- United States

- /

- Machinery

- /

- NYSE:IR

Ingersoll Rand (IR) Eyes M&A With Strong Balance Sheet Despite US$115 Million Q2 Loss

Reviewed by Simply Wall St

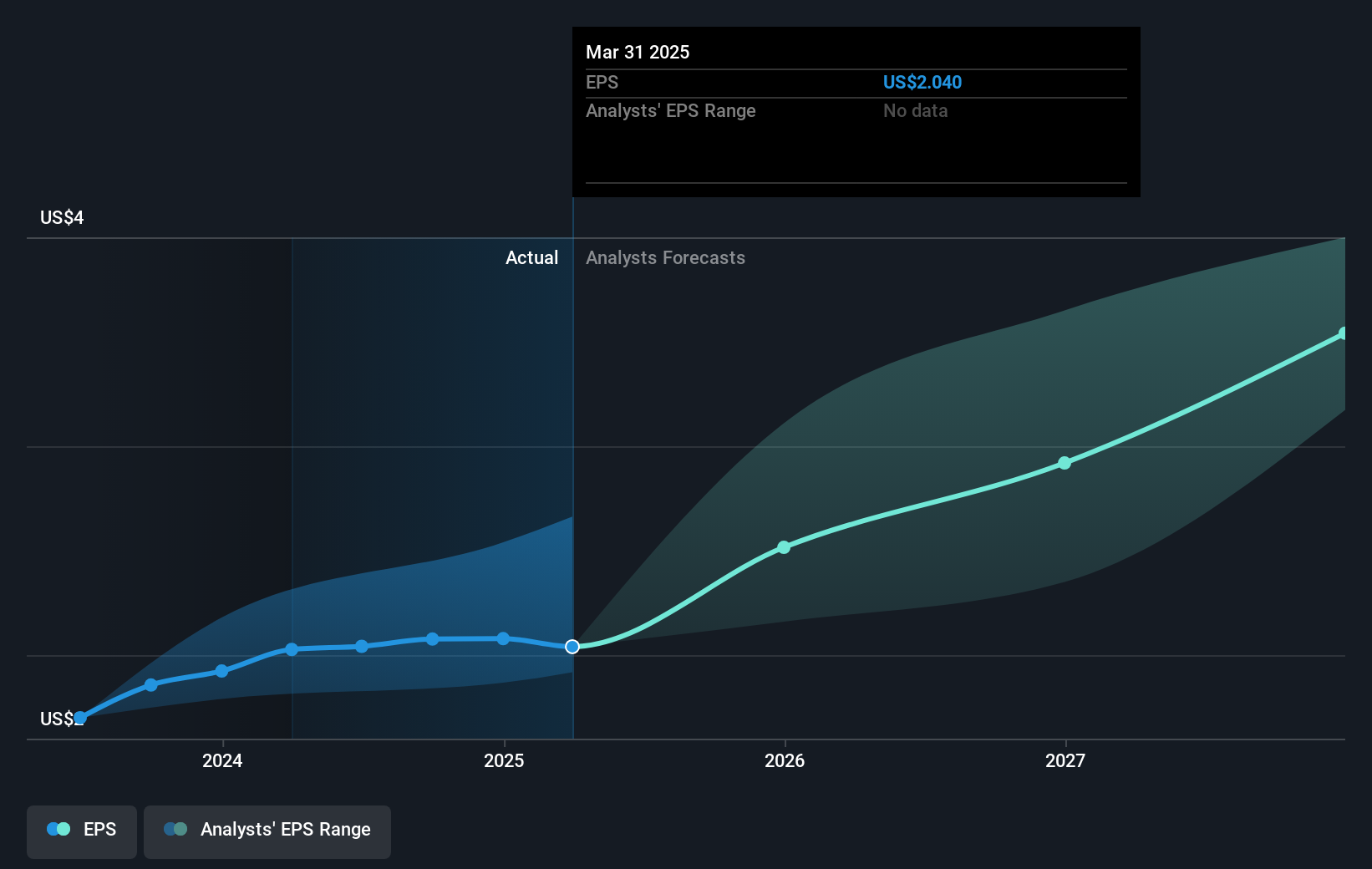

Ingersoll Rand (IR) announced a second-quarter sales increase to $1,888 million, but reported a net loss of $115 million, which influenced its stock price movement. Despite the company's revised revenue guidance indicating modest growth, its focus on mergers and acquisitions, highlighted by an accelerated $500 million share repurchase, could have added weight to the stock's 10% rise over the last quarter. Meanwhile, broader market trends, including declines due to new tariff concerns and weak job reports, might have countered some of these positive impulses, affecting investor sentiment toward Ingersoll Rand.

You should learn about the 1 possible red flag we've spotted with Ingersoll Rand.

The recent announcements from Ingersoll Rand could significantly influence the company's long-term growth narrative. The focus on mergers and acquisitions, alongside a $500 million share repurchase, underscores a commitment to enhancing shareholder returns. These moves might support the future revenue and earnings forecasts by providing additional growth channels and potentially improved profit margins through increased economies of scale and operational efficiencies. However, the reported net loss of $115 million could caution investors about the risks inherent in such strategies, particularly the challenges in successfully integrating acquisitions.

Ingersoll Rand's shares have shown substantial growth over a longer span, achieving a total return of 157.32% over the past five years. This performance reflects the company's capability to deliver consistent results and might appeal to investors looking for historical stability in returns. In contrast, over the past year, the company's stock underperformed the broader US Market's 15.7% return, which may raise questions about its immediate competitive positioning within the industry.

With the current share price of $84.63 versus a consensus price target of $93.47, there is a 10.44% discount, suggesting potential for future appreciation if analysts' projections materialize. This discount reflects a cautious optimism, with the market yet to be fully convinced by the projected growth targets. The ability of Ingersoll Rand to meet or exceed those expectations will likely hinge on the successful integration of acquisitions and the execution of its cost-efficiency strategies, especially in light of broader market challenges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:IR

Ingersoll Rand

Provides various mission-critical air, fluid, energy, and medical technologies services and solutions worldwide.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives