Last Update 19 Jun 26

JNJ: Future Drug Cycle And Dividend Strength Will Balance Policy And Legal Risks

Analysts have raised the Johnson & Johnson price target to $265 from $252, reflecting increased confidence in the company’s new drug momentum and product cycle, while also considering ongoing policy and partnership risks highlighted in recent research.

Analyst Commentary

Recent Street research around Johnson & Johnson highlights a mix of enthusiasm about the company’s new drug pipeline and product cycle, alongside fresh policy questions and selected partnership headwinds that investors should factor into expectations for execution and valuation.

Bullish Takeaways

- Bullish analysts point to what they describe as strong new drug momentum at Johnson & Johnson, with particular focus on pipeline assets such as Icotyde and Inlexzo, which they see as important to long term growth and the justification for higher price targets.

- Several firms, including large global houses, have raised Johnson & Johnson price targets in close succession. This is interpreted by some as a sign of rising confidence in the company’s ability to execute on its product cycle and capture value from its research investments.

- Coverage assumed with positive ratings at major brokers, alongside upgrades from neutral stances, suggests that a broader group of analysts now sees the risk or reward balance as more favorable for the stock than in prior periods.

- Comments about ongoing product cycle momentum from international banks indicate that, in their view, Johnson & Johnson has multiple drivers within its portfolio that could support revenue over time rather than relying on a single product.

Bearish Takeaways

- Policy risk has re-emerged as a concern, with the proposed move to make the Medicare Drug Price Negotiation Program permanent from 2029 and tighter rules on combination products. These developments create potential pressure on long term pricing for Johnson & Johnson therapies.

- Bearish analysts highlight that, while legal challenges and exemptions may soften the program’s impact, the headline risk alone can affect sentiment and the multiple investors are willing to pay for Johnson & Johnson earnings.

- Commentary from firms covering related partners points to supply constraints and the winding down of certain relationships, which could introduce some friction for Johnson & Johnson around collaboration driven revenue or cost efficiencies.

- The emphasis by some analysts on “aspirational” long term growth targets serves as a reminder that execution risk remains, particularly if upcoming events or data do not match the optimism embedded in higher price targets.

What’s in the News for Johnson & Johnson

- Johnson & Johnson reported positive Phase 3 MonumenTAL-3 results for multiple myeloma, where TALVEY combined with DARZALEX FASPRO, with or without pomalidomide, reduced the risk of disease progression or death by up to 72% and the risk of death by up to 53% versus a standard DARZALEX FASPRO based regimen. The data were published in The New England Journal of Medicine and presented at a major scientific meeting. (Source: company release, EHA, NEJM)

- The company announced a US$1b cash acquisition of Firefly Bio, adding a degrader antibody conjugate platform targeting KRAS driven tumors to Johnson & Johnson’s oncology pipeline. Closing is subject to regulatory approvals later in 2026. (Source: recent M&A announcement)

- A Los Angeles jury ordered Johnson & Johnson and subsidiaries to pay US$32m in an asbestos linked talc case involving historical baby powder products, adding to legal and reputational pressures around legacy talc litigation. (Source: court verdict reporting)

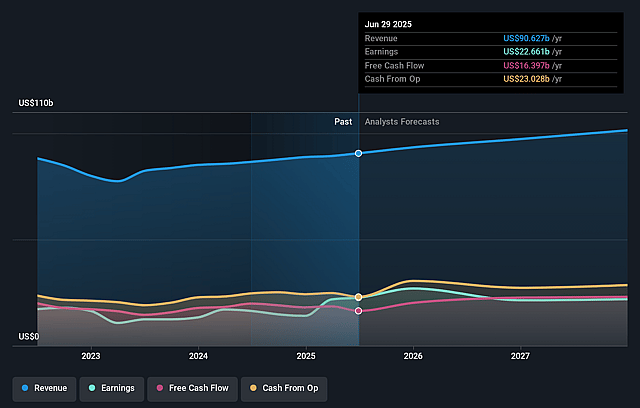

- Johnson & Johnson increased its quarterly dividend by 3.1% to US$1.34 per share, marking 64 consecutive years of dividend growth. This was announced alongside Q1 2026 revenue of US$24.06b and updated full year guidance of US$100.3b to US$101.3b in revenue and adjusted EPS of US$11.45 to US$11.65. (Source: Q1 2026 and dividend announcement)

- The company plans to invest more than US$1b in a new ACUVUE contact lens manufacturing and distribution facility in Jacksonville, Florida, as part of a wider US$55b commitment to US manufacturing, R&D and technology through early 2029. (Source: manufacturing investment announcement)

Valuation Changes for Johnson & Johnson Stock

- Fair Value: Model fair value remains unchanged at $252.87 per share, with no shift in the underlying valuation output.

- Discount Rate: The discount rate is effectively stable at 7.11%, indicating no material revision to the required return assumption for Johnson & Johnson.

- Revenue Growth: The long term revenue growth input is steady at 6.56%, reflecting no change to top line expectations used in the model.

- Net Profit Margin: The net profit margin assumption is effectively unchanged at 23.09%, signaling consistent expectations for Johnson & Johnson profitability in the model.

- Future P/E: The future P/E multiple remains at 27.74x, suggesting no adjustment to the valuation multiple applied to forward earnings.

Key Takeaways

- Johnson & Johnson is poised for growth in immunology and oncology despite facing challenges from loss of drug exclusivity, leveraging next-gen therapies for strengthened revenue.

- Strategic investments in U.S. operations, acquisitions, and MedTech expansion aim to boost future earnings and efficiency, with potential restructuring in surgery to aid profitability.

- Loss of exclusivity for key products and tariffs could significantly threaten revenue and margins, while ongoing litigation poses financial risks.

Catalysts

About Johnson & Johnson- Engages in the research and development, manufacture, and sale of various products in the healthcare field worldwide.

- Johnson & Johnson anticipates accelerated growth in their portfolio and pipeline, particularly in the Innovative Medicine sector, despite the headwind from STELARA's loss of exclusivity. This is expected to bolster revenues through next-generation therapies and significant market share gains in oncology and immunology.

- The company's substantial investment of over $55 billion into manufacturing, R&D, and technology in the U.S. over the next four years is projected to expand capacity for advanced medicines and devices, potentially increasing operational efficiency and future earnings.

- Recent acquisitions, such as Intra-Cellular Therapies, are expected to contribute substantial revenue streams, with products like CAPLYTA potentially reaching over $5 billion in peak sales, positively affecting the company’s revenue and EPS in the future.

- Ongoing expansion within MedTech, highlighted by strong performance from acquired cardiovascular units Abiomed and Shockwave, as well as developments in robotic surgery, are expected to drive revenue growth and enhance adjusted income margins over time.

- The company plans significant restructuring in their surgery business within MedTech to streamline operations and improve efficiency, anticipated to have short-term revenue disruptions but expected to enhance long-term profitability and margin expansion.

Johnson & Johnson Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Johnson & Johnson's revenue will grow by 6.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 21.8% today to 23.1% in 3 years time.

- Analysts expect earnings to reach $26.9 billion (and earnings per share of $11.45) by about June 2029, up from $21.0 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $22.5 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 27.7x on those 2029 earnings, up from 26.1x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 15.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Loss of exclusivity for STELARA and the impact of biosimilar competition could significantly erode revenue from one of Johnson & Johnson's major products. This could affect overall revenue and net margins, especially in the innovative medicine segment.

- Tariffs, particularly those related to exports to China, could increase costs and impact the net margins negatively, due to increased cost of goods sold from tariffs being relieved through the P&L in future periods.

- The ongoing litigation related to talc, though controlled for now, poses a continual risk to financial stability and could impact net earnings and cash flow, particularly if adverse judgments or settlements occur.

- The orthopedics segment faced headwinds, including competitive pressures and challenges in the spine and sports areas. Ongoing issues could impact revenue and earnings unless the planned innovations drive a turnaround.

- Potential dilution from acquisitions such as Intra-Cellular Therapies and the impact of tariffs could affect operating margin improvement efforts, challenging overall earnings and net margins despite robust sales growth in some areas.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $252.87 for Johnson & Johnson based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $285.0, and the most bearish reporting a price target of just $155.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $116.6 billion, earnings will come to $26.9 billion, and it would be trading on a PE ratio of 27.7x, assuming you use a discount rate of 7.1%.

- Given the current share price of $228.39, the analyst price target of $252.87 is 9.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Johnson & Johnson?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.