Advertisement

3 TSX Stocks Estimated To Be Trading At Discounts Up To 44.9%

Simply Wall St

Reviewed by Simply Wall St

The Canadian market is currently navigating a landscape where inflation pressures are influenced by both goods and services, with services showing signs of moderation. Amid these economic conditions, investors often seek stocks that appear undervalued relative to their intrinsic value, presenting potential opportunities for growth despite broader market uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| West Fraser Timber (TSX:WFG) | CA$96.21 | CA$174.60 | 44.9% |

| Triple Flag Precious Metals (TSX:TFPM) | CA$31.76 | CA$48.59 | 34.6% |

| TerraVest Industries (TSX:TVK) | CA$167.03 | CA$310.01 | 46.1% |

| OceanaGold (TSX:OGC) | CA$18.91 | CA$34.82 | 45.7% |

| Magellan Aerospace (TSX:MAL) | CA$17.22 | CA$26.79 | 35.7% |

| K92 Mining (TSX:KNT) | CA$14.37 | CA$22.79 | 36.9% |

| Ivanhoe Mines (TSX:IVN) | CA$10.65 | CA$20.16 | 47.2% |

| Exchange Income (TSX:EIF) | CA$65.99 | CA$97.92 | 32.6% |

| Endeavour Mining (TSX:EDV) | CA$42.21 | CA$71.51 | 41% |

| Blackline Safety (TSX:BLN) | CA$6.25 | CA$10.17 | 38.5% |

We're going to check out a few of the best picks from our screener tool.

Alphamin Resources (TSXV:AFM)

Overview: Alphamin Resources Corp., along with its subsidiaries, focuses on the production and sale of tin concentrate and has a market cap of CA$1.20 billion.

Operations: The company's revenue is primarily derived from the production and sale of tin concentrate from its Bisie Tin Mine, amounting to $539.16 million.

Estimated Discount To Fair Value: 29.1%

Alphamin Resources appears undervalued based on cash flows, trading at 29.1% below its estimated fair value of CA$1.32, with a current price of CA$0.94. Despite an unstable dividend track record, the company has shown significant earnings growth of over 100% in the past year and is expected to continue growing at a rate faster than the Canadian market. The recent acquisition by Alpha Mining Ltd for CAD 500 million could further impact its valuation dynamics positively or negatively depending on integration outcomes and strategic direction post-acquisition.

- The growth report we've compiled suggests that Alphamin Resources' future prospects could be on the up.

- Get an in-depth perspective on Alphamin Resources' balance sheet by reading our health report here.

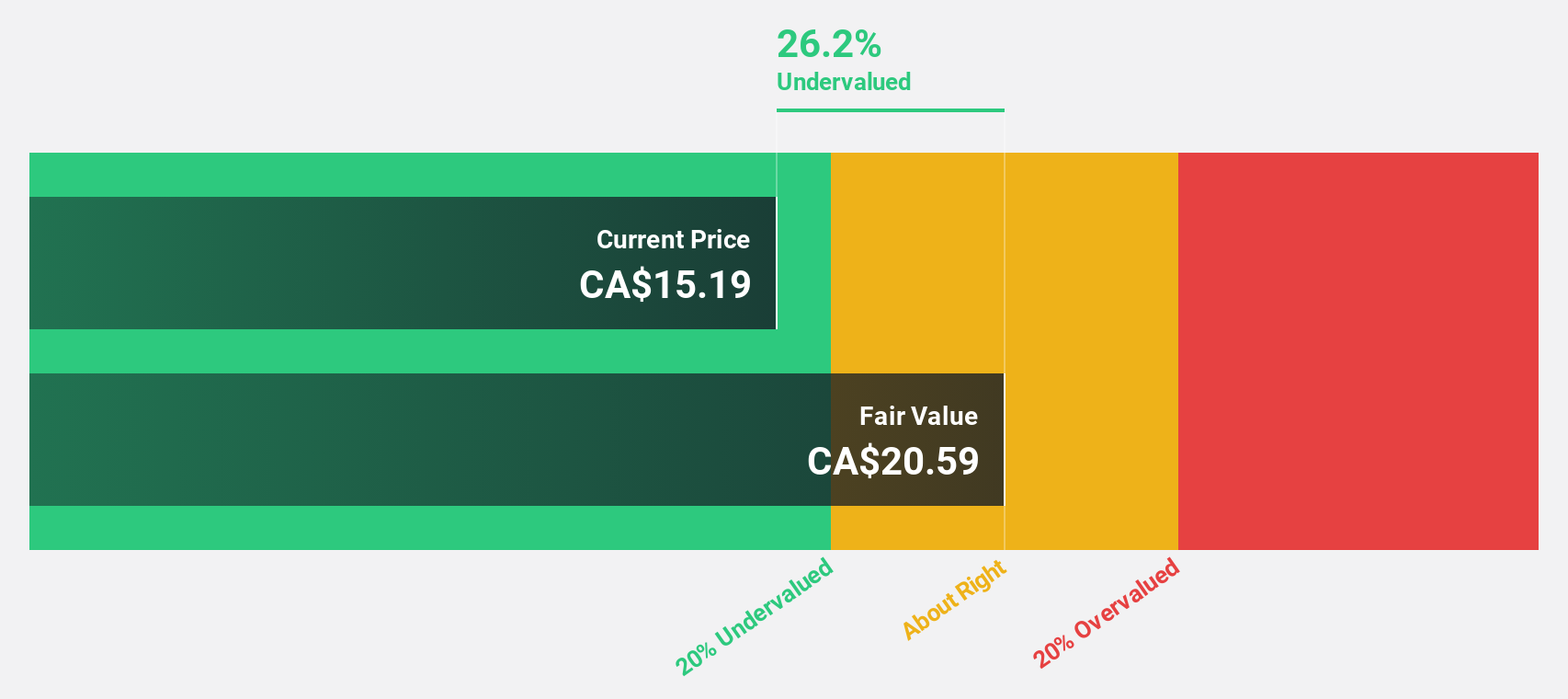

VersaBank (TSX:VBNK)

Overview: VersaBank offers a range of banking products and services in Canada and the United States, with a market cap of CA$515.10 million.

Operations: VersaBank generates revenue from its Digital Banking Canada segment, which accounts for CA$96.26 million, and its DRTC division, focused on cybersecurity services and financial technology development, contributing CA$9.24 million.

Estimated Discount To Fair Value: 22.4%

VersaBank is trading at CA$15.84, below its fair value estimate of CA$20.40, suggesting it may be undervalued based on cash flows. Despite recent shareholder dilution and significant insider selling, the bank's earnings are forecast to grow substantially at 61.8% annually over the next three years, outpacing the Canadian market average. Recent executive changes could impact strategic direction as Susan McGovern steps in as interim CEO amidst ongoing structural realignment efforts.

- Insights from our recent growth report point to a promising forecast for VersaBank's business outlook.

- Delve into the full analysis health report here for a deeper understanding of VersaBank.

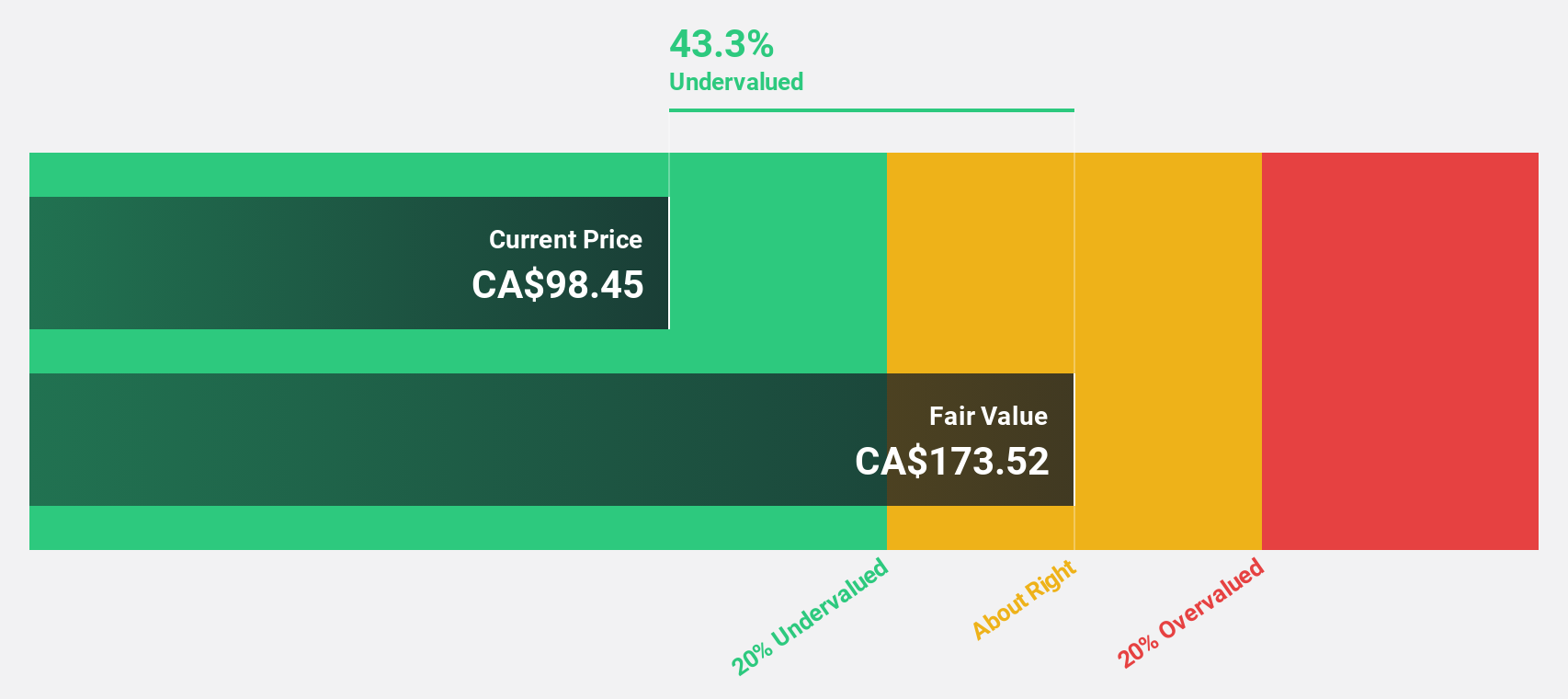

West Fraser Timber (TSX:WFG)

Overview: West Fraser Timber Co. Ltd. is a diversified wood products company involved in manufacturing, selling, marketing, and distributing lumber, engineered wood products, pulp, newsprint, wood chips, other residuals and renewable energy with a market cap of CA$7.59 billion.

Operations: West Fraser Timber's revenue is primarily derived from Lumber ($2.60 billion), North America Engineered Wood Products ($2.51 billion), Pulp & Paper ($318 million), and Europe Engineered Wood Products ($474 million).

Estimated Discount To Fair Value: 44.9%

West Fraser Timber is trading at CA$96.21, significantly below its estimated fair value of CA$174.6, indicating it may be undervalued based on cash flows. Despite recent quarterly losses and reduced sales, the company forecasts substantial earnings growth of 52.87% annually over the next three years. Recent buybacks and a renewed $1 billion credit facility enhance financial flexibility, although return on equity is expected to remain modest at 9.2%.

- In light of our recent growth report, it seems possible that West Fraser Timber's financial performance will exceed current levels.

- Click to explore a detailed breakdown of our findings in West Fraser Timber's balance sheet health report.

Make It Happen

- Get an in-depth perspective on all 21 Undervalued TSX Stocks Based On Cash Flows by using our screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:VBNK

VersaBank

Provides various banking products and services in Canada and the United States.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor