Advertisement

Today we'll evaluate Enghouse Systems Limited (TSE:ENGH) to determine whether it could have potential as an investment idea. In particular, we'll consider its Return On Capital Employed (ROCE), as that can give us insight into how profitably the company is able to employ capital in its business.

Firstly, we'll go over how we calculate ROCE. Then we'll compare its ROCE to similar companies. Last but not least, we'll look at what impact its current liabilities have on its ROCE.

Understanding Return On Capital Employed (ROCE)

ROCE measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Generally speaking a higher ROCE is better. Overall, it is a valuable metric that has its flaws. Renowned investment researcher Michael Mauboussin has suggested that a high ROCE can indicate that 'one dollar invested in the company generates value of more than one dollar'.

How Do You Calculate Return On Capital Employed?

The formula for calculating the return on capital employed is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for Enghouse Systems:

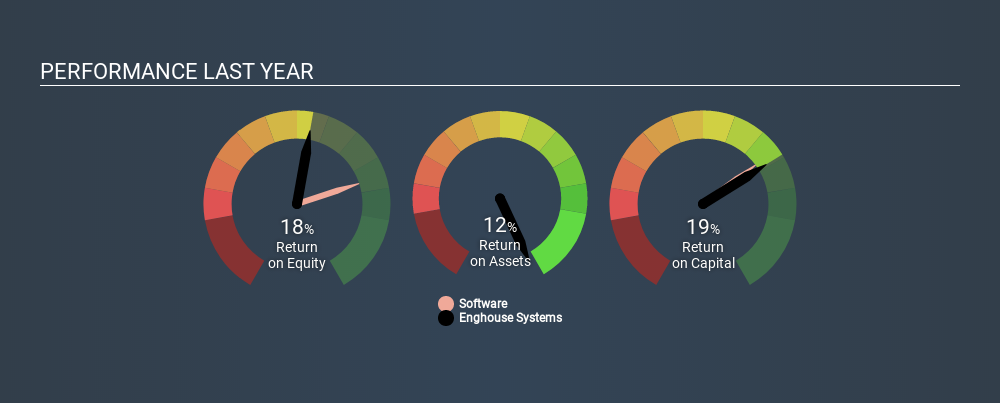

0.19 = CA$81m ÷ (CA$591m - CA$161m) (Based on the trailing twelve months to October 2019.)

So, Enghouse Systems has an ROCE of 19%.

See our latest analysis for Enghouse Systems

Is Enghouse Systems's ROCE Good?

ROCE can be useful when making comparisons, such as between similar companies. Using our data, we find that Enghouse Systems's ROCE is meaningfully better than the 11% average in the Software industry. I think that's good to see, since it implies the company is better than other companies at making the most of its capital. Separate from Enghouse Systems's performance relative to its industry, its ROCE in absolute terms looks satisfactory, and it may be worth researching in more depth.

You can see in the image below how Enghouse Systems's ROCE compares to its industry. Click to see more on past growth.

When considering this metric, keep in mind that it is backwards looking, and not necessarily predictive. ROCE can be misleading for companies in cyclical industries, with returns looking impressive during the boom times, but very weak during the busts. This is because ROCE only looks at one year, instead of considering returns across a whole cycle. Since the future is so important for investors, you should check out our free report on analyst forecasts for Enghouse Systems.

Do Enghouse Systems's Current Liabilities Skew Its ROCE?

Liabilities, such as supplier bills and bank overdrafts, are referred to as current liabilities if they need to be paid within 12 months. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To check the impact of this, we calculate if a company has high current liabilities relative to its total assets.

Enghouse Systems has total assets of CA$591m and current liabilities of CA$161m. Therefore its current liabilities are equivalent to approximately 27% of its total assets. Current liabilities are minimal, limiting the impact on ROCE.

The Bottom Line On Enghouse Systems's ROCE

With that in mind, Enghouse Systems's ROCE appears pretty good. There might be better investments than Enghouse Systems out there, but you will have to work hard to find them . These promising businesses with rapidly growing earnings might be right up your alley.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:ENGH

Enghouse Systems

Develops enterprise software solutions worldwide.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

177 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k9.6% overvalued

24 followersusers have followed this narrative

1 commentusers have commented on this narrative

25 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$50013.5% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8563.4% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

SO

Souza123 on Inter & Co ·

Inter&Co - 60/30/30 Plan

Fair Value:US$33.374.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.6% undervalued

70 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Janpeo on Solaria Energía y Medio Ambiente ·

Solaria – Intrinsic Value Update (March 2026)

Fair Value:€1918.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9827.3% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.9% undervalued

56 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6433.7% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0