- United States

- /

- Retail REITs

- /

- NYSE:GTY

Getty Realty Corp.'s (NYSE:GTY) Fundamentals Look Pretty Strong: Could The Market Be Wrong About The Stock?

With its stock down 39% over the past three months, it is easy to disregard Getty Realty (NYSE:GTY). However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. In this article, we decided to focus on Getty Realty's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Getty Realty

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Getty Realty is:

8.4% = US$50m ÷ US$589m (Based on the trailing twelve months to December 2019).

The 'return' is the amount earned after tax over the last twelve months. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.08.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

A Side By Side comparison of Getty Realty's Earnings Growth And 8.4% ROE

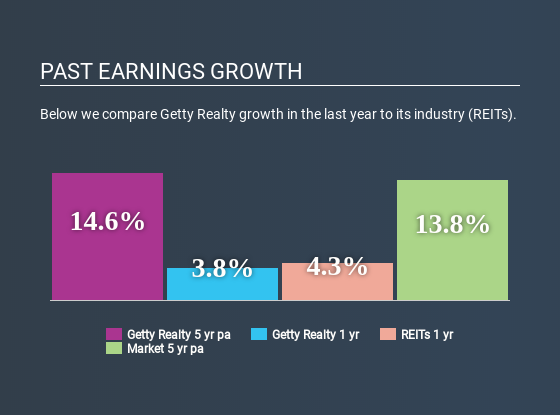

At first glance, Getty Realty's ROE doesn't look very promising. Although a closer study shows that the company's ROE is higher than the industry average of 5.8% which we definitely can't overlook. This certainly adds some context to Getty Realty's moderate 15% net income growth seen over the past five years. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. So there might well be other reasons for the earnings to grow. E.g the company has a low payout ratio or could belong to a high growth industry.

We then performed a comparison between Getty Realty's net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 15% in the same period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Getty Realty is trading on a high P/E or a low P/E, relative to its industry.

Is Getty Realty Making Efficient Use Of Its Profits?

Getty Realty seems to be paying out most of its income as dividends judging by its three-year median payout ratio of 54%, meaning the company retains only 46% of its income. However, this is typical for REITs as they are often required by law to distribute most of their earnings. Despite this, the company's earnings grew moderately as we saw above.

Moreover, Getty Realty is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 1.8% over the next three years. However, the company's ROE is not expected to change by much despite the lower expected payout ratio.

Conclusion

In total, it does look like Getty Realty has some positive aspects to its business. Specifically, its respectable ROE which likely led to the considerable growth in earnings. Yet, the company is retaining a small portion of its profits. Which means that the company has been able to grow its earnings in spite of it, so that's not too bad. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:GTY

Getty Realty

A publicly traded, net lease REIT specializing in the acquisition, financing and development of convenience, automotive and other single tenant retail real estate.

Undervalued established dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion