Advertisement

- Finland

- /

- Electrical

- /

- HLSE:KEMPOWR

European Value Stocks Trading At Estimated Discounts

Simply Wall St

Reviewed by Simply Wall St

Amid renewed uncertainty about U.S. trade policy and escalating geopolitical tensions in the Middle East, European markets have experienced a downturn, with major stock indexes like Germany’s DAX and Italy’s FTSE MIB seeing significant declines. In this environment of market volatility, identifying value stocks—those trading at prices lower than their intrinsic worth—can present opportunities for investors seeking potential discounts in the European market.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| VIGO Photonics (WSE:VGO) | PLN518.00 | PLN1019.78 | 49.2% |

| TTS (Transport Trade Services) (BVB:TTS) | RON4.31 | RON8.45 | 49% |

| Sparebank 68° Nord (OB:SB68) | NOK180.00 | NOK358.42 | 49.8% |

| Qt Group Oyj (HLSE:QTCOM) | €54.60 | €108.05 | 49.5% |

| Lectra (ENXTPA:LSS) | €23.90 | €46.66 | 48.8% |

| Koskisen Oyj (HLSE:KOSKI) | €8.80 | €17.34 | 49.2% |

| I.CO.P.. Società Benefit (BIT:ICOP) | €13.00 | €25.66 | 49.3% |

| doValue (BIT:DOV) | €2.22 | €4.43 | 49.9% |

| CTT Systems (OM:CTT) | SEK208.50 | SEK407.80 | 48.9% |

| Boreo Oyj (HLSE:BOREO) | €14.85 | €29.48 | 49.6% |

Let's dive into some prime choices out of the screener.

Lumibird (ENXTPA:LBIRD)

Overview: Lumibird SA designs, manufactures, and sells lasers for scientific, industrial, and medical applications internationally, with a market cap of €352.15 million.

Operations: The company's revenue is primarily derived from its Medical segment, contributing €107.75 million, and its Photonic segment, which adds €99.37 million.

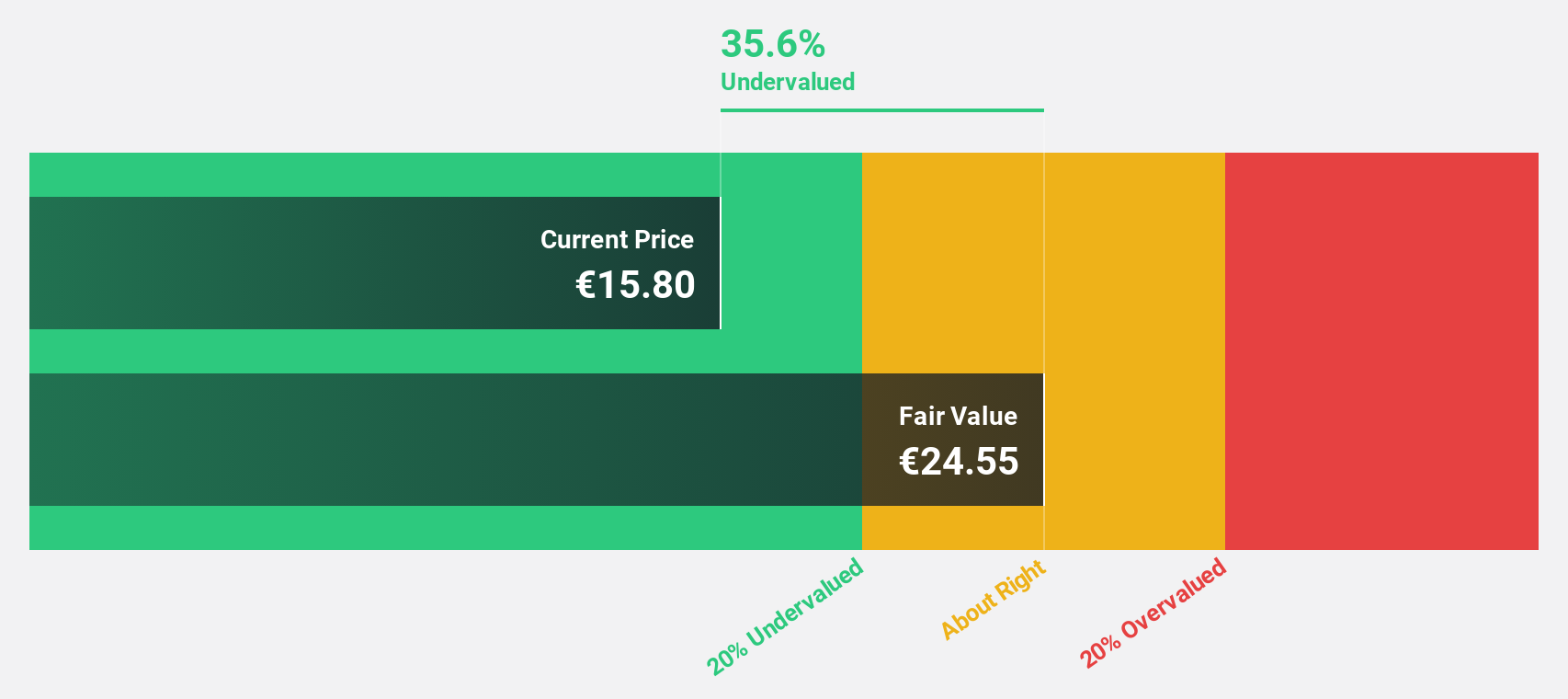

Estimated Discount To Fair Value: 35%

Lumibird is trading at €16, significantly below its estimated fair value of €24.62, presenting a compelling case for undervaluation based on discounted cash flow analysis. Despite high share price volatility and low forecasted return on equity of 8.7%, Lumibird's earnings are expected to grow significantly at 37.3% annually, outpacing the French market's average growth rate. Revenue growth is also projected to exceed the market average, enhancing its attractiveness despite recent large one-off items affecting results.

- The growth report we've compiled suggests that Lumibird's future prospects could be on the up.

- Click here to discover the nuances of Lumibird with our detailed financial health report.

Kempower Oyj (HLSE:KEMPOWR)

Overview: Kempower Oyj specializes in manufacturing and selling electric vehicle charging equipment and solutions for various modes of transportation across the Nordics, Europe, North America, and globally, with a market cap of €584.20 million.

Operations: The company's revenue is primarily derived from its electric equipment segment, which generated €224.60 million.

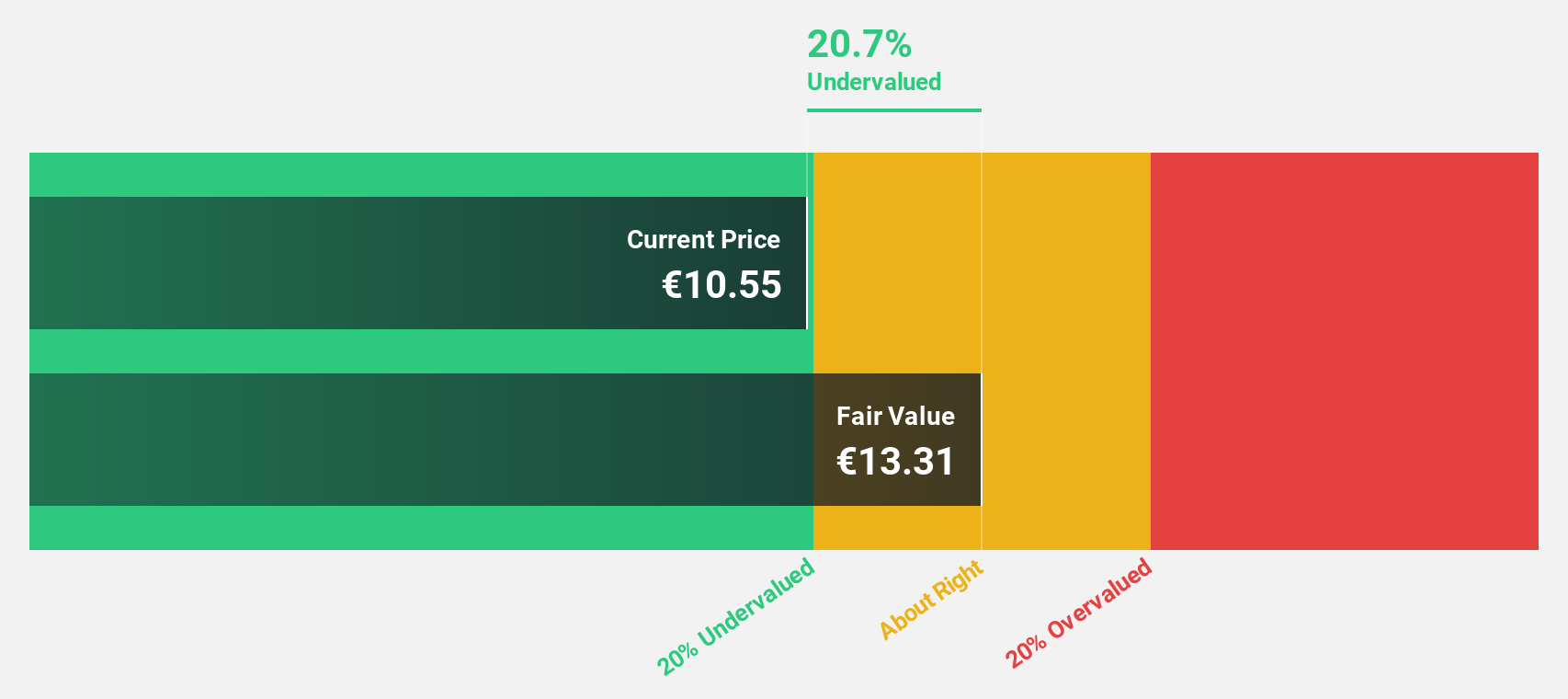

Estimated Discount To Fair Value: 20.6%

Kempower Oyj, trading at €10.55, is undervalued compared to its estimated fair value of €13.29, based on discounted cash flow analysis. While the company is not yet profitable, it is expected to achieve profitability within three years with earnings forecasted to grow significantly by 59.84% annually. Recent strategic moves include a four-year testing collaboration with Etteplan and securing a €40 million green revolving credit facility, reinforcing its growth potential despite current share price volatility.

- According our earnings growth report, there's an indication that Kempower Oyj might be ready to expand.

- Get an in-depth perspective on Kempower Oyj's balance sheet by reading our health report here.

Dätwyler Holding (SWX:DAE)

Overview: Dätwyler Holding AG produces and sells elastomer components for various industries including healthcare, mobility, connectors, general, and food and beverage across Europe, North America, South America, Australia, and Asia with a market cap of CHF2.04 billion.

Operations: The company's revenue is derived from two main segments: Healthcare Solutions, contributing CHF446 million, and Industrial Solutions, contributing CHF664.80 million.

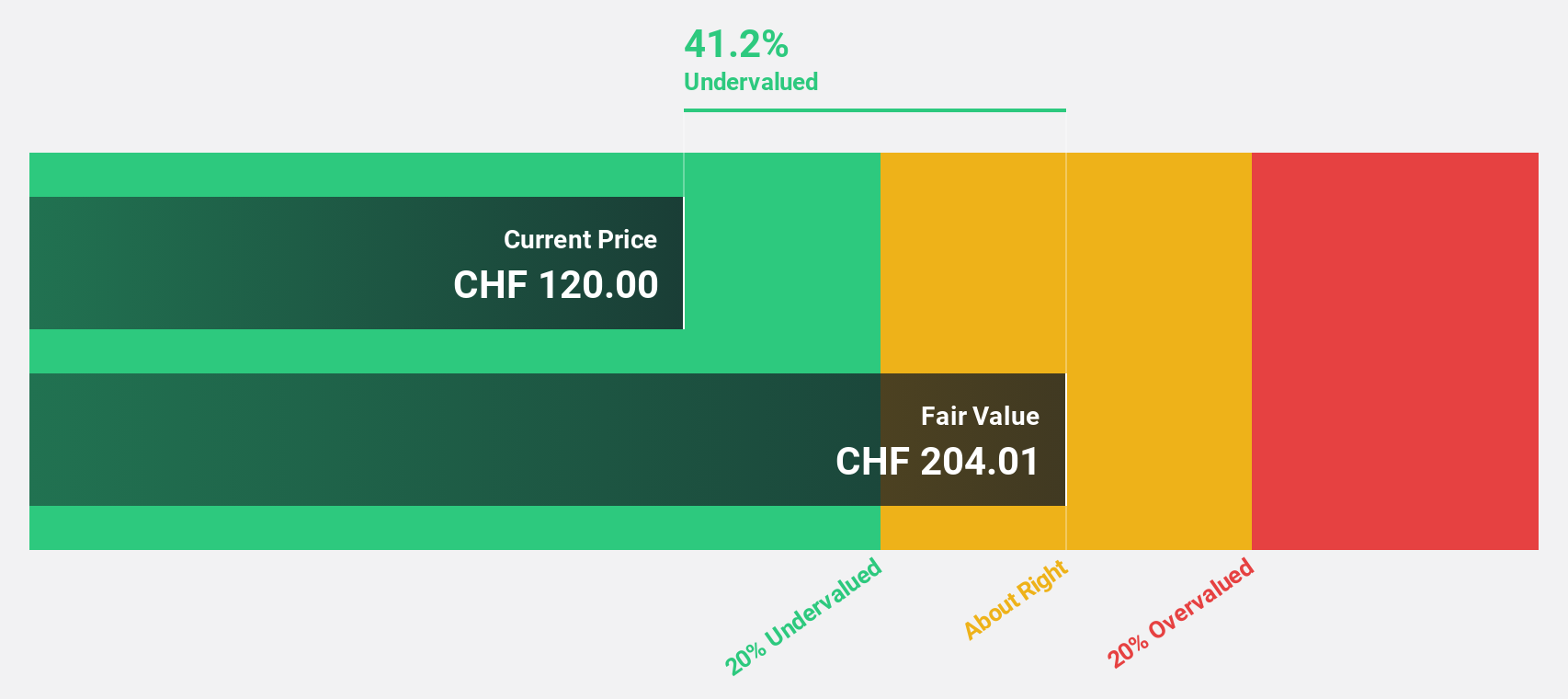

Estimated Discount To Fair Value: 41.2%

Dätwyler Holding, trading at CHF120, is significantly undervalued compared to its estimated fair value of CHF204.01 based on discounted cash flow analysis. Although profit margins have decreased from last year and the dividend yield of 2.67% is not well-covered by earnings, the company's earnings are forecasted to grow substantially at 33.6% annually over the next three years, surpassing Swiss market growth expectations and indicating strong future profitability potential despite current financial challenges.

- The analysis detailed in our Dätwyler Holding growth report hints at robust future financial performance.

- Dive into the specifics of Dätwyler Holding here with our thorough financial health report.

Where To Now?

- Reveal the 179 hidden gems among our Undervalued European Stocks Based On Cash Flows screener with a single click here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kempower Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About HLSE:KEMPOWR

Kempower Oyj

Manufactures and sells electric vehicle (EV) charging equipment and solutions for cars, buses, trucks, boats, aviation, and machinery in Nordics, rest of Europe, North America, and internationally.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor