Stock Analysis

- United States

- /

- Packaging

- /

- NYSE:GPK

It's A Story Of Risk Vs Reward With Graphic Packaging Holding Company (NYSE:GPK)

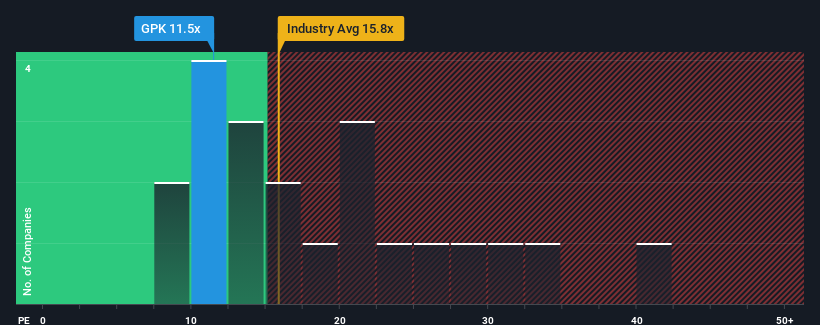

With a price-to-earnings (or "P/E") ratio of 11.5x Graphic Packaging Holding Company (NYSE:GPK) may be sending bullish signals at the moment, given that almost half of all companies in the United States have P/E ratios greater than 17x and even P/E's higher than 32x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Graphic Packaging Holding certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Graphic Packaging Holding

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Graphic Packaging Holding's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 39%. Pleasingly, EPS has also lifted 294% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 9.2% per annum during the coming three years according to the twelve analysts following the company. That's shaping up to be similar to the 10% per annum growth forecast for the broader market.

In light of this, it's peculiar that Graphic Packaging Holding's P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Final Word

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Graphic Packaging Holding's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

There are also other vital risk factors to consider before investing and we've discovered 2 warning signs for Graphic Packaging Holding that you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're helping make it simple.

Find out whether Graphic Packaging Holding is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:GPK

Graphic Packaging Holding

Graphic Packaging Holding Company, together with its subsidiaries, designs, produces, and sells consumer packaging products to brands in food, beverage, foodservice, household, and other consumer products.

Undervalued with solid track record.