Advertisement

- United States

- /

- Consumer Services

- /

- NYSE:GHC

Graham Holdings Company (NYSE:GHC)'s Could Be A Buy For Its Upcoming Dividend

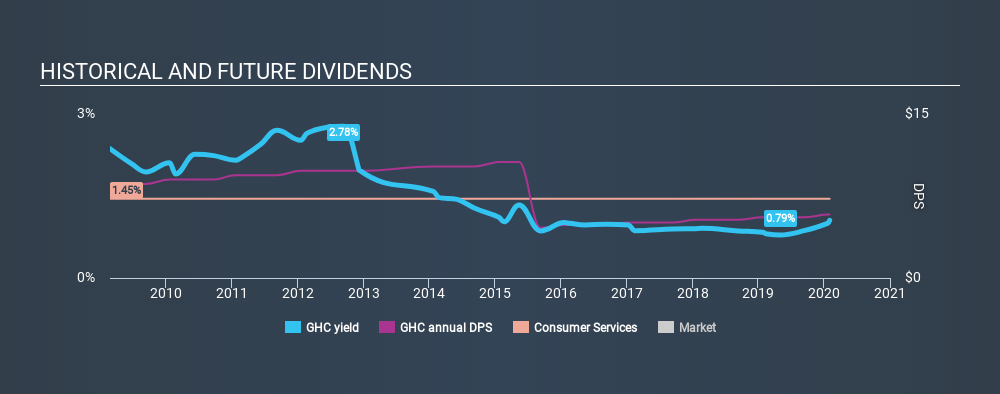

It looks like Graham Holdings Company (NYSE:GHC) is about to go ex-dividend in the next 3 days. If you purchase the stock on or after the 5th of February, you won't be eligible to receive this dividend, when it is paid on the 20th of February.

Graham Holdings's next dividend payment will be US$1.45 per share. Last year, in total, the company distributed US$5.56 to shareholders. Based on the last year's worth of payments, Graham Holdings stock has a trailing yield of around 1.1% on the current share price of $549.22. If you buy this business for its dividend, you should have an idea of whether Graham Holdings's dividend is reliable and sustainable. So we need to investigate whether Graham Holdings can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Graham Holdings

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Graham Holdings has a low and conservative payout ratio of just 12% of its income after tax. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Over the last year it paid out 56% of its free cash flow as dividends, within the usual range for most companies.

It's positive to see that Graham Holdings's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit Graham Holdings paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. It's encouraging to see Graham Holdings has grown its earnings rapidly, up 39% a year for the past five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Graham Holdings has seen its dividend decline 3.9% per annum on average over the past ten years, which is not great to see. Graham Holdings is a rare case where dividends have been decreasing at the same time as earnings per share have been improving. It's unusual to see, and could point to unstable conditions in the core business, or more rarely an intensified focus on reinvesting profits.

To Sum It Up

Should investors buy Graham Holdings for the upcoming dividend? From a dividend perspective, we're encouraged to see that earnings per share have been growing, the company is paying out less than half of its earnings, and a bit over half its free cash flow. Graham Holdings looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

Keen to explore more data on Graham Holdings's financial performance? Check out our visualisation of its historical revenue and earnings growth.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:GHC

Graham Holdings

Through its subsidiaries, operates as a diversified holding company in the United States and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor