Advertisement

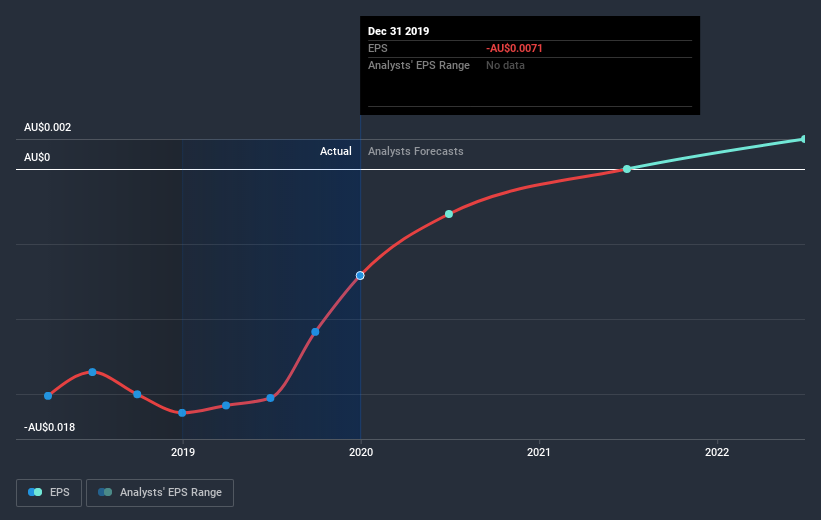

SECOS Group Limited's (ASX:SES): SECOS Group Limited manufactures and distributes sustainable packaging materials worldwide. The AU$56m market-cap company’s loss lessens since it announced a AU$4.2m loss in the full financial year, compared to the latest trailing-twelve-month loss of AU$2.3m, as it approaches breakeven. Many investors are wondering the rate at which SES will turn a profit, with the big question being “when will the company breakeven?” In this article, I will touch on the expectations for SES’s growth and when analysts expect the company to become profitable.

Check out our latest analysis for SECOS Group

According to the industry analysts covering SES, breakeven is near. They anticipate the company to incur a final loss in 2020, before generating positive profits of AU$200k in 2021. So, SES is predicted to breakeven approximately a couple of months from now! How fast will SES have to grow each year in order to reach the breakeven point by 2021? Working backwards from analyst estimates, it turns out that they expect the company to grow 111% year-on-year, on average, which is extremely buoyant. Should the business grow at a slower rate, it will become profitable at a later date than expected.

Given this is a high-level overview, I won’t go into details of SES’s upcoming projects, but, keep in mind that typically a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before I wrap up, there’s one aspect worth mentioning. SES has managed its capital prudently, with debt making up 8.6% of equity. This means that SES has predominantly funded its operations from equity capital,and its low debt obligation reduces the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on SES, so if you are interested in understanding the company at a deeper level, take a look at SES’s company page on Simply Wall St. I’ve also compiled a list of relevant factors you should look at:

- Valuation: What is SES worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether SES is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on SECOS Group’s board and the CEO’s back ground.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

When trading SECOS Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:MCO

Myeco Group

Develops, manufactures, and sells sustainable packaging and materials in Oceanic, Asia, the United States, Europe, and Africa.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1257.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.720.8% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

JR

JRY on Bloom Energy ·

The Bloom Story is early days

Fair Value:US$386.143.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CH

ChuckN on NextEra Energy ·

Investor Thesis: Why the NextEra Energy / Dominion Energy Merger Could Be a Major AI Power Infrastructure Event

Fair Value:US$93.719.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.1% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

284 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

145 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

169 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0