Advertisement

GW Pharmaceuticals plc (NASDAQ:GWPH): Are Analysts Optimistic?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

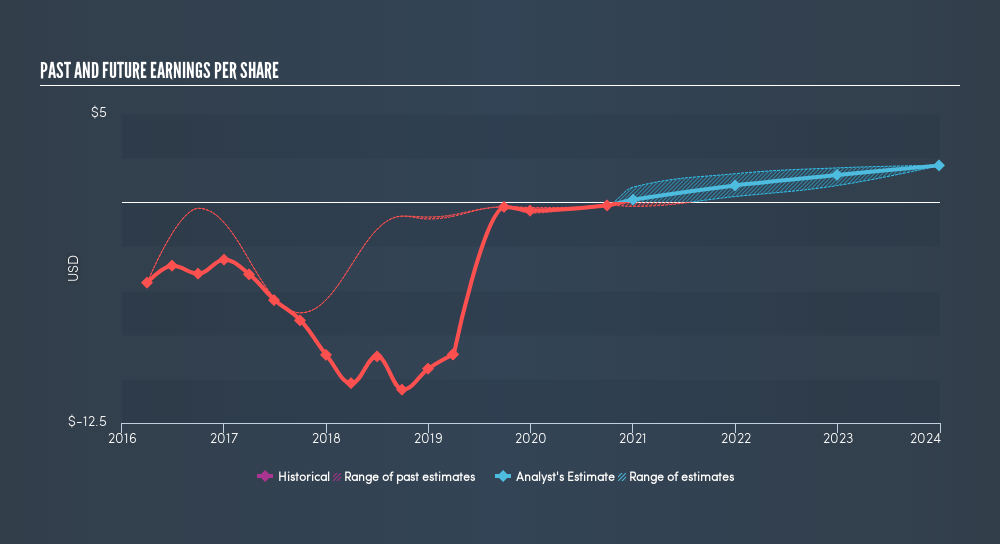

GW Pharmaceuticals plc's (NASDAQ:GWPH): GW Pharmaceuticals plc, a biopharmaceutical company, focuses on discovering, developing, and commercializing cannabinoid prescription medicines using botanical extracts derived from the Cannabis plant. The US$5.6b market-cap company’s loss lessens since it announced a -US$287.6m bottom-line in the full financial year, compared to the latest trailing-twelve-month loss of -US$268.2m, as it approaches breakeven. Many investors are wondering the rate at which GWPH will turn a profit, with the big question being “when will the company breakeven?” I’ve put together a brief outline of industry analyst expectations for GWPH, its year of breakeven and its implied growth rate.

View our latest analysis for GW Pharmaceuticals

According to the 11 industry analysts covering GWPH, the consensus is breakeven is near. They anticipate the company to incur a final loss in 2019, before generating positive profits of US$11m in 2020. So, GWPH is predicted to breakeven approximately a few months from now. How fast will GWPH have to grow each year in order to reach the breakeven point by 2020? Working backwards from analyst estimates, it turns out that they expect the company to grow 83% year-on-year, on average, which is extremely buoyant. If this rate turns out to be too aggressive, GWPH may become profitable much later than analysts predict.

Underlying developments driving GWPH’s growth isn’t the focus of this broad overview, though, take into account that by and large pharmaceuticals, depending on the stage of product development, have irregular periods of cash flow. This means that a high growth rate is not unusual, especially if the company is currently in an investment period.

Before I wrap up, there’s one aspect worth mentioning. GWPH has managed its capital prudently, with debt making up 5.8% of equity. This means that GWPH has predominantly funded its operations from equity capital,and its low debt obligation reduces the risk around investing in the loss-making company.

Next Steps:

There are too many aspects of GWPH to cover in one brief article, but the key fundamentals for the company can all be found in one place – GWPH’s company page on Simply Wall St. I’ve also compiled a list of key factors you should further examine:

- Valuation: What is GWPH worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether GWPH is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on GW Pharmaceuticals’s board and the CEO’s back ground.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.9% undervalued

64 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$487.1% overvalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

46 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$829.5% undervalued

25 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

BR

Bravosatya on Meta Platforms ·

Meta Platforms - Zuckerberg’s investment decisions are impulsive or Prudent?

Fair Value:US$730.0216.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JU

julio on FIGS ·

Figs valuation

Fair Value:US$14.3930.2% undervalued

21 followersusers have followed this narrative

6 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k45.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.3% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9634.1% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative