Advertisement

- New Zealand

- /

- REITS

- /

- NZSE:APL

Is Asset Plus Limited (NZSE:APL) A Good Dividend Stock?

Is Asset Plus Limited (NZSE:APL) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. Yet sometimes, investors buy a popular dividend stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

In this case, Asset Plus likely looks attractive to investors, given its 5.6% dividend yield and a payment history of over ten years. We'd guess that plenty of investors have purchased it for the income. Some simple research can reduce the risk of buying Asset Plus for its dividend - read on to learn more.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Asset Plus paid out 113% of its profit as dividends, over the trailing twelve month period. A payout ratio above 100% is definitely an item of concern, unless there are some other circumstances that would justify it.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. Asset Plus paid out 154% of its free cash flow last year, which we think is concerning if cash flows do not improve. Paying out more than 100% of your free cash flow in dividends is generally not a long-term, sustainable state of affairs, so we think shareholders should watch this metric closely. Cash is slightly more important than profit from a dividend perspective, but given Asset Plus's payouts were not well covered by either earnings or cash flow, we would definitely be concerned about the sustainability of this dividend.

Asset Plus is a REIT, which is an investment structure that often has different payout rules compared to other companies. It is not uncommon for REITs to pay out 100% of their earnings each year.

Is Asset Plus's Balance Sheet Risky?

As Asset Plus's dividend was not well covered by earnings, we need to check its balance sheet for signs of financial distress. A rough way to check this is with these two simple ratios: a) net debt divided by EBITDA (earnings before interest, tax, depreciation and amortisation), and b) net interest cover. Net debt to EBITDA is a measure of a company's total debt. Net interest cover measures the ability to meet interest payments. Essentially we check that a) the company does not have too much debt, and b) that it can afford to pay the interest. Asset Plus has net debt of 1.26 times its EBITDA, which is generally an okay level of debt for most companies.

We calculated its interest cover by measuring its earnings before interest and tax (EBIT), and dividing this by the company's net interest expense. Net interest cover of 7.81 times its interest expense appears reasonable for Asset Plus, although we're conscious that even high interest cover doesn't make a company bulletproof. That said, Asset Plus is in the real estate business, which is typically able to sustain much higher levels of debt, relative to other industries.

Dividend Volatility

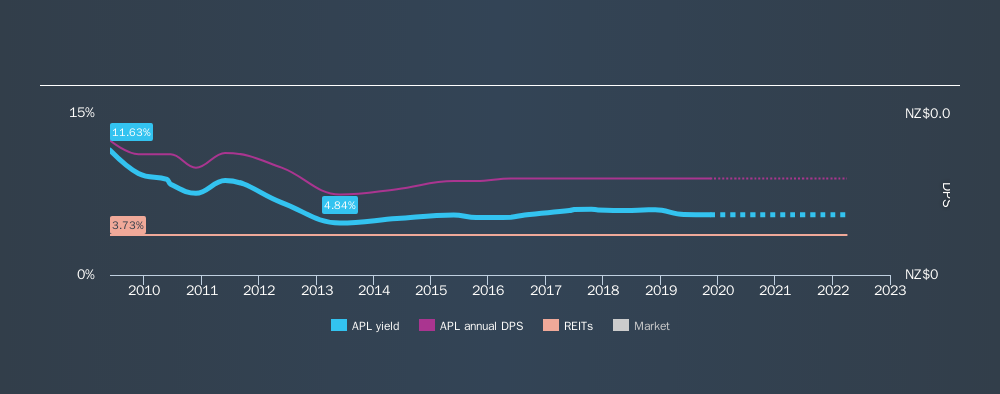

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. For the purpose of this article, we only scrutinise the last decade of Asset Plus's dividend payments. This dividend has been unstable, which we define as having fallen by at least 20% one or more times over this time. During the past ten-year period, the first annual payment was NZ$0.05 in 2009, compared to NZ$0.036 last year. This works out to be a decline of approximately 3.3% per year over that time. Asset Plus's dividend has been cut sharply at least once, so it hasn't fallen by 3.3% every year, but this is a decent approximation of the long term change.

We struggle to make a case for buying Asset Plus for its dividend, given that payments have shrunk over the past ten years.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share (EPS) are growing. Why take the risk of a dividend getting cut, unless there's a good chance of bigger dividends in future? Asset Plus's earnings per share have shrunk at 13% a year over the past five years. With this kind of significant decline, we always wonder what has changed in the business. Dividends are about stability, and Asset Plus's earnings per share, which support the dividend, have been anything but stable.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. It's a concern to see that the company paid out such a high percentage of its earnings and cashflow as dividends. Earnings per share are down, and Asset Plus's dividend has been cut at least once in the past, which is disappointing. In this analysis, Asset Plus doesn't shape up too well as a dividend stock. We'd find it hard to look past the flaws, and would not be inclined to think of it as a reliable dividend-payer.

You can also discover whether shareholders are aligned with insider interests by checking our visualisation of insider shareholdings and trades in Asset Plus stock.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NZSE:APL

Asset Plus

NPT Limited operates as a property company.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

66 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

EV

everyseed on Zylox-Tonbridge Medical Technology ·

Zylox-Tonbridge: Early Signs of an Emerging Global Vascular Intervention Platform

Fair Value:HK$30.8539.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.7460.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on CSL ·

Strong buy. World-leading healthcare company with steady growth

Fair Value:AU$143.1519.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative