Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:AAPL

Is Apple Inc. (NASDAQ:AAPL) Potentially Undervalued?

Apple Inc. (NASDAQ:AAPL) led the NASDAQGS gainers with a relatively large price hike in the past couple of weeks. As a large-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. However, what if the stock is still a bargain? Let’s examine Apple’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

See our latest analysis for Apple

What is Apple worth?

According to my valuation model, the stock is currently overvalued by about 40%, trading at US$383 compared to my intrinsic value of $273.26. This means that the buying opportunity has probably disappeared for now. If you like the stock, you may want to keep an eye out for a potential price decline in the future. Given that Apple’s share is fairly volatile (i.e. its price movements are magnified relative to the rest of the market) this could mean the price can sink lower, giving us another chance to buy in the future. This is based on its high beta, which is a good indicator for share price volatility.

Can we expect growth from Apple?

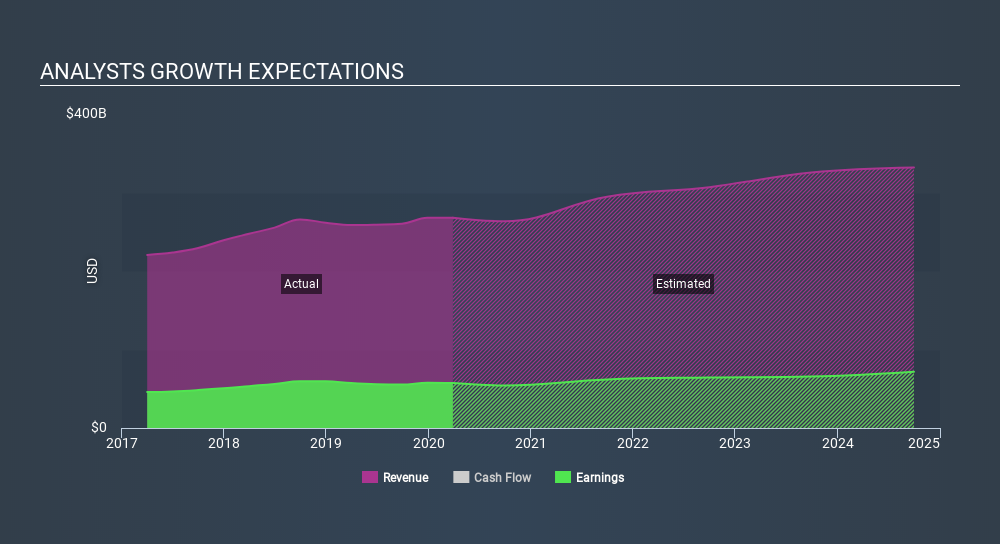

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. With profit expected to grow by a double-digit 14% over the next couple of years, the outlook is positive for Apple. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? It seems like the market has well and truly priced in AAPL’s positive outlook, with shares trading above its fair value. However, this brings up another question – is now the right time to sell? If you believe AAPL should trade below its current price, selling high and buying it back up again when its price falls towards its real value can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on AAPL for some time, now may not be the best time to enter into the stock. The price has surpassed its true value, which means there’s no upside from mispricing. However, the optimistic prospect is encouraging for AAPL, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Apple. You can find everything you need to know about Apple in the latest infographic research report. If you are no longer interested in Apple, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

When trading Apple or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGS:AAPL

Apple

Designs, manufactures, and markets smartphones, personal computers, tablets, wearables, and accessories worldwide.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

63 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

17 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on HealthCo Healthcare and Wellness REIT ·

The Discount Is Real — But Only If You Price the Exit, Not the Balance Sheet

Fair Value:AU$1.0733.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on Netflix ·

Netflix's Attention Deficit: Pricing and Ads Racing Against View-Hour Stagnation

Fair Value:US$7710.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Silver Storm Mining ·

Silver Storm Mining, 34 Million Oz Produced, Now Targeting Q2 2026 Restart

Fair Value:CA$8.8495.5% undervalued

13 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

63 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0