Advertisement

- United States

- /

- Chemicals

- /

- NYSEAM:FSI

Flexible Solutions International Inc. Beat Analyst Estimates: See What The Consensus Is Forecasting For This Year

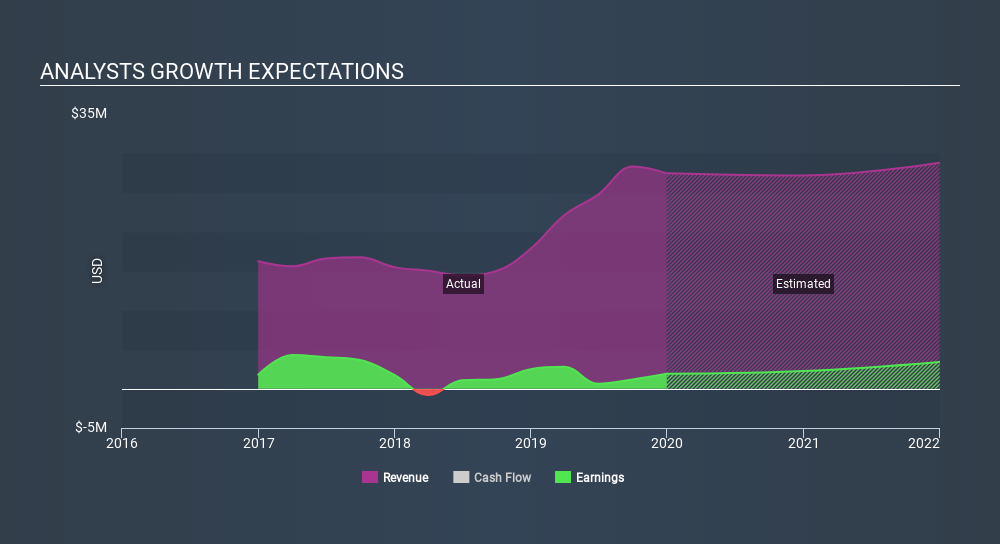

Flexible Solutions International Inc. (NYSEMKT:FSI) shareholders are probably feeling a little disappointed, since its shares fell 9.4% to US$1.15 in the week after its latest annual results. Revenues were US$27m, approximately in line with whatthe analyst expected, although statutory earnings per share (EPS) crushed expectations, coming in at US$0.16, an impressive 45% ahead of estimates. This is an important time for investors, as they can track a company's performance in its report, look at what expert is forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analyst is expecting for next year.

See our latest analysis for Flexible Solutions International

Following last week's earnings report, Flexible Solutions International's lone analyst are forecasting 2020 revenues to be US$27.2m, approximately in line with the last 12 months. Statutory earnings per share are predicted to swell 12% to US$0.18. In the lead-up to this report, the analyst had been modelling revenues of US$30.0m and earnings per share (EPS) of US$0.20 in 2020. The analyst seem less optimistic after the recent results, reducing their sales forecasts and making a substantial drop in earnings per share numbers.

The consensus price target fell 23% to US$2.50, with the weaker earnings outlook clearly leading valuation estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Flexible Solutions International's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast revenue decline of 1.0%, a significant reduction from annual growth of 9.3% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 3.1% next year. It's pretty clear that Flexible Solutions International's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analyst downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. The consensus price target fell measurably, with the analyst seemingly not reassured by the latest results, leading to a lower estimate of Flexible Solutions International's future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Flexible Solutions International going out as far as 2021, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 5 warning signs for Flexible Solutions International that you need to be mindful of.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSEAM:FSI

Flexible Solutions International

Develops, manufactures, and markets specialty chemicals that slow the evaporation of water in Canada, the United States, and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

IV

Ivoed on Intuit ·

he Market May Be Overpricing AI Risk And Underpricing Cash Flow Durability

Fair Value:US$39031.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on Adyen ·

Adyen’s next debate is not about payments growth, but whether its new layers actually become cash flow

Fair Value:€974.8110.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

ALL_in on Shenzhen Kaifa Technology ·

$深科技 / 000021.SZ — the chokepoint nobody is pricing in.

Fair Value:CN¥88.9547.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

60 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative