Advertisement

Is China e-Wallet Payment Group (HKG:802) Using Debt Sensibly?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that China e-Wallet Payment Group Limited (HKG:802) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for China e-Wallet Payment Group

What Is China e-Wallet Payment Group's Net Debt?

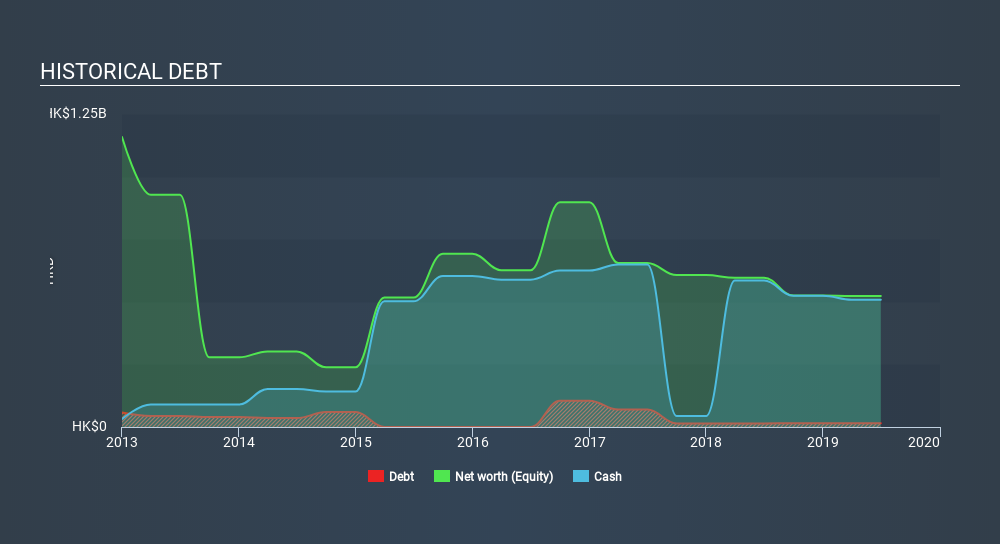

As you can see below, China e-Wallet Payment Group had HK$15.0m of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. But on the other hand it also has HK$508.2m in cash, leading to a HK$493.3m net cash position.

A Look At China e-Wallet Payment Group's Liabilities

The latest balance sheet data shows that China e-Wallet Payment Group had liabilities of HK$55.1m due within a year, and liabilities of HK$11.0m falling due after that. Offsetting this, it had HK$508.2m in cash and HK$43.9m in receivables that were due within 12 months. So it can boast HK$486.0m more liquid assets than total liabilities.

This surplus liquidity suggests that China e-Wallet Payment Group's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, it seems its balance sheet is as strong as a black-belt karate master. Simply put, the fact that China e-Wallet Payment Group has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is China e-Wallet Payment Group's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year China e-Wallet Payment Group wasn't profitable at an EBIT level, but managed to grow its revenue by21%, to HK$90m. With any luck the company will be able to grow its way to profitability.

So How Risky Is China e-Wallet Payment Group?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that China e-Wallet Payment Group had negative earnings before interest and tax (EBIT), over the last year. Indeed, in that time it burnt through HK$39m of cash and made a loss of HK$64m. But the saving grace is the HK$493.3m on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. China e-Wallet Payment Group's revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. For riskier companies like China e-Wallet Payment Group I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:802

China e-Wallet Payment Group

An investment holding company, primarily engages in the internet and mobile’s application, and related accessories business in Hong Kong and the People’s Republic of China.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor