Advertisement

- United States

- /

- Media

- /

- OTCPK:AUDA.Q

Entercom Communications Corp. (NYSE:ETM) Analysts Are Pretty Bullish On The Stock After Recent Results

Entercom Communications Corp. (NYSE:ETM) missed earnings with its latest first-quarter results, disappointing overly-optimistic forecasters. It was a pretty negative result overall, with revenues of US$297m missing analyst predictions by 2.6%. Worse, the business reported a statutory loss of US$0.07 per share, much larger than the analysts had forecast prior to the result. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Entercom Communications

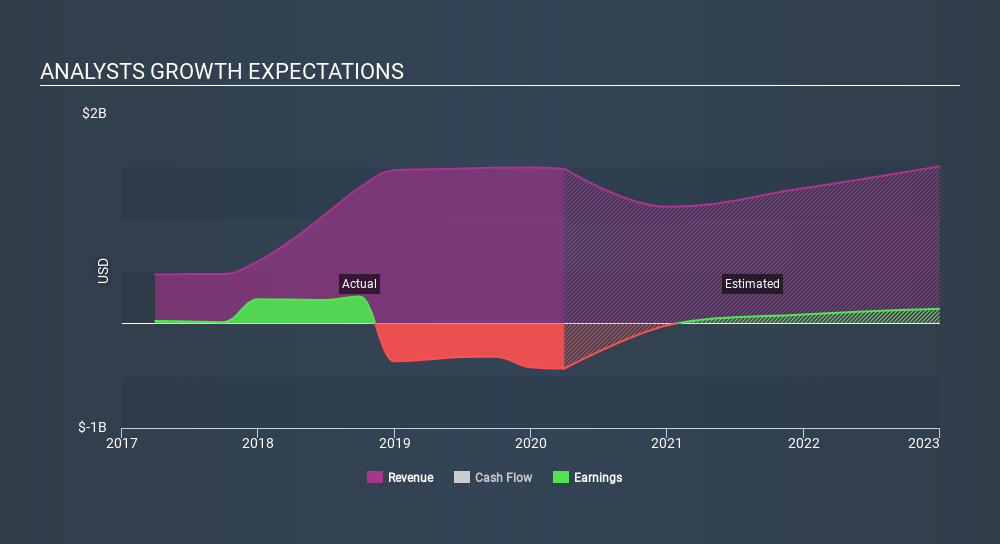

Following the recent earnings report, the consensus from four analysts covering Entercom Communications is for revenues of US$1.11b in 2020, implying a concerning 25% decline in sales compared to the last 12 months. Entercom Communications is also expected to turn profitable, with statutory earnings of US$0.27 per share. In the lead-up to this report, the analysts had been modelling revenues of US$1.18b and earnings per share (EPS) of US$0.24 in 2020. While revenue forecasts have been revised downwards, the analysts look to have become more optimistic on the company's cost base, given the solid gain to to the earnings per share numbers.

The average price target increased 6.7% to US$2.00, with the analysts signalling that the improved earnings outlook is more important to the company's valuation than its revenue. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Entercom Communications at US$3.50 per share, while the most bearish prices it at US$1.00. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how analysts think this business will perform. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with the forecast 25% revenue decline a notable change from historical growth of 34% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.1% annually for the foreseeable future. It's pretty clear that Entercom Communications' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Entercom Communications following these results. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. With that said, earnings are more important to the long-term value of the business. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Entercom Communications going out to 2022, and you can see them free on our platform here.

Even so, be aware that Entercom Communications is showing 2 warning signs in our investment analysis , you should know about...

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OTCPK:AUDA.Q

Audacy

A multi-platform audio content and entertainment company, engages in the radio broadcasting business in the United States.

Moderate and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor