Advertisement

Analysts Just Slashed Their Public Joint Stock Company Aeroflot - Russian Airlines (MCX:AFLT) Earnings Forecasts

The latest analyst coverage could presage a bad day for Public Joint Stock Company Aeroflot - Russian Airlines (MCX:AFLT), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

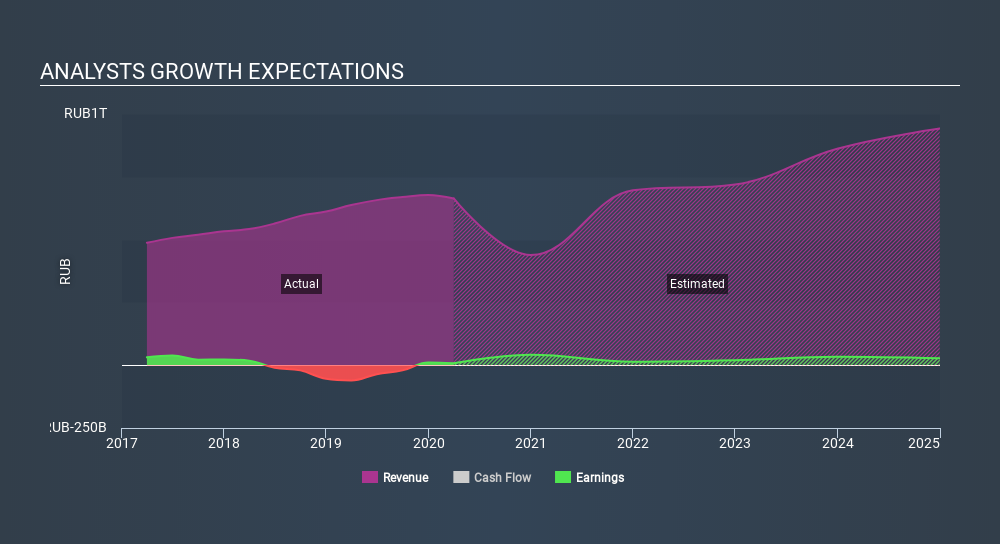

Following the latest downgrade, the ten analysts covering Aeroflot - Russian Airlines provided consensus estimates of ₽399b revenue in 2020, which would reflect a substantial 40% decline on its sales over the past 12 months. Following this this downgrade, earnings are now expected to tip over into loss-making territory, with the analysts forecasting losses of ₽14.93 per share in 2020. Before this latest update, the analysts had been forecasting revenues of ₽445b and earnings per share (EPS) of ₽33.55 in 2020. There looks to have been a major change in sentiment regarding Aeroflot - Russian Airlines' prospects, with a measurable cut to revenues and the analysts now forecasting a loss instead of a profit.

View our latest analysis for Aeroflot - Russian Airlines

There was no major change to the consensus price target of US$1.41, signalling that the business is performing roughly in line with expectations, despite lower earnings per share forecasts. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Aeroflot - Russian Airlines analyst has a price target of US$144 per share, while the most pessimistic values it at US$51.52. We would probably assign less value to the forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Aeroflot - Russian Airlines' past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with the forecast 40% revenue decline a notable change from historical growth of 13% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 8.6% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Aeroflot - Russian Airlines is expected to lag the wider industry.

The Bottom Line

The biggest low-light for us was that the forecasts for Aeroflot - Russian Airlines dropped from profits to a loss this year. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Aeroflot - Russian Airlines' revenues are expected to grow slower than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of Aeroflot - Russian Airlines.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Aeroflot - Russian Airlines going out to 2024, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About MISX:AFLT

Aeroflot - Russian Airlines

Public Joint Stock Company Aeroflot - Russian Airlines, together with its subsidiaries, provides passenger and cargo air transportation services in Russia and internationally.

Good value slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor