Advertisement

European Stocks That May Be Trading Below Estimated Value In June 2025

Simply Wall St

Reviewed by Simply Wall St

As European markets navigate the complexities of geopolitical tensions and economic shifts, indices such as the STOXX Europe 600 have experienced declines, reflecting broader concerns. In this environment, identifying stocks that may be trading below their estimated value can provide investors with opportunities to potentially benefit from market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| TTS (Transport Trade Services) (BVB:TTS) | RON4.29 | RON8.47 | 49.4% |

| Sparebank 68° Nord (OB:SB68) | NOK182.98 | NOK357.54 | 48.8% |

| Selvita (WSE:SLV) | PLN28.70 | PLN56.89 | 49.6% |

| Lingotes Especiales (BME:LGT) | €6.00 | €11.87 | 49.4% |

| Laboratorios Farmaceuticos Rovi (BME:ROVI) | €54.00 | €104.47 | 48.3% |

| Koskisen Oyj (HLSE:KOSKI) | €8.84 | €17.31 | 48.9% |

| Galderma Group (SWX:GALD) | CHF111.30 | CHF221.71 | 49.8% |

| dormakaba Holding (SWX:DOKA) | CHF723.00 | CHF1400.15 | 48.4% |

| Absolent Air Care Group (OM:ABSO) | SEK209.00 | SEK415.74 | 49.7% |

| ABO Energy GmbH KGaA (XTRA:AB9) | €36.50 | €70.64 | 48.3% |

Here we highlight a subset of our preferred stocks from the screener.

Recordati Industria Chimica e Farmaceutica (BIT:REC)

Overview: Recordati Industria Chimica e Farmaceutica S.p.A. is a pharmaceutical company that researches, develops, produces, and sells its products across various international markets including Italy, the United States, and several European countries, with a market cap of approximately €11.20 billion.

Operations: Recordati generates revenue through its Rare Diseases segment, which contributes €891.12 million, and its Specialty & Primary Care segment, which accounts for €1.52 billion.

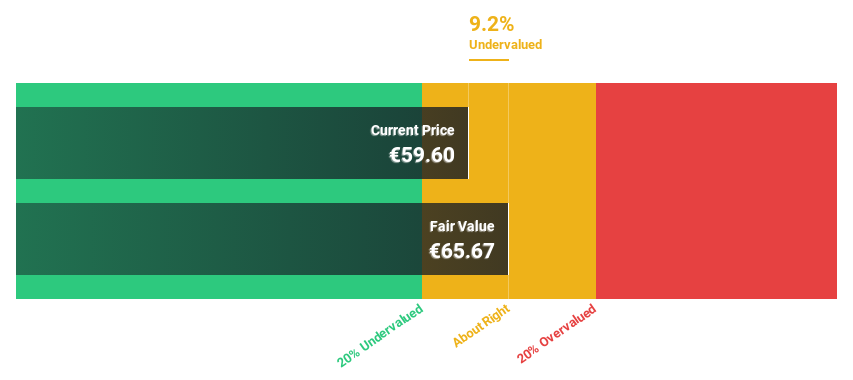

Estimated Discount To Fair Value: 11.3%

Recordati Industria Chimica e Farmaceutica is trading at €54.3, below its estimated fair value of €61.23, suggesting it may be undervalued based on discounted cash flows. Despite a high level of debt, the company forecasts earnings growth of 12.33% annually, outpacing the Italian market's 6.4%. Recent FDA approval for ISTURISA® expands its market potential, while Q1 2025 results showed sales growth to €679.96 million from €607.82 million year-over-year.

- Our comprehensive growth report raises the possibility that Recordati Industria Chimica e Farmaceutica is poised for substantial financial growth.

- Click here to discover the nuances of Recordati Industria Chimica e Farmaceutica with our detailed financial health report.

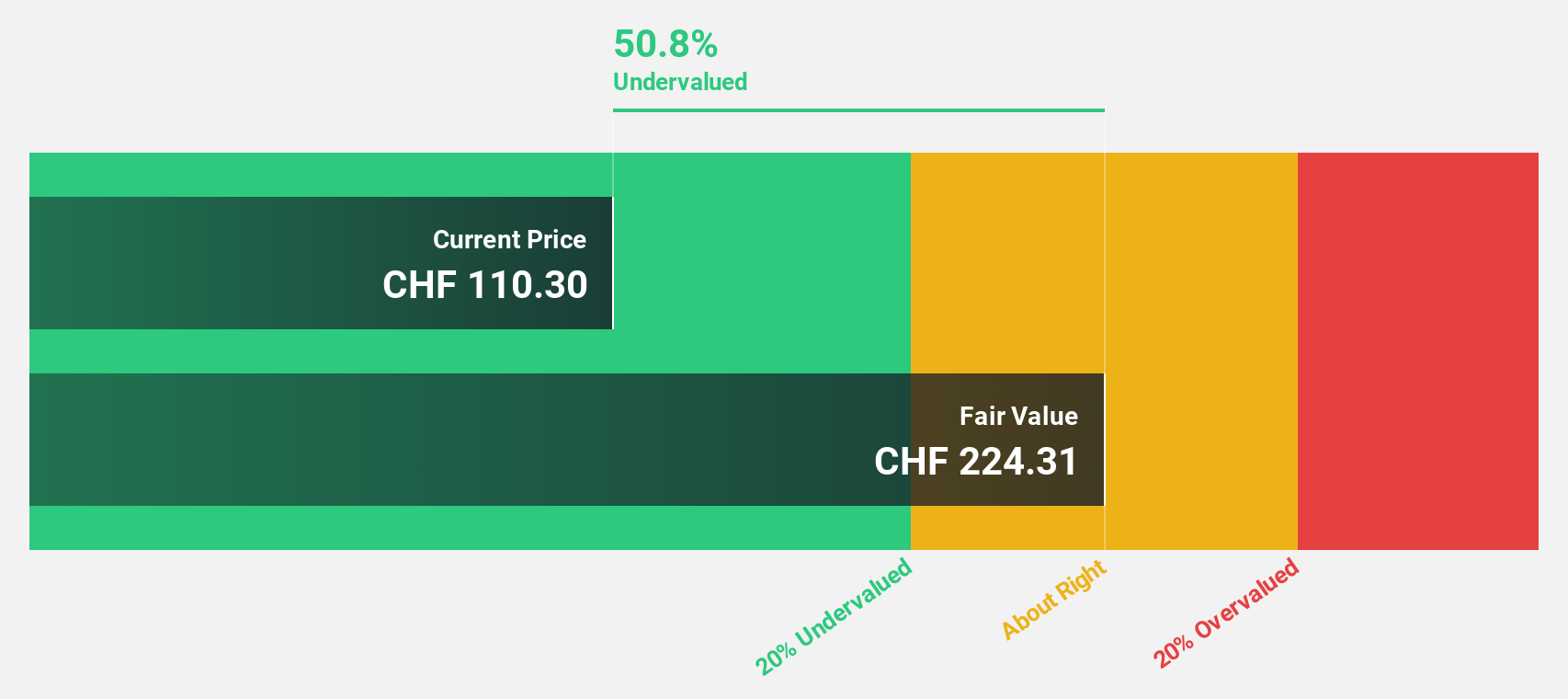

Galderma Group (SWX:GALD)

Overview: Galderma Group AG is a global dermatology company with a market cap of CHF26.42 billion.

Operations: The company's revenue segment is focused on dermatology, generating $4.44 billion.

Estimated Discount To Fair Value: 49.8%

Galderma Group, trading at CHF111.3, is significantly undervalued with a fair value estimate of CHF221.71. Its earnings are projected to grow 32% annually, surpassing the Swiss market's average growth rate of 10.4%. The company recently expanded its U.S. operations and introduced innovative products like Nemluvio for skin diseases, enhancing its growth prospects despite recent share price volatility and a forecasted low return on equity in three years (12%).

- The growth report we've compiled suggests that Galderma Group's future prospects could be on the up.

- Dive into the specifics of Galderma Group here with our thorough financial health report.

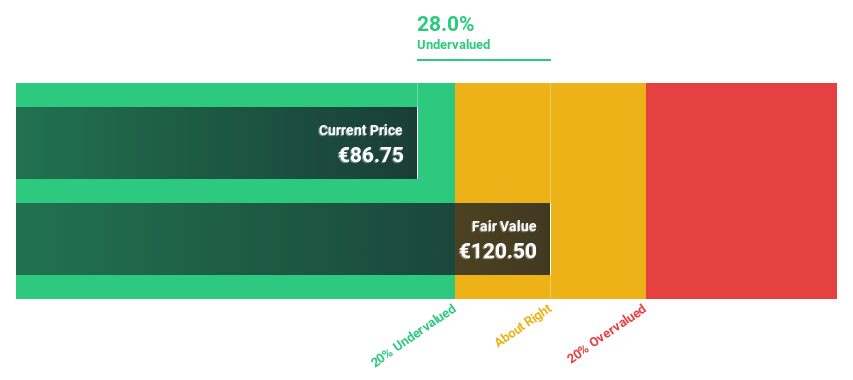

Knorr-Bremse (XTRA:KBX)

Overview: Knorr-Bremse AG, along with its subsidiaries, specializes in developing, producing, and marketing brake systems for rail and commercial vehicles as well as other safety-critical systems globally, with a market cap of approximately €13.67 billion.

Operations: The company's revenue is primarily derived from Rail Vehicle Systems, contributing €4.23 billion, and Commercial Vehicle Systems, which accounts for €3.79 billion.

Estimated Discount To Fair Value: 21.5%

Knorr-Bremse, trading at €84.8, is undervalued relative to its fair value estimate of €108. Its earnings are forecasted to grow significantly at 23.2% annually, outpacing the German market's growth rate of 16.4%. Despite a recent decline in quarterly revenue and net income compared to last year, the company maintains strong future prospects with confirmed guidance for revenues between €8.1 billion and €8.4 billion for fiscal year 2025.

- Upon reviewing our latest growth report, Knorr-Bremse's projected financial performance appears quite optimistic.

- Get an in-depth perspective on Knorr-Bremse's balance sheet by reading our health report here.

Seize The Opportunity

- Investigate our full lineup of 168 Undervalued European Stocks Based On Cash Flows right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Knorr-Bremse might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:KBX

Knorr-Bremse

Develops, produces, and markets brake systems for rail and commercial vehicles and other safety-critical systems worldwide.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|40.5% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|91.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|16.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.5% undervalued

AG

Community Contributor