Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Interpump Group S.p.A. (BIT:IP) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Interpump Group

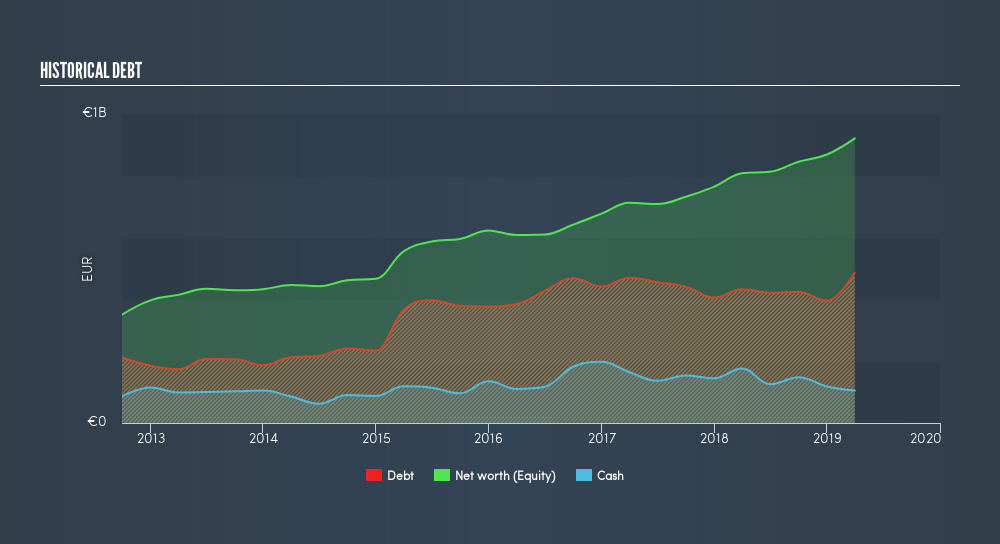

What Is Interpump Group's Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Interpump Group had €486.4m of debt, an increase on €432.7m, over one year. However, because it has a cash reserve of €104.8m, its net debt is less, at about €381.6m.

A Look At Interpump Group's Liabilities

According to the last reported balance sheet, Interpump Group had liabilities of €489.5m due within 12 months, and liabilities of €400.5m due beyond 12 months. Offsetting this, it had €104.8m in cash and €330.3m in receivables that were due within 12 months. So its liabilities total €454.9m more than the combination of its cash and short-term receivables.

Given Interpump Group has a market capitalization of €2.73b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Interpump Group has a low net debt to EBITDA ratio of only 1.3. And its EBIT easily covers its interest expense, being 68.3 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Also good is that Interpump Group grew its EBIT at 17% over the last year, further increasing its ability to manage debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Interpump Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Interpump Group's free cash flow amounted to 43% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

The good news is that Interpump Group's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its EBIT growth rate also supports that impression! Looking at all the aforementioned factors together, it strikes us that Interpump Group can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. We'd be motivated to research the stock further if we found out that Interpump Group insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About BIT:IP

Interpump Group

Engages in the manufacturing and selling of high-pressure pumps in Italy, rest of Europe, North America, the Far East and the Pacific Area, and internationally.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2537.9% undervalued

148 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0327.9% undervalued

33 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.521.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.726.3% undervalued

42 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Argenta Silver ·

Frank Giustra Backed: The High-Grade Silver Project Acquired for Just $3.5M Could Deliver 30x Silver Torque

Fair Value:CA$40.3598.8% undervalued

16 followersusers have followed this narrative

9 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HU

Hunter_Z on Oriental Kopi Holdings Berhad ·

Oriental Kopi's Indonesia JV Strengthens Regional Growth Narrative

Fair Value:RM 1.533.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on UCB ·

FV 206,24 but with a 310-154 range...to discuss

Fair Value:€206.249.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28021.8% undervalued

264 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.0% overvalued

129 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.7% undervalued

160 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0