Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies KuangChi Science Limited (HKG:439) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for KuangChi Science

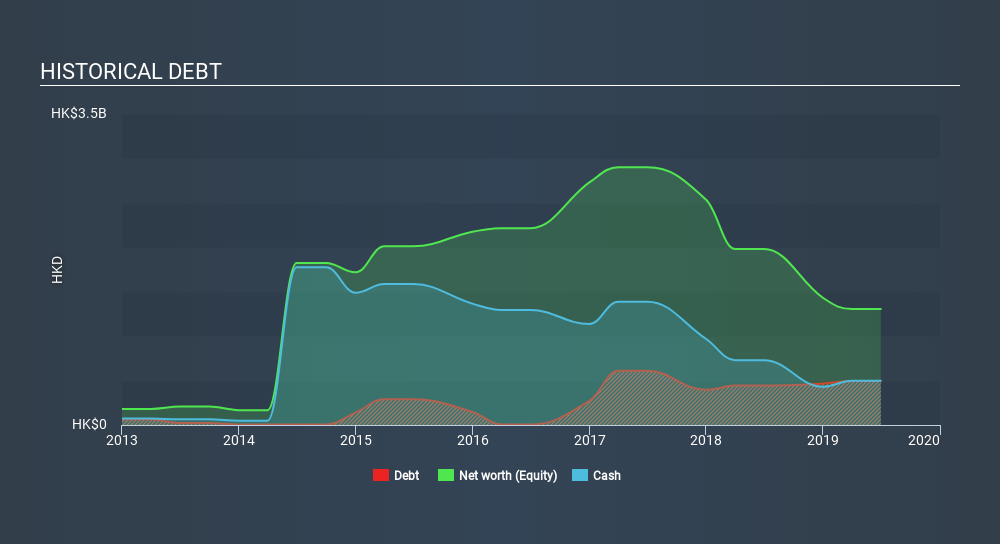

How Much Debt Does KuangChi Science Carry?

You can click the graphic below for the historical numbers, but it shows that as of June 2019 KuangChi Science had HK$494.4m of debt, an increase on HK$444.4m, over one year. However, it does have HK$498.2m in cash offsetting this, leading to net cash of HK$3.83m.

How Healthy Is KuangChi Science's Balance Sheet?

We can see from the most recent balance sheet that KuangChi Science had liabilities of HK$509.6m falling due within a year, and liabilities of HK$226.1m due beyond that. On the other hand, it had cash of HK$498.2m and HK$222.1m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$15.5m.

This state of affairs indicates that KuangChi Science's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the HK$1.97b company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, KuangChi Science also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for KuangChi Science (of which 1 is major) which any shareholder or potential investor should be aware of.

In the last year KuangChi Science had negative earnings before interest and tax, and actually shrunk its revenue by 50%, to HK$103m. That makes us nervous, to say the least.

So How Risky Is KuangChi Science?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months KuangChi Science lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through HK$291m of cash and made a loss of HK$321m. However, it has net cash of HK$3.83m, so it has a bit of time before it will need more capital. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how KuangChi Science's profit, revenue, and operating cashflow have changed over the last few years.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:439

KuangChi Science

An investment holding company, engages in the development of artificial intelligence (AI) technology and related products in the People’s Republic of China, Hong Kong, and internationally.

Excellent balance sheet very low.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor