Advertisement

- Italy

- /

- Energy Services

- /

- BIT:SPM

Here's Why We Think Saipem's (BIT:SPM) Statutory Earnings Might Be Conservative

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. That said, the current statutory profit is not always a good guide to a company's underlying profitability. This article will consider whether Saipem's (BIT:SPM) statutory profits are a good guide to its underlying earnings.

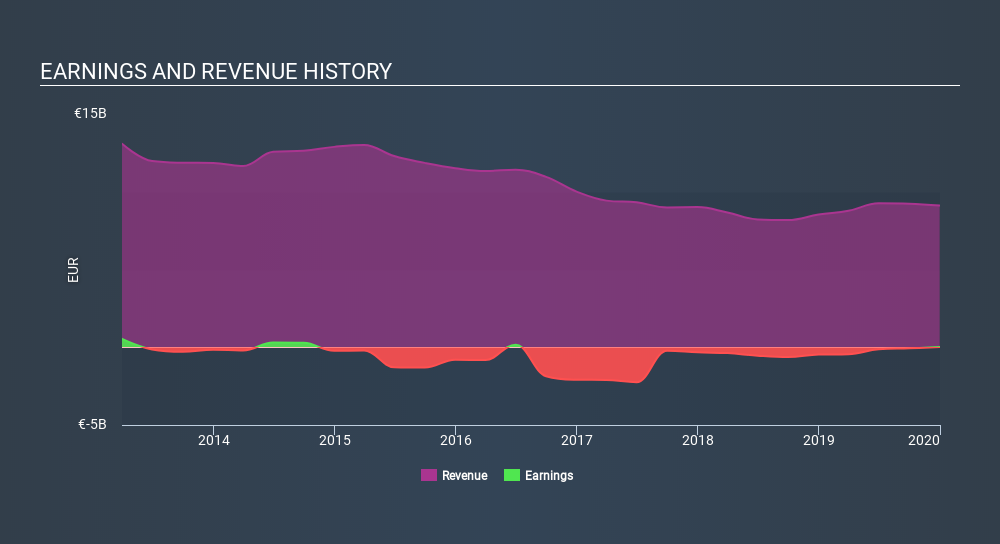

While Saipem was able to generate revenue of €9.11b in the last twelve months, we think its profit result of €12.0m was more important. The chart below shows that while revenue has fallen over the last three years, the company has moved from unprofitable to profitable.

Check out our latest analysis for Saipem

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. As a result, today we're going to take a closer look at Saipem's cashflow, and unusual items, with a view to understanding what these might tell us about its statutory profit. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

A Closer Look At Saipem's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

For the year to December 2019, Saipem had an accrual ratio of -0.23. That indicates that its free cash flow quite significantly exceeded its statutory profit. Indeed, in the last twelve months it reported free cash flow of €921m, well over the €12.0m it reported in profit. Saipem shareholders are no doubt pleased that free cash flow improved over the last twelve months. However, that's not all there is to consider. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part.

The Impact Of Unusual Items On Profit

Saipem's profit was reduced by unusual items worth €91m in the last twelve months, and this helped it produce high cash conversion, as reflected by its unusual items. This is what you'd expect to see where a company has a non-cash charge reducing paper profits. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. Assuming those unusual expenses don't come up again, we'd therefore expect Saipem to produce a higher profit next year, all else being equal.

Our Take On Saipem's Profit Performance

In conclusion, both Saipem's accrual ratio and its unusual items suggest that its statutory earnings are probably reasonably conservative. Based on these factors, we think Saipem's underlying earnings potential is as good as, or probably even better, than the statutory profit makes it seem! If you'd like to know more about Saipem as a business, it's important to be aware of any risks it's facing. In terms of investment risks, we've identified 2 warning signs with Saipem, and understanding them should be part of your investment process.

After our examination into the nature of Saipem's profit, we've come away optimistic for the company. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About BIT:SPM

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|4.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor