Advertisement

Companies Like 8common (ASX:8CO) Can Afford To Invest In Growth

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. Indeed, 8common (ASX:8CO) stock is up 183% in the last year, providing strong gains for shareholders. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given its strong share price performance, we think it's worthwhile for 8common shareholders to consider whether its cash burn is concerning. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for 8common

When Might 8common Run Out Of Money?

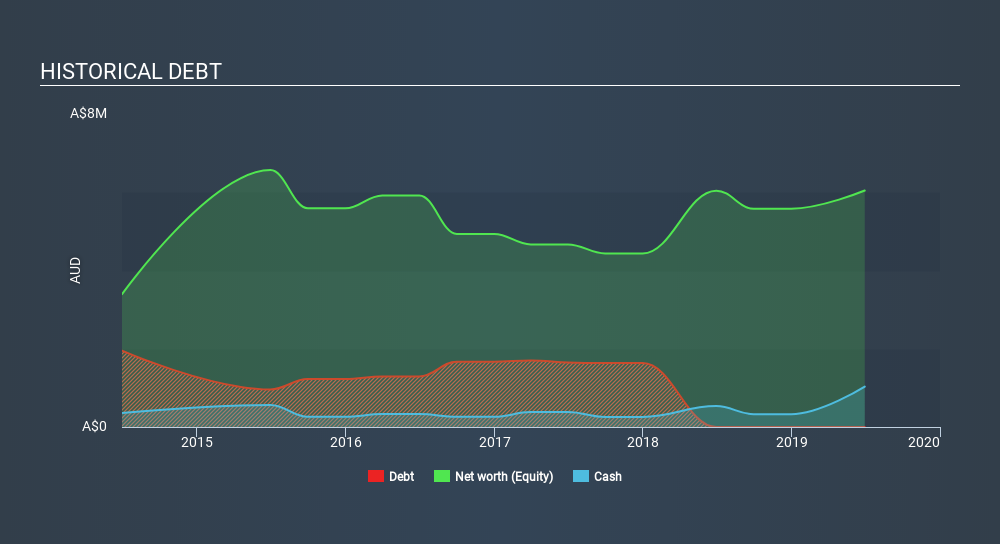

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In June 2019, 8common had AU$1.0m in cash, and was debt-free. Importantly, its cash burn was AU$130k over the trailing twelve months. That means it had a cash runway of about 7.9 years as of June 2019. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. You can see how its cash balance has changed over time in the image below.

How Well Is 8common Growing?

8common managed to reduce its cash burn by 75% over the last twelve months, which suggests it's on the right flight path. Pleasingly, this was achieved with the help of a 32% boost to revenue. We think it is growing rather well, upon reflection. Of course, we've only taken a quick look at the stock's growth metrics, here. You can take a look at how 8common is growing revenue over time by checking this visualization of past revenue growth.

How Hard Would It Be For 8common To Raise More Cash For Growth?

There's no doubt 8common seems to be in a fairly good position, when it comes to managing its cash burn, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash to drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

8common's cash burn of AU$130k is about 0.8% of its AU$15m market capitalisation. So it could almost certainly just borrow a little to fund another year's growth, or else easily raise the cash by issuing a few shares.

How Risky Is 8common's Cash Burn Situation?

It may already be apparent to you that we're relatively comfortable with the way 8common is burning through its cash. In particular, we think its cash runway stands out as evidence that the company is well on top of its spending. And even its revenue growth was very encouraging. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash. When you don't have traditional metrics like earnings per share and free cash flow to value a company, many are extra motivated to consider qualitative factors such as whether insiders are buying or selling shares. Please Note: 8common insiders have been trading shares, according to our data. Click here to check whether insiders have been buying or selling.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ASX:8CO

8common

Engages in the expense management software business in Australia, Asia, North America, and internationally.

Medium-low and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor