Advertisement

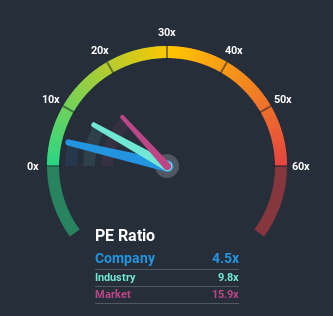

When close to half the companies in France have price-to-earnings ratios (or "P/E's") above 16x, you may consider Groupimo S.A. (EPA:ALIMO) as a highly attractive investment with its 4.5x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Earnings have risen firmly for Groupimo recently, which is pleasing to see. It might be that many expect the respectable earnings performance to degrade substantially, which has repressed the P/E. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

Check out our latest analysis for Groupimo

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Groupimo would need to produce anemic growth that's substantially trailing the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 16% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 29% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

This is in contrast to the rest of the market, which is expected to decline by 6.4% over the next year, or less than the company's recent medium-term annualised earnings decline.

With this information, it's not too hard to see why Groupimo is trading at a lower P/E in comparison. Nonetheless, with earnings going quickly in reverse, it's not guaranteed that the P/E has found a floor yet. Even just maintaining these prices will be difficult to achieve as recent earnings trends are already weighing down the shares heavily.

What We Can Learn From Groupimo's P/E?

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Groupimo revealed its sharp three-year contraction in earnings is contributing to its low P/E, given the market is set to shrink less severely. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. However, we're still cautious about the company's ability to prevent an acceleration of its recent medium-term course and resist even greater pain to its business from the broader market turmoil. In the meantime, unless the company's relative performance improves, the share price will hit a barrier around these levels.

We don't want to rain on the parade too much, but we did also find 4 warning signs for Groupimo (2 are a bit unpleasant!) that you need to be mindful of.

If these risks are making you reconsider your opinion on Groupimo, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you’re looking to trade Groupimo, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ENXTPA:ALIMO

Excellent balance sheet moderate.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor