Advertisement

In 2017, Zhiyong Zhang was appointed CEO of China Dongxiang (Group) Co., Ltd. (HKG:3818). First, this article will compare CEO compensation with compensation at similar sized companies. Next, we'll consider growth that the business demonstrates. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. The aim of all this is to consider the appropriateness of CEO pay levels.

See our latest analysis for China Dongxiang (Group)

How Does Zhiyong Zhang's Compensation Compare With Similar Sized Companies?

Our data indicates that China Dongxiang (Group) Co., Ltd. is worth HK$3.7b, and total annual CEO compensation was reported as CN¥3.2m for the year to March 2019. Notably, the salary of CN¥3.6m is the vast majority of the CEO compensation. We examined companies with market caps from CN¥1.4b to CN¥5.7b, and discovered that the median CEO total compensation of that group was CN¥2.6m.

Now let's take a look at the pay mix on an industry and company level to gain a better understanding of where China Dongxiang (Group) stands. On an industry level, roughly 90% of total compensation represents salary and 10.0% is other remuneration. So it seems like there isn't a significant difference between China Dongxiang (Group) and the broader market, in terms of salary allocation in the overall compensation package.

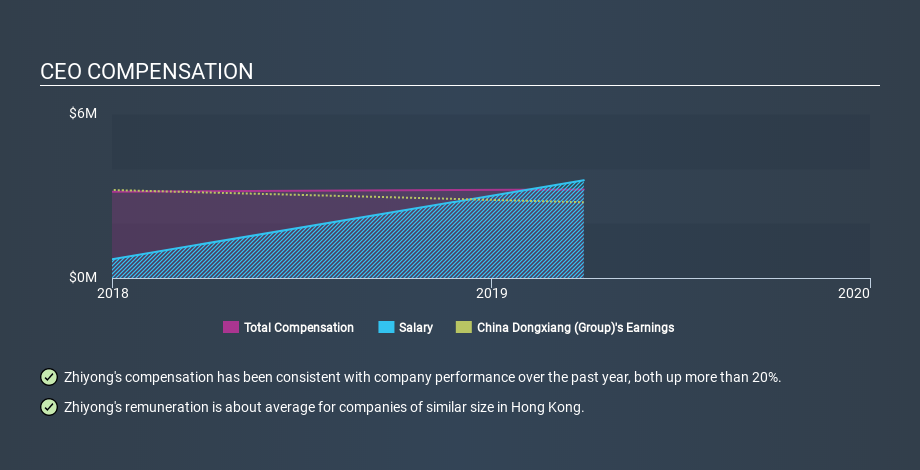

That means Zhiyong Zhang receives fairly typical remuneration for the CEO of a company that size. While this data point isn't particularly informative alone, it gains more meaning when considered with business performance. You can see a visual representation of the CEO compensation at China Dongxiang (Group), below.

Is China Dongxiang (Group) Co., Ltd. Growing?

China Dongxiang (Group) Co., Ltd. has reduced its earnings per share by an average of 18% a year, over the last three years (measured with a line of best fit). In the last year, its revenue is up 18%.

Sadly for shareholders, earnings per share are actually down, over three years. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that earnings per share has gone backwards over three years. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Shareholders might be interested in this free visualization of analyst forecasts.

Has China Dongxiang (Group) Co., Ltd. Been A Good Investment?

Since shareholders would have lost about 39% over three years, some China Dongxiang (Group) Co., Ltd. shareholders would surely be feeling negative emotions. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Remuneration for Zhiyong Zhang is close enough to the median pay for a CEO of a similar sized company .

The company isn't growing EPS, and shareholder returns have been disappointing. Suffice it to say, we don't think the CEO is underpaid! Shifting gears from CEO pay for a second, we've spotted 3 warning signs for China Dongxiang (Group) you should be aware of, and 1 of them shouldn't be ignored.

Important note: China Dongxiang (Group) may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About SEHK:3818

China Dongxiang (Group)

Engages in the design, development, and sale of sport-related apparel, footwear, and accessories in the People’s Republic of China and internationally.

Adequate balance sheet and overvalued.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1939.7% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6527.1% undervalued

41 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.6% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30155.3% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

ES

Esteban on Tyler Technologies ·

Tyler Technologies 04-2026

Fair Value:US$144.97107.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PittTheYounger on Erste Group Bank ·

An Austrian industry leader with attractive CEE exposure

Fair Value:€149.2323.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EU

European_Hidden_Gem_Stocks on Yü Group ·

Massive Cash Pile. Accelerating Growth. Is the Market Mispricing Yü Group?

Fair Value:UK£44.4263.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5451.0% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3462.5% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative