Advertisement

- Sweden

- /

- Specialty Stores

- /

- OM:BILI A

How Does Bilia AB (publ)'s (STO:BILI A) Earnings Growth Stack Up Against Industry Performance?

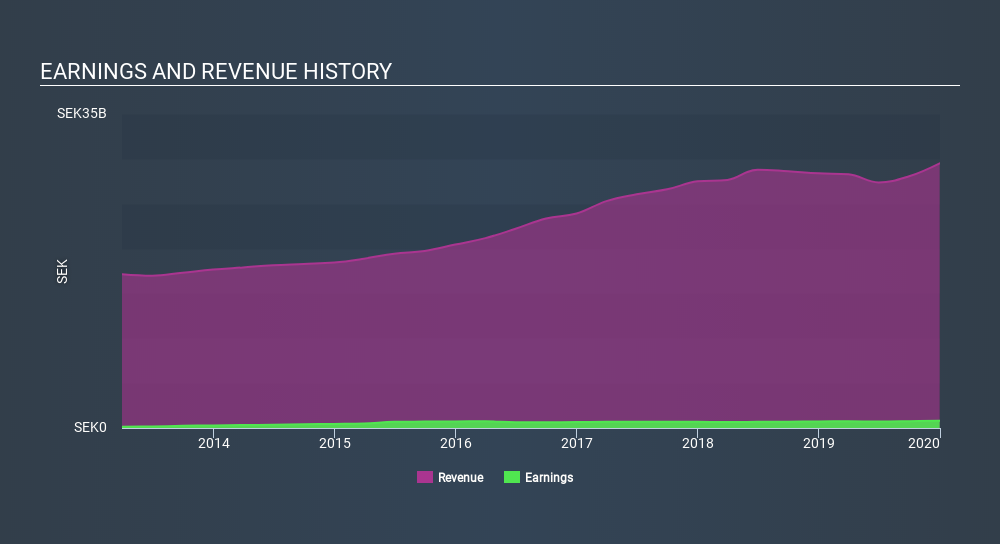

After reading Bilia AB (publ)'s (OM:BILI A) latest earnings update (31 December 2019), I found it beneficial to look back at how the company has performed in the past and compare this against the most recent numbers. As a long-term investor I tend to pay attention to earnings trend, rather than a single number at one point in time. I also like to compare against an industry benchmark to understand whether BILI A has outperformed, or whether it is simply riding an industry wave. Below is a brief commentary on my key takeaways.

See our latest analysis for Bilia

Did BILI A's recent earnings growth beat the long-term trend and the industry?

BILI A's trailing twelve-month earnings (from 31 December 2019) of kr807m has increased by 9.9% compared to the previous year.

Furthermore, this one-year growth rate has exceeded its 5-year annual growth average of 4.9%, indicating the rate at which BILI A is growing has accelerated. What's the driver of this growth? Well, let’s take a look at if it is merely because of an industry uplift, or if Bilia has seen some company-specific growth.

In terms of returns from investment, Bilia has invested its equity funds well leading to a 25% return on equity (ROE), above the sensible minimum of 20%. Furthermore, its return on assets (ROA) of 6.0% exceeds the SE Specialty Retail industry of 5.5%, indicating Bilia has used its assets more efficiently. However, its return on capital (ROC), which also accounts for Bilia’s debt level, has declined over the past 3 years from 15% to 12%. This correlates with an increase in debt holding, with debt-to-equity ratio rising from 2.8% to 80% over the past 5 years.

What does this mean?

Bilia's track record can be a valuable insight into its earnings performance, but it certainly doesn't tell the whole story. Companies that have performed well in the past, such as Bilia gives investors conviction. However, the next step would be to assess whether the future looks as optimistic. You should continue to research Bilia to get a better picture of the stock by looking at:

- Financial Health: Are BILI A’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

- Valuation: What is BILI A worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether BILI A is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 31 December 2019. This may not be consistent with full year annual report figures.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OM:BILI A

Bilia

Operates as a full-service supplier for car ownership in Sweden, Norway, Luxemburg, and Belgium.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor