Advertisement

- France

- /

- Commercial Services

- /

- ENXTPA:ALDLT

How Much is Delta Plus Group's (EPA:DLTA) CEO Getting Paid?

The CEO of Delta Plus Group (EPA:DLTA) is Jérôme Benoit. This analysis aims first to contrast CEO compensation with other companies that have similar market capitalization. Then we'll look at a snap shot of the business growth. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. This method should give us information to assess how appropriately the company pays the CEO.

Check out our latest analysis for Delta Plus Group

How Does Jérôme Benoit's Compensation Compare With Similar Sized Companies?

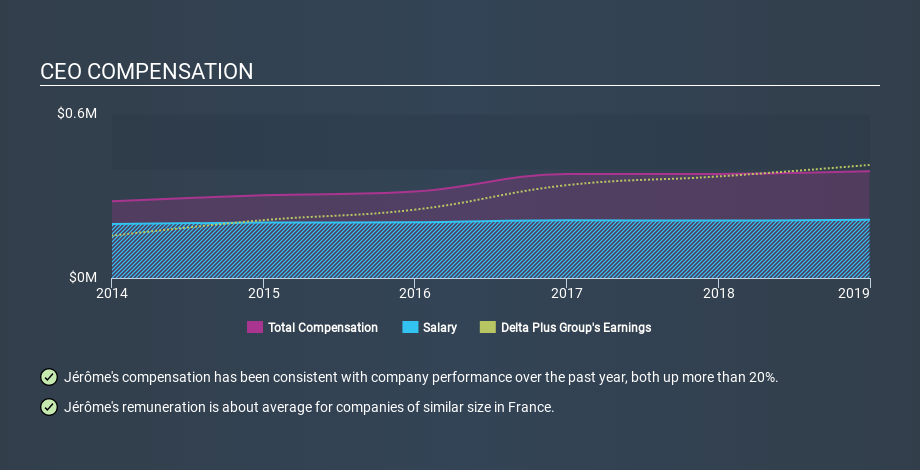

At the time of writing, our data says that Delta Plus Group has a market cap of €281m, and reported total annual CEO compensation of €390k for the year to December 2018. We think total compensation is more important but we note that the CEO salary is lower, at €213k. As part of our analysis we looked at companies in the same jurisdiction, with market capitalizations of €178m to €711m. The median total CEO compensation was €487k.

Next, let's break down remuneration compositions to understand how the industry and company compare with each other. Speaking on an industry level, we can see that nearly 73% of total compensation represents salary, while the remainder of 27% is other remuneration. So it seems like there isn't a significant difference between Delta Plus Group and the broader market, in terms of salary allocation in the overall compensation package.

That means Jérôme Benoit receives fairly typical remuneration for the CEO of a company that size. While this data point isn't particularly informative alone, it gains more meaning when considered with business performance. You can see a visual representation of the CEO compensation at Delta Plus Group, below.

Is Delta Plus Group Growing?

Over the last three years Delta Plus Group has seen earnings per share (EPS) move in a positive direction by an average of 15% per year (using a line of best fit). Its revenue is up 9.5% over last year.

This demonstrates that the company has been improving recently. A good result. It's nice to see a little revenue growth, as this is consistent with healthy business conditions. Shareholders might be interested in this free visualization of analyst forecasts.

Has Delta Plus Group Been A Good Investment?

Given the total loss of 8.7% over three years, many shareholders in Delta Plus Group are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Jérôme Benoit is paid around the same as most CEOs of similar size companies.

We think that the EPS growth is very pleasing, but we find the returns over the last three years to be lacking. We'd be surprised if shareholders want to see a pay rise for the CEO, but we'd stop short of calling their pay too generous. CEO compensation is an important area to keep your eyes on, but we've also identified 3 warning signs for Delta Plus Group (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

Important note: Delta Plus Group may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About ENXTPA:ALDLT

Delta Plus Group

Engages in design, manufacture, and distribution of a range of personal protective equipment worldwide.

Very undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4342.5% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7829.0% undervalued

32 followersusers have followed this narrative

6 commentsusers have commented on this narrative

19 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1752.7% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6435.3% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

JU

JuanVargas on Promigas E.S.P ·

Promigas E.S.P looks to a promising future with 35% revenue growth

Fair Value:Col$13.26k51.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Kratos Defense & Security Solutions ·

Kratos Defense & Security Solutions (KTOS): Scaling "Attritable" Dominance in a New Era of Aerial Conflict.

Fair Value:US$11821.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on BWX Technologies ·

BWX Technologies (BWXT): Powering the Nuclear Renaissance from Naval Depths to Medical Frontiers.

Fair Value:US$205.22.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.3% undervalued

1305 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative