Advertisement

Here's Why We Think Kancelaria Medius's (WSE:KME) Statutory Earnings Might Be Conservative

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. This article will consider whether Kancelaria Medius's (WSE:KME) statutory profits are a good guide to its underlying earnings.

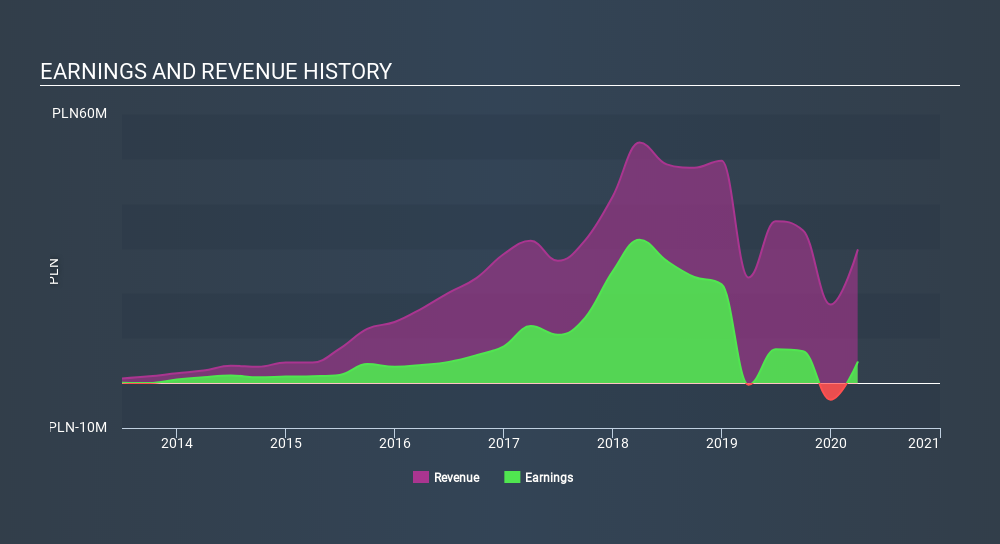

We like the fact that Kancelaria Medius made a profit of zł4.65m on its revenue of zł29.7m, in the last year.

View our latest analysis for Kancelaria Medius

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. As a result, we think it's well worth considering what Kancelaria Medius's cashflow (when compared to its earnings) can tell us about the nature of its statutory profit. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Kancelaria Medius.

Examining Cashflow Against Kancelaria Medius's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to March 2020, Kancelaria Medius had an accrual ratio of -1.73. Therefore, its statutory earnings were very significantly less than its free cashflow. In fact, it had free cash flow of zł22m in the last year, which was a lot more than its statutory profit of zł4.65m. Kancelaria Medius's free cash flow improved over the last year, which is generally good to see.

Our Take On Kancelaria Medius's Profit Performance

Happily for shareholders, Kancelaria Medius produced plenty of free cash flow to back up its statutory profit numbers. Because of this, we think Kancelaria Medius's underlying earnings potential is as good as, or possibly even better, than the statutory profit makes it seem! And one can definitely find a positive in the fact that it made a profit this year, despite losing money last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. If you'd like to know more about Kancelaria Medius as a business, it's important to be aware of any risks it's facing. Every company has risks, and we've spotted 3 warning signs for Kancelaria Medius (of which 2 can't be ignored!) you should know about.

Today we've zoomed in on a single data point to better understand the nature of Kancelaria Medius's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor