Advertisement

- Australia

- /

- Retail REITs

- /

- ASX:WPR

Here's What You Should Know About Viva Energy REIT's (ASX:VVR) 5.2% Dividend Yield

Is Viva Energy REIT (ASX:VVR) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. Yet sometimes, investors buy a popular dividend stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

Viva Energy REIT yields a solid 5.2%, although it has only been paying for three years. A 5.2% yield does look good. Could the short payment history hint at future dividend growth? Some simple analysis can offer a lot of insights when buying a company for its dividend, and we'll go through this below.

Explore this interactive chart for our latest analysis on Viva Energy REIT!

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Viva Energy REIT paid out 133% of its profit as dividends, over the trailing twelve month period. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. With a cash payout ratio of 133%, Viva Energy REIT's dividend payments are poorly covered by cash flow. Paying out more than 100% of your free cash flow in dividends is generally not a long-term, sustainable state of affairs, so we think shareholders should watch this metric closely. Cash is slightly more important than profit from a dividend perspective, but given Viva Energy REIT's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

REITs like Viva Energy REIT often have different rules governing their distributions, so a higher payout ratio on its own is not unusual.

Dividend Volatility

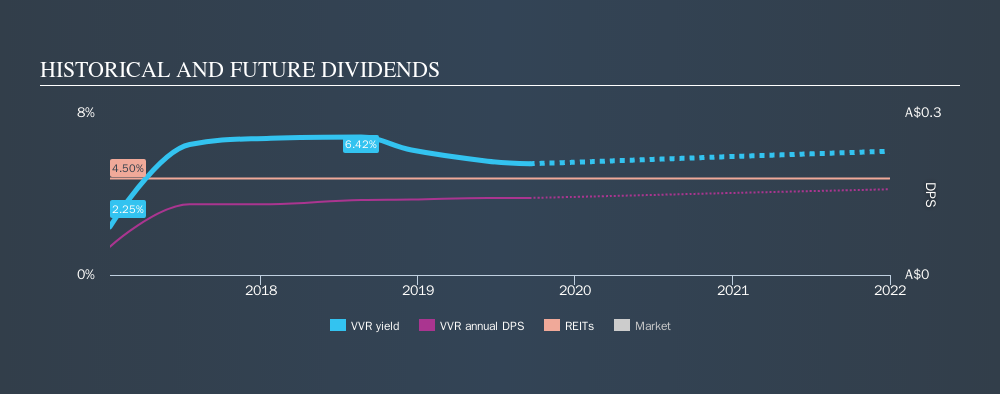

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. The company has been paying a stable dividend for a few years now, but we'd like to see more evidence of consistency over a longer period. During the past three-year period, the first annual payment was AU$0.053 in 2016, compared to AU$0.14 last year. This works out to be a compound annual growth rate (CAGR) of approximately 40% a year over that time.

Viva Energy REIT has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term. Strong earnings per share (EPS) growth might encourage our interest in the company despite fluctuating dividends, which is why it's great to see Viva Energy REIT has grown its earnings per share at 138% per annum over the past five years. Earnings per share have been growing very rapidly, although the company is also paying out virtually all of its profit in dividends. While EPS could grow fast enough to make the dividend sustainable, in this type of situation, we'd want to pay extra attention to any fragilities in the company's balance sheet.

We'd also point out that Viva Energy REIT issued a meaningful number of new shares in the past year. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. We're a bit uncomfortable with Viva Energy REIT paying out a high percentage of both its cashflow and earnings. Next, earnings growth has been good, but unfortunately the company has not been paying dividends as long as we'd like. In summary, Viva Energy REIT has a number of shortcomings that we'd find it hard to get past. Things could change, but we think there are a number of better ideas out there.

Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 3 analysts we track are forecasting for Viva Energy REIT for free with public analyst estimates for the company.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:WPR

Waypoint REIT

Waypoint REIT is Australia’s largest listed REIT owning solely fuel and convenience retail properties; it has a high-quality network across all Australian States and mainland Territories.

Undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor