Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Hemcheck Sweden AB (publ) (STO:HEMC) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Hemcheck Sweden

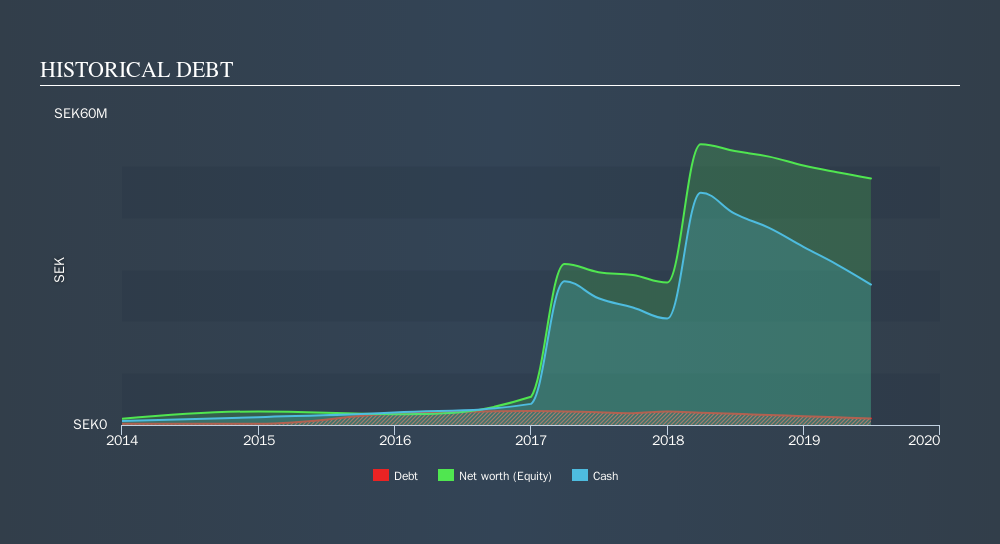

What Is Hemcheck Sweden's Net Debt?

You can click the graphic below for the historical numbers, but it shows that Hemcheck Sweden had kr1.27m of debt in June 2019, down from kr2.15m, one year before. But on the other hand it also has kr27.1m in cash, leading to a kr25.8m net cash position.

How Strong Is Hemcheck Sweden's Balance Sheet?

We can see from the most recent balance sheet that Hemcheck Sweden had liabilities of kr3.15m falling due within a year, and liabilities of kr425.5k due beyond that. Offsetting this, it had kr27.1m in cash and kr392.7k in receivables that were due within 12 months. So it can boast kr23.9m more liquid assets than total liabilities.

This luscious liquidity implies that Hemcheck Sweden's balance sheet is sturdy like a giant sequoia tree. On this view, it seems its balance sheet is as strong as a black-belt karate master. Succinctly put, Hemcheck Sweden boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is Hemcheck Sweden's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Hemcheck Sweden reported revenue of kr4.4m, which is a gain of 11%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Hemcheck Sweden?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Hemcheck Sweden had negative earnings before interest and tax (EBIT), over the last year. And over the same period it saw negative free cash outflow of kr13m and booked a kr5.8m accounting loss. But at least it has kr25.8m on the balance sheet to spend on growth, near-term. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Hemcheck Sweden insider transactions.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OM:BIOVIT

Bio Vitos Pharma

Operates as a medical technology company in Sweden and internationally.

Medium-low with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor