- India

- /

- Healthcare Services

- /

- NSEI:LOTUSEYE

A Rising Share Price Has Us Looking Closely At Lotus Eye Hospital and Institute Limited's (NSE:LOTUSEYE) P/E Ratio

Lotus Eye Hospital and Institute (NSE:LOTUSEYE) shares have had a really impressive month, gaining 34%, after some slippage. Looking back a bit further, we're also happy to report the stock is up 71% in the last year.

Assuming no other changes, a sharply higher share price makes a stock less attractive to potential buyers. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that deep value investors might steer clear when expectations of a company are too high. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

Check out our latest analysis for Lotus Eye Hospital and Institute

How Does Lotus Eye Hospital and Institute's P/E Ratio Compare To Its Peers?

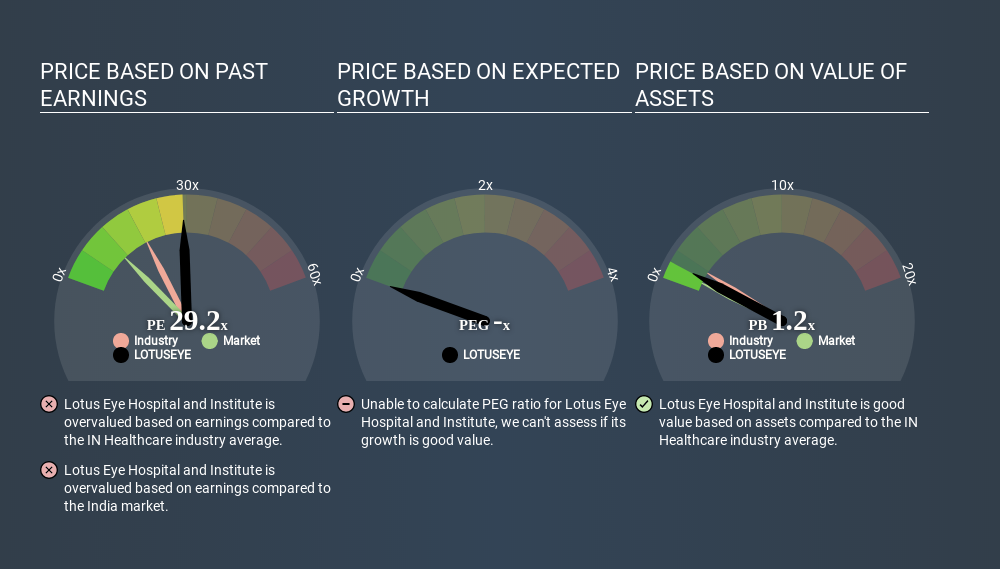

We can tell from its P/E ratio of 33.39 that there is some investor optimism about Lotus Eye Hospital and Institute. The image below shows that Lotus Eye Hospital and Institute has a higher P/E than the average (25.8) P/E for companies in the healthcare industry.

Lotus Eye Hospital and Institute's P/E tells us that market participants think the company will perform better than its industry peers, going forward. The market is optimistic about the future, but that doesn't guarantee future growth. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. Earnings growth means that in the future the 'E' will be higher. That means even if the current P/E is high, it will reduce over time if the share price stays flat. A lower P/E should indicate the stock is cheap relative to others -- and that may attract buyers.

In the last year, Lotus Eye Hospital and Institute grew EPS like Taylor Swift grew her fan base back in 2010; the 211% gain was both fast and well deserved. And earnings per share have improved by 44% annually, over the last three years. So you might say it really deserves to have an above-average P/E ratio.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

Don't forget that the P/E ratio considers market capitalization. In other words, it does not consider any debt or cash that the company may have on the balance sheet. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

So What Does Lotus Eye Hospital and Institute's Balance Sheet Tell Us?

Since Lotus Eye Hospital and Institute holds net cash of ₹52m, it can spend on growth, justifying a higher P/E ratio than otherwise.

The Verdict On Lotus Eye Hospital and Institute's P/E Ratio

Lotus Eye Hospital and Institute trades on a P/E ratio of 33.4, which is multiples above its market average of 10.9. The excess cash it carries is the gravy on top its fast EPS growth. To us, this is the sort of company that we would expect to carry an above average price tag (relative to earnings). What is very clear is that the market has become significantly more optimistic about Lotus Eye Hospital and Institute over the last month, with the P/E ratio rising from 25.0 back then to 33.4 today. For those who prefer to invest with the flow of momentum, that might mean it's time to put the stock on a watchlist, or research it. But the contrarian may see it as a missed opportunity.

Investors should be looking to buy stocks that the market is wrong about. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. Although we don't have analyst forecasts shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

But note: Lotus Eye Hospital and Institute may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About NSEI:LOTUSEYE

Lotus Eye Hospital and Institute

A specialty eye care hospital, provides eye care and related services in India.

Flawless balance sheet with questionable track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)