Advertisement

Jeff Fox became the CEO of Endurance International Group Holdings, Inc. (NASDAQ:EIGI) in 2017. This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. After that, we will consider the growth in the business. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

Check out our latest analysis for Endurance International Group Holdings

How Does Jeff Fox's Compensation Compare With Similar Sized Companies?

According to our data, Endurance International Group Holdings, Inc. has a market capitalization of US$220m, and paid its CEO total annual compensation worth US$2.9m over the year to December 2018. We think total compensation is more important but we note that the CEO salary is lower, at US$794k. We further remind readers that the CEO may face performance requirements to receive the non-salary part of the total compensation. When we examined a selection of companies with market caps ranging from US$100m to US$400m, we found the median CEO total compensation was US$1.5m.

Pay mix tells us a lot about how a company functions versus the wider industry, and it's no different in the case of Endurance International Group Holdings. Speaking on an industry level, we can see that nearly 15% of total compensation represents salary, while the remainder of 85% is other remuneration. Endurance International Group Holdings pays out 27% of aggregate payment in the shape of a salary, which is significantly higher than the industry average.

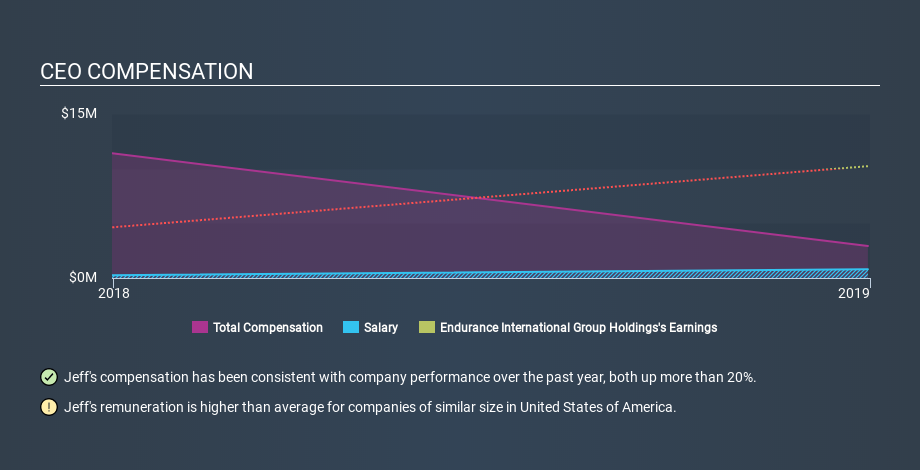

Thus we can conclude that Jeff Fox receives more in total compensation than the median of a group of companies in the same market, and of similar size to Endurance International Group Holdings, Inc.. However, this doesn't necessarily mean the pay is too high. We can better assess whether the pay is overly generous by looking into the underlying business performance. The graphic below shows how CEO compensation at Endurance International Group Holdings has changed from year to year.

Is Endurance International Group Holdings, Inc. Growing?

Endurance International Group Holdings, Inc. has increased its earnings per share (EPS) by an average of 84% a year, over the last three years (using a line of best fit). In the last year, its revenue is down 2.8%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. Revenue growth is a real positive for growth, but ultimately profits are more important. It could be important to check this free visual depiction of what analysts expect for the future.

Has Endurance International Group Holdings, Inc. Been A Good Investment?

With a three year total loss of 81%, Endurance International Group Holdings, Inc. would certainly have some dissatisfied shareholders. So shareholders would probably think the company shouldn't be too generous with CEO compensation.

In Summary...

We compared the total CEO remuneration paid by Endurance International Group Holdings, Inc., and compared it to remuneration at a group of similar sized companies. Our data suggests that it pays above the median CEO pay within that group.

However, the earnings per share growth over three years is certainly impressive. On the other hand returns to investors over the same period have probably disappointed many. While EPS is positive, we'd say shareholders would want better returns before the CEO is paid much more. Looking into other areas, we've picked out 2 warning signs for Endurance International Group Holdings that investors should think about before committing capital to this stock.

Important note: Endurance International Group Holdings may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor