Advertisement

Alexion Pharmaceuticals, Inc. Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

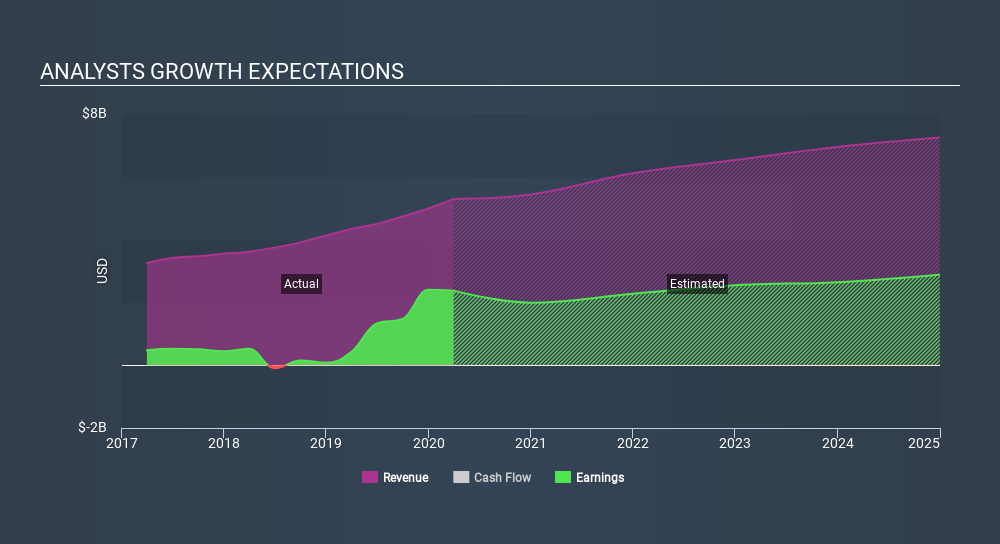

Alexion Pharmaceuticals, Inc. (NASDAQ:ALXN) just released its latest first-quarter results and things are looking bullish. Alexion Pharmaceuticals beat earnings, with revenues hitting US$1.4b, ahead of expectations, and statutory earnings per share outperforming analyst reckonings by a solid 12%. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Alexion Pharmaceuticals

After the latest results, the 23 analysts covering Alexion Pharmaceuticals are now predicting revenues of US$5.44b in 2020. If met, this would reflect a modest 2.7% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to sink 17% to US$8.83 in the same period. In the lead-up to this report, the analysts had been modelling revenues of US$5.60b and earnings per share (EPS) of US$8.89 in 2020. So it looks like the analysts have become a bit less optimistic after the latest results announcement, with revenues expected to fall even as the company is supposed to maintain EPS.

The average price target was steady at US$137 even though revenue estimates declined; likely suggesting the analysts place a higher value on earnings. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Alexion Pharmaceuticals at US$170 per share, while the most bearish prices it at US$110. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's pretty clear that there is an expectation that Alexion Pharmaceuticals' revenue growth will slow down substantially, with revenues next year expected to grow 2.7%, compared to a historical growth rate of 16% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 19% next year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Alexion Pharmaceuticals.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target held steady at US$137, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Alexion Pharmaceuticals going out to 2024, and you can see them free on our platform here.

It might also be worth considering whether Alexion Pharmaceuticals' debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor