Advertisement

- United States

- /

- Software

- /

- NasdaqGS:PRGS

How Should Investors React To Progress Software's (NASDAQ:PRGS) CEO Pay?

Yogesh Gupta has been the CEO of Progress Software Corporation (NASDAQ:PRGS) since 2016, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also assess whether Progress Software pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

View our latest analysis for Progress Software

Comparing Progress Software Corporation's CEO Compensation With the industry

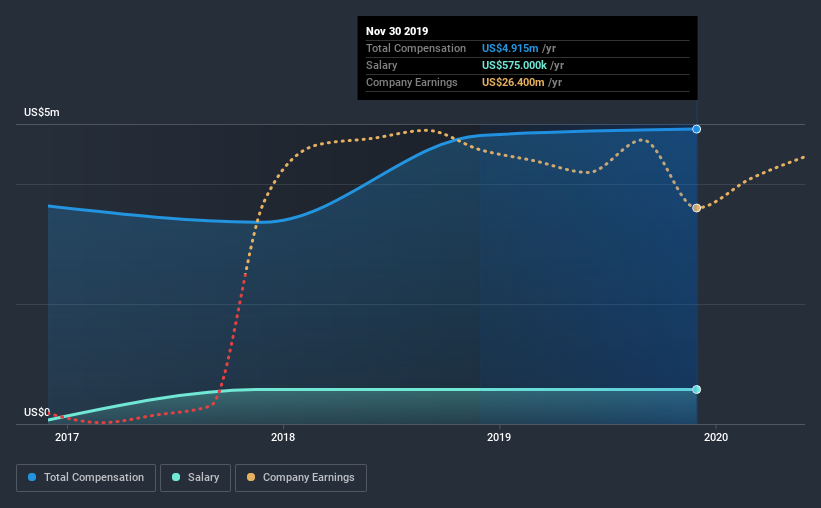

At the time of writing, our data shows that Progress Software Corporation has a market capitalization of US$1.7b, and reported total annual CEO compensation of US$4.9m for the year to November 2019. That's mostly flat as compared to the prior year's compensation. While we always look at total compensation first, our analysis shows that the salary component is less, at US$575k.

On comparing similar companies from the same industry with market caps ranging from US$1.0b to US$3.2b, we found that the median CEO total compensation was US$4.5m. This suggests that Progress Software remunerates its CEO largely in line with the industry average. Furthermore, Yogesh Gupta directly owns US$3.5m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$575k | US$575k | 12% |

| Other | US$4.3m | US$4.2m | 88% |

| Total Compensation | US$4.9m | US$4.8m | 100% |

On an industry level, roughly 11% of total compensation represents salary and 89% is other remuneration. There isn't a significant difference between Progress Software and the broader market, in terms of salary allocation in the overall compensation package. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Progress Software Corporation's Growth

Progress Software Corporation's earnings per share (EPS) grew 49% per year over the last three years. It achieved revenue growth of 14% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Progress Software Corporation Been A Good Investment?

Progress Software Corporation has served shareholders reasonably well, with a total return of 15% over three years. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

To Conclude...

As we touched on above, Progress Software Corporation is currently paying a compensation that's close to the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. But EPS growth over the last three years has been impressive, although the same cannot be said for shareholder returns. As a result of these considerations, we would suggest the compensation is reasonable, but looking ahead shareholders will likely want to see healthier returns.

CEO compensation can have a massive impact on performance, but it's just one element. We've identified 3 warning signs for Progress Software that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading Progress Software or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGS:PRGS

Progress Software

Develops, deploys, and manages artificial intelligence (AI) powered applications and digital experiences in the United States and internationally.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor