Advertisement

- India

- /

- Life Sciences

- /

- NSEI:BROOKS

Brooks Laboratories (NSE:BROOKS) Is Making Moderate Use Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Brooks Laboratories Limited (NSE:BROOKS) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Brooks Laboratories

What Is Brooks Laboratories's Net Debt?

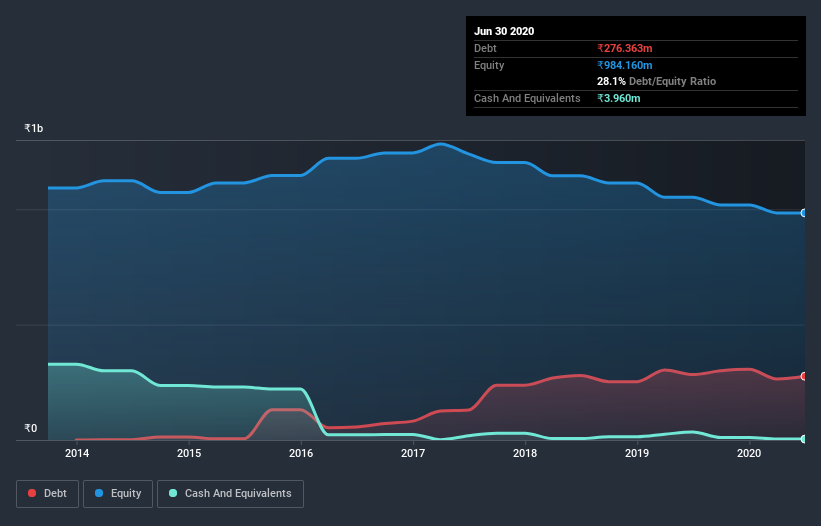

You can click the graphic below for the historical numbers, but it shows that Brooks Laboratories had ₹264.2m of debt in March 2020, down from ₹283.3m, one year before. Net debt is about the same, since the it doesn't have much cash.

How Strong Is Brooks Laboratories's Balance Sheet?

According to the last reported balance sheet, Brooks Laboratories had liabilities of ₹458.0m due within 12 months, and liabilities of ₹136.5m due beyond 12 months. Offsetting this, it had ₹3.96m in cash and ₹218.7m in receivables that were due within 12 months. So it has liabilities totalling ₹371.8m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Brooks Laboratories is worth ₹1.34b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Brooks Laboratories's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Brooks Laboratories wasn't profitable at an EBIT level, but managed to grow its revenue by 6.8%, to ₹653m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Brooks Laboratories had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at ₹94m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled ₹120m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Consider for instance, the ever-present spectre of investment risk. We've identified 5 warning signs with Brooks Laboratories (at least 2 which are significant) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Brooks Laboratories, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Brooks Laboratories might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:BROOKS

Brooks Laboratories

Provides contract development and manufacturing services for pharmaceutical companies in India and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1941.1% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

50 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.5% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.5% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

AG

Agricola on Silver Storm Mining ·

A case for USD $26.00 (CAD 36.00) by 2030 with a MKT CAP of CAD$8.40 billion (USD$6.10) (10 bagger by Dec 2027)

Fair Value:CA$3698.8% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on First Mining Gold ·

First Mining Gold's competitive advantages in the mining sector.

Fair Value:CA$587.4% undervalued

23 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Central Asia Metals ·

A Case for Central Asia Metals to reach £8-12 by 2031 in a commodities bull market.

Fair Value:UK£1288.6% undervalued

2 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.6% undervalued

92 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5455.7% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3455.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0