Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:ENB

Enbridge Inc. Earnings Missed Analyst Estimates: Here's What Analysts Are Forecasting Now

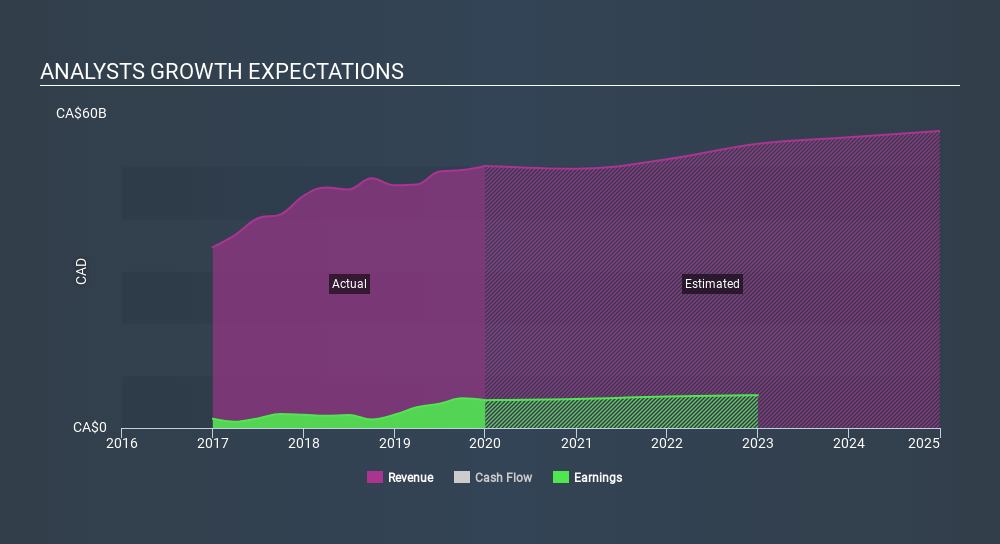

Last week saw the newest yearly earnings release from Enbridge Inc. (TSE:ENB), an important milestone in the company's journey to build a stronger business. Revenues of CA$50b were in line with forecasts, although statutory earnings per share (EPS) came in below expectations at CA$2.64, missing estimates by 8.6%. Earnings are an important time for investors, as they can track a company's performance, look at what top analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what analysts are expecting for next year.

Check out our latest analysis for Enbridge

Following last week's earnings report, Enbridge's 14 analysts are forecasting 2020 revenues to be CA$49.5b, approximately in line with the last 12 months. Statutory per share are forecast to be CA$2.65, approximately in line with the last 12 months. In the lead-up to this report, analysts had been modelling revenues of CA$50.8b and earnings per share (EPS) of CA$2.69 in 2020. So it looks like analysts have become a bit less optimistic after the latest results announcement, with revenues expected to fall even as the company is expected to maintain EPS.

The average price target was steady at CA$57.14 even though revenue estimates declined; likely suggesting analysts place a higher value on earnings. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Enbridge analyst has a price target of CA$65.00 per share, while the most pessimistic values it at CA$38.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Enbridge shareholders.

Further, we can compare these estimates to past performance, and see how Enbridge forecasts compare to the wider market's forecast performance. We would highlight that sales are expected to reverse, with the forecast 1.1% revenue decline a notable change from historical growth of 9.1% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same market are forecast to see their revenue grow 3.3% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - analysts also expect Enbridge to grow slower than the wider market.

The Bottom Line

The most obvious conclusion from these results is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. Unfortunately, analysts also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider market. Even so, earnings per share are more important to the intrinsic value of the business. Still, earnings are more important to the long-term value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have forecasts for Enbridge going out to 2024, and you can see them free on our platform here.

You can also see whether Enbridge is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:ENB

Enbridge

Operates as an energy infrastructure company.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1156.8% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7720.5% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1909.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

FU

FundamentalFlow on Samsung Electronics ·

Samsung electronics, the DRAM bottleneck, leading the memory shortage wave?

Fair Value:₩500k47.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DI

divine_4y1uv on PRG Holdings Berhad ·

Dato’ Ng Yan Cheng Perjelaskan Pendahuluan RM89.55 Juta Bagi Menyokong Kewangan Syarikat

Fair Value:RM 0.361.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on PRG Holdings Berhad ·

Dato' Ng Yan Cheng Clarifies RM89.55 Million in Financial Support To PRG

Fair Value:RM 0.361.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.2% undervalued

99 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.1% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.8% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0