Stock Analysis

- United States

- /

- Software

- /

- NYSE:PD

PagerDuty (NYSE:PD shareholders incur further losses as stock declines 5.2% this week, taking five-year losses to 59%

Statistically speaking, long term investing is a profitable endeavour. But along the way some stocks are going to perform badly. Zooming in on an example, the PagerDuty, Inc. (NYSE:PD) share price dropped 59% in the last half decade. We certainly feel for shareholders who bought near the top. And we doubt long term believers are the only worried holders, since the stock price has declined 32% over the last twelve months. Shareholders have had an even rougher run lately, with the share price down 16% in the last 90 days.

Since PagerDuty has shed US$101m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

Check out our latest analysis for PagerDuty

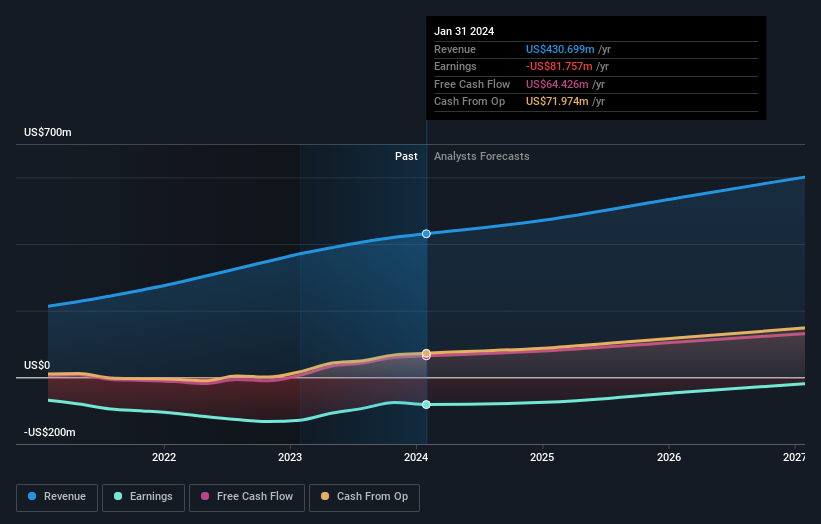

PagerDuty isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally hope to see good revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

Over five years, PagerDuty grew its revenue at 25% per year. That's well above most other pre-profit companies. In contrast, the share price is has averaged a loss of 10% per year - that's quite disappointing. This could mean high expectations have been tempered, potentially because investors are looking to the bottom line. If you think the company can keep up its revenue growth, you'd have to consider the possibility that there's an opportunity here.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

PagerDuty is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. You can see what analysts are predicting for PagerDuty in this interactive graph of future profit estimates.

A Different Perspective

While the broader market gained around 24% in the last year, PagerDuty shareholders lost 32%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 10% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand PagerDuty better, we need to consider many other factors. To that end, you should be aware of the 1 warning sign we've spotted with PagerDuty .

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether PagerDuty is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:PD

PagerDuty

PagerDuty, Inc. engages in the operation of a digital operations management platform in the United States and internationally.

Excellent balance sheet and good value.