Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:AMAT

Applied Materials, Inc. Just Reported First-Quarter Earnings And Analysts Are Lifting Their Estimates

It's been a good week for Applied Materials, Inc. (NASDAQ:AMAT) shareholders, because the company has just released its latest first-quarter results, and the shares gained 8.3% to US$66.85. The result was positive overall - although revenues of US$4.2b were in line with what analysts predicted, Applied Materials surprised by delivering a statutory profit of US$0.96 per share, modestly greater than expected. Following the result, analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether analysts have changed their mind on Applied Materials after the latest results.

Check out our latest analysis for Applied Materials

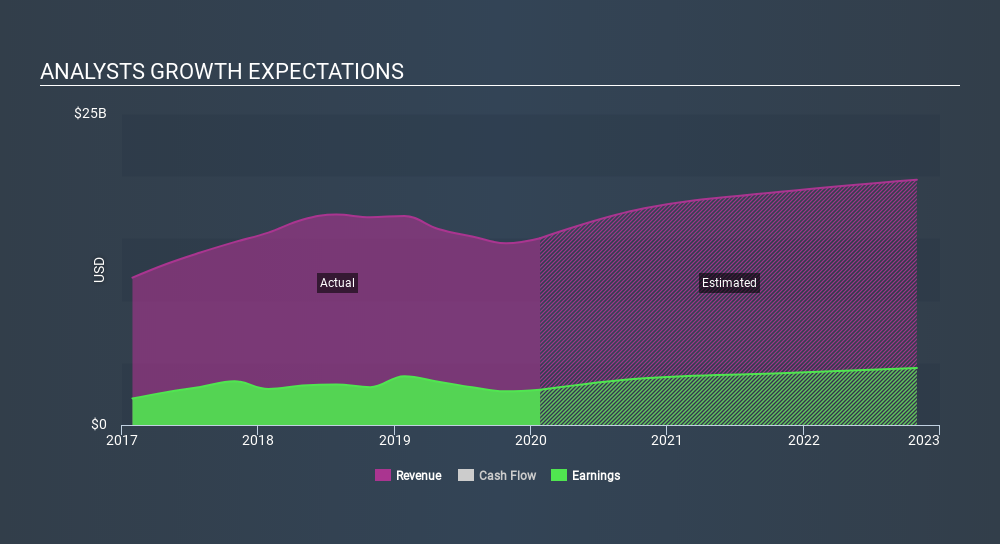

Following the latest results, Applied Materials's 22 analysts are now forecasting revenues of US$17.4b in 2020. This would be a notable 16% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to shoot up 31% to US$4.00. Yet prior to the latest earnings, analysts had been forecasting revenues of US$16.5b and earnings per share (EPS) of US$3.68 in 2020. It looks like there's been a modest increase in sentiment following the latest results, with analysts becoming a bit more optimistic in their predictions for both revenues and earnings.

With these upgrades, we're not surprised to see that analysts have lifted their price target 9.0% to US$75.00 per share. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Applied Materials analyst has a price target of US$86.00 per share, while the most pessimistic values it at US$51.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Applied Materials shareholders.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that Applied Materials's rate of growth is expected to accelerate meaningfully, with forecast 16% revenue growth noticeably faster than its historical growth of 13%p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 8.7% per year. It seems obvious that, while the growth outlook is brighter than the recent past, analysts also expect Applied Materials to grow faster than the wider market.

The Bottom Line

The biggest takeaway for us from these new estimates is that the consensus upgraded its earnings per share estimates, showing a clear improvement in sentiment around Applied Materials's earnings potential next year. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider market. There was also a nice increase in the price target, with analysts feeling that the intrinsic value of the business is improving.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have forecasts for Applied Materials going out to 2022, and you can see them free on our platform here.

It might also be worth considering whether Applied Materials's debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:AMAT

Applied Materials

Provides materials engineering solutions, equipment, services, and software to the semiconductor and related industries in the United States, China, Korea, Taiwan, Japan, Southeast Asia, Europe, and internationally.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.561.6% undervalued

41 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.829.8% undervalued

17 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23057.4% overvalued

48 followersusers have followed this narrative

1 commentusers have commented on this narrative

12 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32041.2% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

SI

Simplicity_Over_Noise on Aurinia Pharmaceuticals ·

Aurinia Pharmaceuticals: Focused Execution in a Narrow but Durable Niche

Fair Value:US$16.290.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

steffen_4h13a on Alzinova ·

Fair value 7.1B Sek

Fair Value:SEK 8598.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AndyB72 on NNN REIT ·

NNN - National Retail Properties Inc. | I'm on 75% position and waiting to buy more.

Fair Value:US$46.421.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.7% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5456.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.9% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative