Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Nico Steel Holdings Limited (SGX:5GF) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Nico Steel Holdings

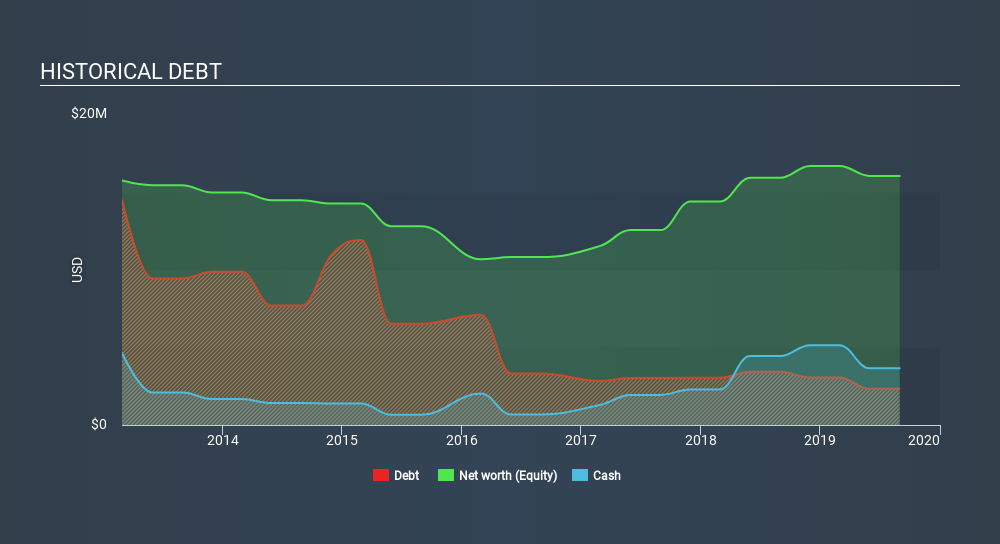

What Is Nico Steel Holdings's Debt?

The image below, which you can click on for greater detail, shows that at August 2019 Nico Steel Holdings had debt of US$2.33m, up from US$3.4 in one year. But it also has US$3.65m in cash to offset that, meaning it has US$1.32m net cash.

How Strong Is Nico Steel Holdings's Balance Sheet?

According to the last reported balance sheet, Nico Steel Holdings had liabilities of US$3.69m due within 12 months, and liabilities of US$140.0k due beyond 12 months. Offsetting this, it had US$3.65m in cash and US$5.53m in receivables that were due within 12 months. So it can boast US$5.35m more liquid assets than total liabilities.

This excess liquidity is a great indication that Nico Steel Holdings's balance sheet is just as strong as racists are weak. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that Nico Steel Holdings has more cash than debt is arguably a good indication that it can manage its debt safely.

Shareholders should be aware that Nico Steel Holdings's EBIT was down 69% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Nico Steel Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Nico Steel Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last two years, Nico Steel Holdings saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Nico Steel Holdings has net cash of US$1.32m, as well as more liquid assets than liabilities. So although we see some areas for improvement, we're not too worried about Nico Steel Holdings's balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Nico Steel Holdings is showing 4 warning signs in our investment analysis , and 1 of those is a bit concerning...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor