Advertisement

Despite Its High P/E Ratio, Is Dassault Systèmes SE (EPA:DSY) Still Undervalued?

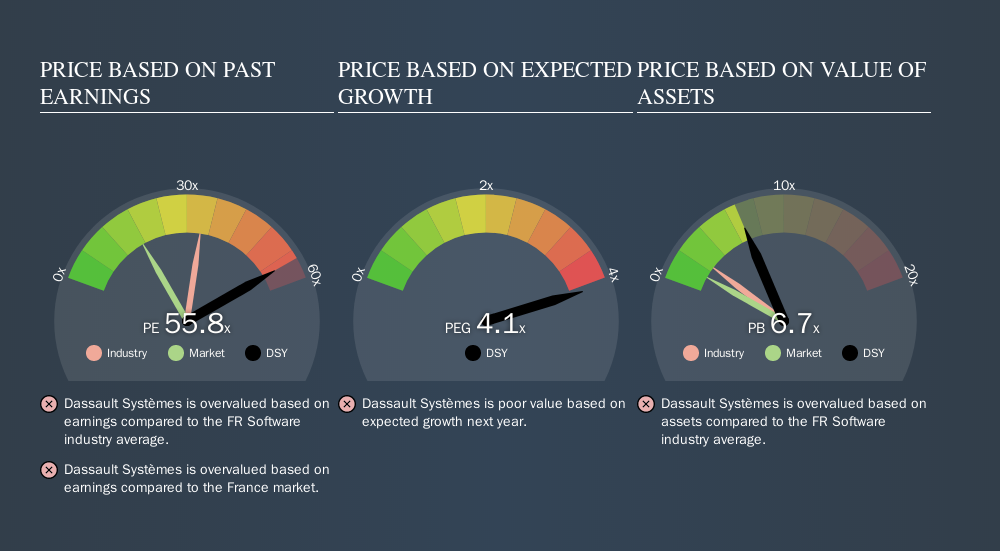

This article is written for those who want to get better at using price to earnings ratios (P/E ratios). We'll show how you can use Dassault Systèmes SE's (EPA:DSY) P/E ratio to inform your assessment of the investment opportunity. What is Dassault Systèmes's P/E ratio? Well, based on the last twelve months it is 55.78. In other words, at today's prices, investors are paying €55.78 for every €1 in prior year profit.

See our latest analysis for Dassault Systèmes

How Do You Calculate Dassault Systèmes's P/E Ratio?

The formula for P/E is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Dassault Systèmes:

P/E of 55.78 = €134.15 ÷ €2.40 (Based on the year to September 2019.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each €1 of company earnings. All else being equal, it's better to pay a low price -- but as Warren Buffett said, 'It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

How Does Dassault Systèmes's P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. As you can see below, Dassault Systèmes has a higher P/E than the average company (33.6) in the software industry.

That means that the market expects Dassault Systèmes will outperform other companies in its industry.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. That's because companies that grow earnings per share quickly will rapidly increase the 'E' in the equation. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

Dassault Systèmes saw earnings per share improve by -8.5% last year. And earnings per share have improved by 15% annually, over the last five years. Shareholders have some reason to be optimistic, but the future is always uncertain. So further research is always essential. I often monitor director buying and selling.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. That means it doesn't take debt or cash into account. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

Is Debt Impacting Dassault Systèmes's P/E?

Dassault Systèmes has net cash of €2.2b. That should lead to a higher P/E than if it did have debt, because its strong balance sheets gives it more options.

The Verdict On Dassault Systèmes's P/E Ratio

With a P/E ratio of 55.8, Dassault Systèmes is expected to grow earnings very strongly in the years to come. EPS was up modestly better over the last twelve months. And the healthy balance sheet means the company can sustain growth while the P/E suggests shareholders think it will.

Investors should be looking to buy stocks that the market is wrong about. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:DSY

Dassault Systèmes

Provides software solutions and services worldwide.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

164 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.0% overvalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9412.5% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87179.9% overvalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Korea Electric Power ·

Korea Electric Power Corp (KEP): The Grid’s Tug-of-War – AI Demand vs. The Strait of Hormuz

Fair Value:US$32.5150.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Coherent ·

Coherent Corp. (COHR): The Optical AI Engine – Scaling the Photon-Silicon Frontier

Fair Value:US$2501.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GL

GlennUrban on High Tide ·

High Tide's Future Potential Will Surge with 15% Revenue Growth

Fair Value:US$1281.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9826.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

35 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0