only 0.40. And its EBIT easily covers its interest expense, being 51.6 times the size. So we're pretty relaxed about its super-conservative use of debt. While Meridian Bioscience doesn't seem to have gained much on the EBIT line, at least earnings remain stable for now. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Meridian Bioscience can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Meridian Bioscience recorded free cash flow worth 78% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Meridian Bioscience's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! It's also worth noting that Meridian Bioscience is in the Medical Equipment industry, which is often considered to be quite defensive. Zooming out, Meridian Bioscience seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Meridian Bioscience insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:VIVO

Meridian Bioscience

Meridian Bioscience, Inc., a life science company, develops, manufactures, distributes, and sells diagnostic test kits primarily for gastrointestinal and respiratory infectious diseases, and elevated blood lead levels worldwide.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor