Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that DTE Energy Company (NYSE:DTE) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for DTE Energy

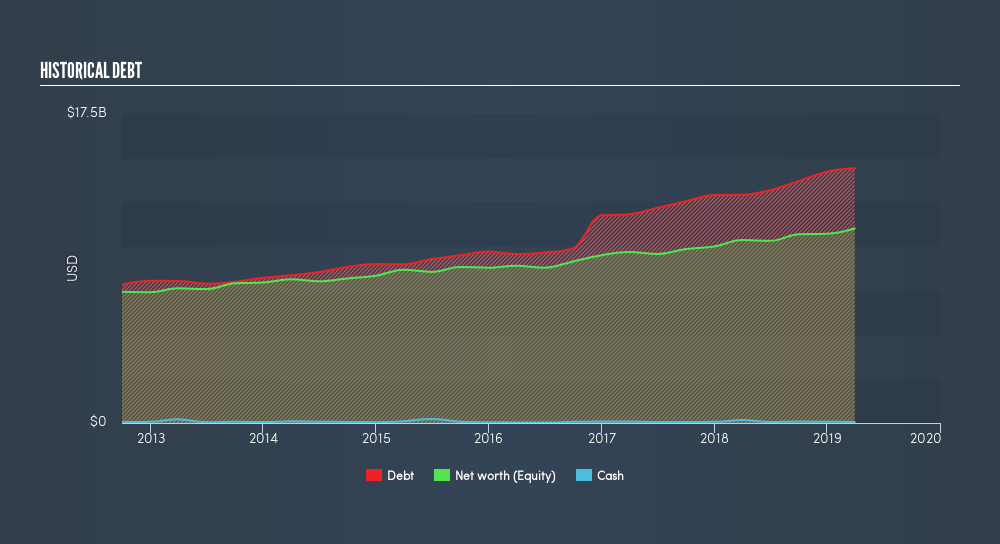

What Is DTE Energy's Debt?

As you can see below, at the end of March 2019, DTE Energy had US$14.4b of debt, up from US$12.9b a year ago. Click the image for more detail. Net debt is about the same, since the it doesn't have much cash.

How Strong Is DTE Energy's Balance Sheet?

The latest balance sheet data shows that DTE Energy had liabilities of US$3.65b due within a year, and liabilities of US$21.8b falling due after that. Offsetting this, it had US$56.0m in cash and US$1.76b in receivables that were due within 12 months. So its liabilities total US$23.6b more than the combination of its cash and short-term receivables.

When you consider that this deficiency exceeds the company's huge US$23.4b market capitalization, you might well be inclined to review the balance sheet, just like one might study a new partner's social media. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

DTE Energy has a rather high debt to EBITDA ratio of 5.7 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 2.9 times, suggesting it can responsibly service its obligations. Notably, DTE Energy's EBIT was pretty flat over the last year, which isn't ideal given the debt load. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine DTE Energy's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, DTE Energy recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for and improvement.

Our View

On the face of it, DTE Energy's conversion of EBIT to free cash flow left us tentative about the stock, and its net debt to EBITDA was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to grow its EBIT isn't such a worry. We should also note that Integrated Utilities industry companies like DTE Energy commonly do use debt without problems. Overall, it seems to us that DTE Energy's balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. Given our hesitation about the stock, it would be good to know if DTE Energy insiders have sold any shares recently. You click here to find out if insiders have sold recently.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:DTE

Solid track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor