Advertisement

- India

- /

- Consumer Durables

- /

- NSEI:BUTTERFLY

Introducing Butterfly Gandhimathi Appliances (NSE:BUTTERFLY), A Stock That Climbed 44% In The Last Year

These days it's easy to simply buy an index fund, and your returns should (roughly) match the market. But if you pick the right individual stocks, you could make more than that. To wit, the Butterfly Gandhimathi Appliances Limited (NSE:BUTTERFLY) share price is 44% higher than it was a year ago, much better than the market return of around 8.2% (not including dividends) in the same period. If it can keep that out-performance up over the long term, investors will do very well! However, the stock hasn't done so well in the longer term, with the stock only up 13% in three years.

Check out our latest analysis for Butterfly Gandhimathi Appliances

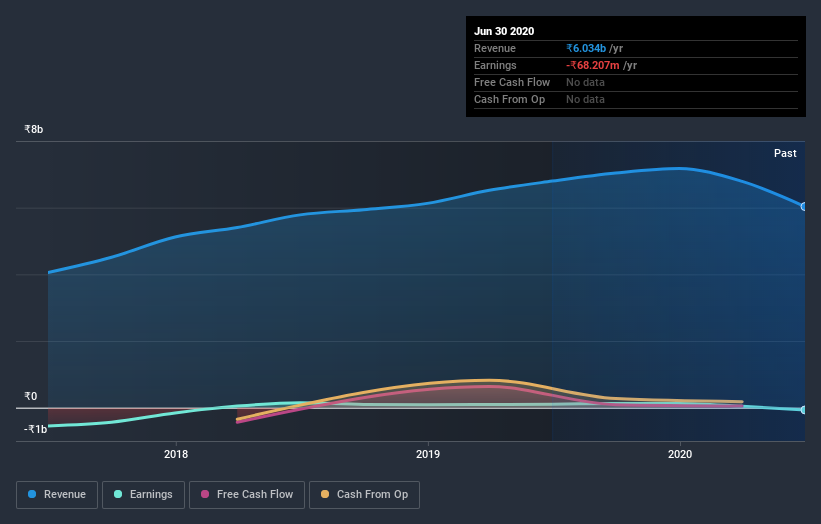

Butterfly Gandhimathi Appliances wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. When a company doesn't make profits, we'd generally expect to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

Butterfly Gandhimathi Appliances actually shrunk its revenue over the last year, with a reduction of 11%. Despite the lack of revenue growth, the stock has returned a solid 44% the last twelve months. We can correlate the share price rise with revenue or profit growth, but it seems the market had previously expected weaker results, and sentiment around the stock is improving.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

A Different Perspective

It's nice to see that Butterfly Gandhimathi Appliances shareholders have received a total shareholder return of 44% over the last year. That's better than the annualised return of 7.6% over half a decade, implying that the company is doing better recently. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. It's always interesting to track share price performance over the longer term. But to understand Butterfly Gandhimathi Appliances better, we need to consider many other factors. For instance, we've identified 3 warning signs for Butterfly Gandhimathi Appliances (1 is potentially serious) that you should be aware of.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on IN exchanges.

When trading Butterfly Gandhimathi Appliances or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Butterfly Gandhimathi Appliances might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:BUTTERFLY

Butterfly Gandhimathi Appliances

Engages in the manufacture and sale of domestic kitchen and electrical appliances under the Butterfly brand name in India and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.2% undervalued

TO

Community Contributor